Deck 18: The Theory of Multiple Regression

Full screen (f)

Question

Question

Question

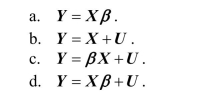

The multiple regression model can be written in matrix form as follows:

Question

The GLS estimator is defined as

Question

Question

Question

Question

Question

Question

Question

One implication of the extended least squares assumptions in the multiple regression model is that

Question

Question

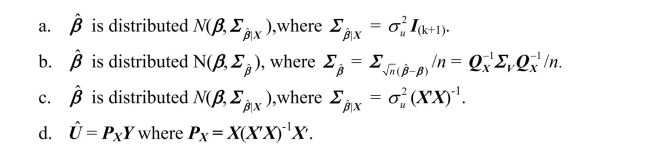

In the case when the errors are homoskedastic and normally distributed, conditional on X, then

Question

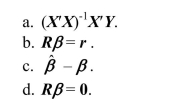

A joint hypothesis that is linear in the coefficients and imposes a number of restrictions can be written as

Question

Question

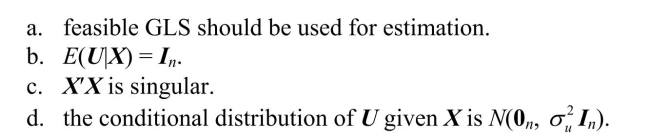

The GLS assumptions include all of the following, with the exception of

Question

Question

The Gauss-Markov theorem for multiple regression proves that

Question

One of the properties of the OLS estimator is

Question

Question

Define the GLS estimator and discuss its properties when  is known. Why is this estimator sometimes called infeasible GLS? What happens when

is known. Why is this estimator sometimes called infeasible GLS? What happens when  is unknown? What would the

is unknown? What would the  matrix look like for the case of independent sampling with heteroskedastic errors, where

matrix look like for the case of independent sampling with heteroskedastic errors, where

Since the inverse of the error variancecovariance matrix is needed to compute the GLS estimator, find https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/ . The textbook shows that the original model

. The textbook shows that the original model

will be transformed into where

where

Find in the above case, and describe what effect the transformation has on the original data.

in the above case, and describe what effect the transformation has on the original data.

is known. Why is this estimator sometimes called infeasible GLS? What happens when is unknown? What would the matrix look like for the case of independent sampling with heteroskedastic errors, where Since the inverse of the error variancecovariance matrix is needed to compute the GLS estimator, find https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/

. The textbook shows that the original model will be transformed into

where Find

in the above case, and describe what effect the transformation has on the original data. Question

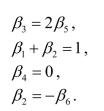

Write the following four restrictions in the form  where the hypotheses are to be tested simultaneously.

where the hypotheses are to be tested simultaneously.

Can you write the following restriction in the same format? Why not?

in the same format? Why not?

where the hypotheses are to be tested simultaneously.Can you write the following restriction

in the same format? Why not? Question

In Chapter 10 of your textbook, panel data estimation was introduced.Panel data consist

of observations on the same n entities at two or more time periods T.For two variables,

you have where n could be the U.S.states.The example in Chapter 10 used annual data from 1982

where n could be the U.S.states.The example in Chapter 10 used annual data from 1982

to 1988 for the fatality rate and beer taxes.Estimation by OLS, in essence, involved

"stacking" the data.

(a)What would the variance-covariance matrix of the errors look like in this case if you

allowed for homoskedasticity-only standard errors? What is its order? Use an example of

a linear regression with one regressor of 4 U.S.states and 3 time periods.

of observations on the same n entities at two or more time periods T.For two variables,

you have

where n could be the U.S.states.The example in Chapter 10 used annual data from 1982to 1988 for the fatality rate and beer taxes.Estimation by OLS, in essence, involved

"stacking" the data.

(a)What would the variance-covariance matrix of the errors look like in this case if you

allowed for homoskedasticity-only standard errors? What is its order? Use an example of

a linear regression with one regressor of 4 U.S.states and 3 time periods.

