Deck 9: Diversifying, Acquiring, and Restructuring

Full screen (f)

Question

Question

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

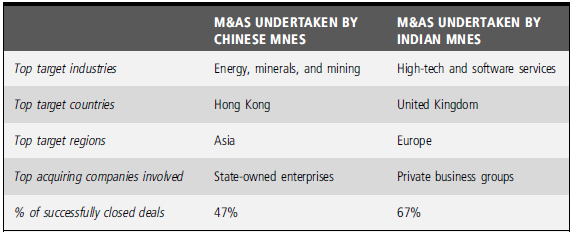

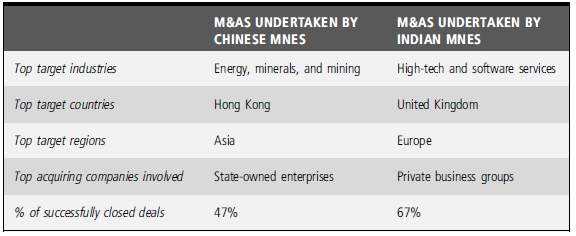

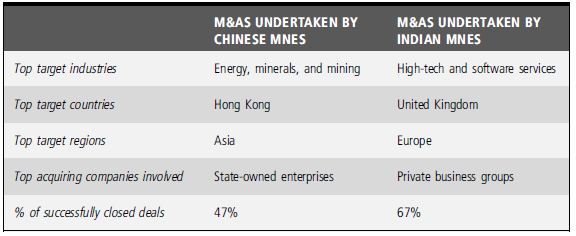

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Why have M As emerged as the primary mode of foreign market entry for Chinese and Indian MNEs?

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Why have M As emerged as the primary mode of foreign market entry for Chinese and Indian MNEs?

Question

Question

Question

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Drawing on industry-based, resource-based, and institution-based views, outline the similarities and differences between Chinese and Indian multinational acquirers.

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Drawing on industry-based, resource-based, and institution-based views, outline the similarities and differences between Chinese and Indian multinational acquirers.

Question

Question

Question

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management ,27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal , 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

ON ETHICS: As CEO of a firm from either China or India engaging in a high-profile acquisition overseas, shareholders at home are criticizing you of "squandering" their money, and target firm management and unions-as well as host country government and the media-are resisting. Should you proceed with the acquisition or consider abandoning the deal? If you are considering abandoning the deal, under what conditions would you abandon it?

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management ,27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal , 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

ON ETHICS: As CEO of a firm from either China or India engaging in a high-profile acquisition overseas, shareholders at home are criticizing you of "squandering" their money, and target firm management and unions-as well as host country government and the media-are resisting. Should you proceed with the acquisition or consider abandoning the deal? If you are considering abandoning the deal, under what conditions would you abandon it?

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/9

Play

Full screen (f)

Deck 9: Diversifying, Acquiring, and Restructuring

1

ON ETHICS: As members of the executive team of a firm, you are trying to decide whether to acquire a foreign firm. The size of your firm will double after this acquisition and it will become the largest in your industry. On the one hand, you are excited about the opportunity to be a leading captain of industry and the associated power, prestige, and income (you expect your income to double next year). On the other hand, you have just read this chapter and are troubled by the 70% M A failure rate. Working in small groups of three or four, develop a strategy for success. Present your strategy in a short paper or visual presentation.

The following are the strategy for success after acquisition:

Explanation:

A firm should make sure that the acquisition is not very costly, and the organization should consider all the factors in identifying how to execute acquisition for all the employees' best interests. A company should try to acquire another company that is performing similar tasks.

If the acquisition were to be carefully planned, the new product lines and distribution should be analyzed in such a way, that cost cutting and net head count reduction should be planned jointly.

The newly shared company shouldfocus on enhancing its product line and determining new ways to compete in the market rather than focusing more on cost reduction.

Explanation:

A firm should make sure that the acquisition is not very costly, and the organization should consider all the factors in identifying how to execute acquisition for all the employees' best interests. A company should try to acquire another company that is performing similar tasks.

If the acquisition were to be carefully planned, the new product lines and distribution should be analyzed in such a way, that cost cutting and net head count reduction should be planned jointly.

The newly shared company shouldfocus on enhancing its product line and determining new ways to compete in the market rather than focusing more on cost reduction.

2

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Why have M As emerged as the primary mode of foreign market entry for Chinese and Indian MNEs?

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Why have M As emerged as the primary mode of foreign market entry for Chinese and Indian MNEs?

The following are the reason why merger and acquisition appear as the primary mode of foreign market entry for CH and ID Countries multinational enterprise (MNE):

Multinational enterprises from ID and CH countries utilize acquisition and merger as the main method to enter foreign markets to utilize the benefit that result from them.

The shareholders gain is considered as the worth foran organization after the acquisition. It also translates into tax growth and can guide to revenue improvement through market share growth. Further, the joint firm gets advantages in conditions of cost effectiveness. Other benefits would be to facilitate a company to get into a new market or to gain industry recognizeon positioning or financial leveraging.

In the context of CH and ID countries multinational enterprises, the cause for acquiring foreign companies using acquisition and merger lies in their requirement for strategic resources, CH country's resources such as minerals, energy, and mining, and ID country for improved technology. The act of purchasinganoverseasorganization could also be interpreted as an act that validates their self-assurance and confidence and in an oblique method their pride in their CH or ID countries identity.

Multinational enterprises from ID and CH countries utilize acquisition and merger as the main method to enter foreign markets to utilize the benefit that result from them.

The shareholders gain is considered as the worth foran organization after the acquisition. It also translates into tax growth and can guide to revenue improvement through market share growth. Further, the joint firm gets advantages in conditions of cost effectiveness. Other benefits would be to facilitate a company to get into a new market or to gain industry recognizeon positioning or financial leveraging.

In the context of CH and ID countries multinational enterprises, the cause for acquiring foreign companies using acquisition and merger lies in their requirement for strategic resources, CH country's resources such as minerals, energy, and mining, and ID country for improved technology. The act of purchasinganoverseasorganization could also be interpreted as an act that validates their self-assurance and confidence and in an oblique method their pride in their CH or ID countries identity.

3

M As are a rare event for most firms. How can they enhance their capabilities for M As?

The following are the ways in which merger and acquisition can enhance their capabilities:

While considering a merger or an acquisition, the key question that needs to be answered concerns how the company will generate value from the deal. During the pre-acquisition stage firms should ideally ask and acquire an answer for this question,"Will this merger and acquisition fulfill the firm's mission?"

• Is the acquisition a capability-based one : This will help the managers to identify organizational areas that will be impacted and the financial savings or value that can be achieved

• Planning for future expansion : In some situations, buyers may purchase a company and keep it aside for a later requirement. Sometimes, a particular acquisition might be immediately required for the organization success

• Combining the capability : Companies must have a strategy that explains how the ability would be incorporated into the larger entity. The key to successful integration would be to identify and articulate the ability that you hope to obtain through the acquisition

While considering a merger or an acquisition, the key question that needs to be answered concerns how the company will generate value from the deal. During the pre-acquisition stage firms should ideally ask and acquire an answer for this question,"Will this merger and acquisition fulfill the firm's mission?"

• Is the acquisition a capability-based one : This will help the managers to identify organizational areas that will be impacted and the financial savings or value that can be achieved

• Planning for future expansion : In some situations, buyers may purchase a company and keep it aside for a later requirement. Sometimes, a particular acquisition might be immediately required for the organization success

• Combining the capability : Companies must have a strategy that explains how the ability would be incorporated into the larger entity. The key to successful integration would be to identify and articulate the ability that you hope to obtain through the acquisition

4

Some argue that shareholders can diversify their stockholdings and that there is no need for corporate diversification to reduce risk. The upshot is that any excess earnings (known as "free cash flows"), instead of being used to acquire other firms, should be returned to shareholders as dividends and that firms should pursue more focused strategies. Write a short paper explaining why you agree or disagree with this statement.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

5

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Drawing on industry-based, resource-based, and institution-based views, outline the similarities and differences between Chinese and Indian multinational acquirers.

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management , 27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal, 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

Drawing on industry-based, resource-based, and institution-based views, outline the similarities and differences between Chinese and Indian multinational acquirers.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

6

ON ETHICS: As a CEO leading an acquisition of a foreign firm (think of Anheuser-Busch or Cadbury), you are interviewed by a reporter from the host country. The reporter asks: "A lot of people in our country are mad about this foreign takeover of our iconic company. How would you alleviate their concerns?"

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

7

Unrelated product diversification (conglomeration) is widely discredited in developed economies. However, in some cases it still seems to add value in emerging economies (see the Opening Case). Is this interest in conglomeration likely to hold or decrease in emerging economies over time? Why? Explain your answers in a short paper.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

8

Emerging Markets: Emerging Acquirers from China and India

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs

Source: Extracted from S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business, 47(1): 4-16.

From an institution-based view, the contrasts between the leading Chinese and Indian acquirers are significant. The primary M A players from China are state-owned enterprises (SOEs), which have their own advantages (such as strong support from the Chinese government) and trappings (such as resentment and suspicion from host country governments). The movers and shakers of overseas M As from India are private business groups, which generally are not viewed with strong suspicion. The limited evidence suggests that M As by Indian firms tend to create value for their shareholders. On the other hand, M As by Chinese firms tend to destroy value for their shareholders-indicative of potential hubris and managerial motives evidenced by empire building and agency problems.

Announcing high-profile deals is one thing, but completing them is another matter. Chinese MNEs have particularly poor records in completing the overseas acquisition deals they announce. Only less than half (47%) of the acquisitions announced by Chinese MNEs were completed, which compares unfavorably to Indian MNEs' 67% completion rate. Chinese MNEs' lack of ability and experience in due diligence and financing is one reason, but another reason is the political backlash and resistance they encounter, especially in developed economies. The 2005 failure of CNOOC's bid for Unocal in the United States and the 2009 failure of Chinalco's bid for Rio Tinto's assets in Australia are but two high-profile examples.

Even assuming successful completion, integration is a leading challenge during the post-acquisition phase. Both Chinese and Indian firms seem to suffer from these challenges. Tata, for example, was famously clawed by Jaguar. In general, acquirers from China and India have often taken the "high road" to acquisitions, in which acquirers deliberately allow acquired target companies to retain autonomy, keep the top management intact, and then gradually encourage interaction between the two sides. In contrast, the "low road" to acquisitions would be for acquirers to act quickly to impose their systems and rules on acquired target companies. Although the "high road" sounds noble, this is a reflection of these acquirers' lack of international management experience and capabilities.

Sources: Based on (1) Y. Chen M. Young, 2010, Crossborder M As by Chinese listed companies, Asia Pacific Journal of Management ,27: 523-539; (2) L. Cui F. Jiang, 2010, Behind ownership decision of Chinese outward FDI, Asia Pacific Journal of Management , 27: 751-774; (3) P. Deng, 2009, Why do Chinese firms tend to acquire strategic assets in international expansion? Journal of World Business , 44: 74-84; (4) S. Gubbi, P. Aulakh, S. Ray, M. Sarkar, R. Chittoor, 2010, Do international acquisitions by emerging economy firms create shareholder value? Journal of International Business Studies , 41: 397-418; (5) M. W. Peng, 2012, The global strategy of emerging multinationals from China, Global Strategy Journal , 2: 97-107; (6) M. W. Peng, 2012, Why China's investments aren't a threat, Harvard Business Review , February: blogs.hbr.org; (7) H. Rui G. Yip, 2008, Foreign acquisitions by Chinese firms, Journal of World Business , 43: 213-226; (8) S. Sun, M. W. Peng, B. Ren, D. Yan, 2012, A comparative ownership advantage framework for cross-border M As: The rise of Chinese and Indian MNEs, Journal of World Business , 47(1): 4-16.

ON ETHICS: As CEO of a firm from either China or India engaging in a high-profile acquisition overseas, shareholders at home are criticizing you of "squandering" their money, and target firm management and unions-as well as host country government and the media-are resisting. Should you proceed with the acquisition or consider abandoning the deal? If you are considering abandoning the deal, under what conditions would you abandon it?

Multinational enterprises (MNEs) from emerging economies, especially from China and India, have emerged as a new breed of acquirers around the world. Causing "oohs" and "ahhs," they have grabbed media headlines and caused controversies. Anecdotes aside, are the patterns of these new global acquirers similar? How do they differ? Only recently has rigorous academic research been conducted to allow for systematic comparison (Table 9.6).

Overall, China's stock of outward foreign direct investment (OFDI) (1.5% of the worldwide total) is about three times India's (0.5%). A visible similarity is that both Chinese and Indian MNEs seem to primarily use M As as their primary mode of OFDI. Throughout the 2000s, Chinese firms spent $130 billion to engage in M As overseas, whereas Indian firms made M A deals worth $60 billion.

From an industry-based view, it is clear that MNEs from China and India have targeted industries to support and strengthen their own most competitive industries at home. Given China's prowess in manufacturing industries at home, Chinese firms' overseas M As have primarily targeted energy, minerals, and mining-crucial supply industries that feed their manufacturing operations. Indian MNEs' world-class leadership position in high-tech and software services is reflected in their interest in acquiring firms in these industries.

The geographic spread of these MNEs is indicative of the level of their capabilities. Chinese firms have undertaken most of their deals in Asia, with Hong Kong being their most favorable location. In other words, the geographic distribution of Chinese M As is not global; rather, it is quite regional. This reflects a relative lack of capabilities to engage in managerial challenges in regions distant from China, especially in more developed economies. Indian MNEs have primarily made deals in Europe, with the United Kingdom as the leading target country. For example, acquisitions made by Tata Motors (Jaguar and Land Rover) and Tata Steel (Corus Group) propelled Tata Group to become the number one private-sector employer in the UK. Overall, Indian firms display a more global spread in their M As, and a higher level of confidence and sophistication in making deals in developed economies.

TABLE 9.6 Comparing Cross-Border M As Undertaken by Chinese and Indian MNEs