Question

q = 5 +3 p - 2 y

q = 5 +3 p - 2 yq = 10 - p + 10 y

p = 6 y

Question

Question

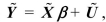

Using the model  and the extended least squares assumptions, derive the OLS estimator https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/

and the extended least squares assumptions, derive the OLS estimator https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/ . Discuss the conditions under which

. Discuss the conditions under which  is invertible.

is invertible.

and the extended least squares assumptions, derive the OLS estimator https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/. Discuss the conditions under which is invertible. Question

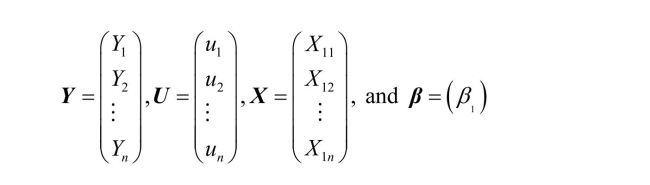

Consider the multiple regression model from Chapter 5, where k = 2 and the assumptions

of the multiple regression model hold.

(a)Show what the X matrix and the vector would look like in this case.

vector would look like in this case.

of the multiple regression model hold.

(a)Show what the X matrix and the

vector would look like in this case. Question

Prove that under the extended least squares assumptions the OLS estimator  is unbiased and that its variance-covariance matrix is

is unbiased and that its variance-covariance matrix is

is unbiased and that its variance-covariance matrix is Question

Assume that the data looks as follows:

Question

Question

Question

In order for a matrix A to have an inverse, its determinant cannot be zero.Derive the

determinant of the following matrices:

determinant of the following matrices:

Question

Your textbook derives the OLS estimator as  Show that the estimator does not exist if there are fewer observations than the number of

Show that the estimator does not exist if there are fewer observations than the number of

explanatory variables, including the constant.What is the rank of X′X in this case?

Show that the estimator does not exist if there are fewer observations than the number ofexplanatory variables, including the constant.What is the rank of X′X in this case?

Question

Given the following matrices

Question

For the OLS estimator  to exist,

to exist,  must be invertible. This is the case when

must be invertible. This is the case when  has full rank. What is the rank of a matrix? What is the rank of the product of two matrices? Is it possible that

has full rank. What is the rank of a matrix? What is the rank of the product of two matrices? Is it possible that  could have rank n ? What would be the rank of

could have rank n ? What would be the rank of  in the case

in the case  Explain intuitively why the OLS estimator does not exist in that situation.

Explain intuitively why the OLS estimator does not exist in that situation.

to exist, must be invertible. This is the case when has full rank. What is the rank of a matrix? What is the rank of the product of two matrices? Is it possible that could have rank n ? What would be the rank of in the case Explain intuitively why the OLS estimator does not exist in that situation. Question

Question

Give several economic examples of how to test various joint linear hypotheses using matrix notation. Include specifications of  where you test for (i) all coefficients other than the constant being zero, (ii) a subset of coefficients being zero, and (iii) equality of coefficients. Talk about the possible distributions involved in finding critical values for your hypotheses.

where you test for (i) all coefficients other than the constant being zero, (ii) a subset of coefficients being zero, and (iii) equality of coefficients. Talk about the possible distributions involved in finding critical values for your hypotheses.

where you test for (i) all coefficients other than the constant being zero, (ii) a subset of coefficients being zero, and (iii) equality of coefficients. Talk about the possible distributions involved in finding critical values for your hypotheses. Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/38

Play

Full screen (f)

Deck 18: The Theory of Multiple Regression

1

The multiple regression model in matrix form can also be written as

A)

B)

C)

D)

A)

B)

C)

D)

2

Minimization of results in

A)

B)

C)

D)

A)

B)

C)

D)

3

The multiple regression model can be written in matrix form as follows:

D

4

The GLS estimator is defined as

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

5

The difference between the central limit theorems for a scalar and vector-valued random variables is

A)that n approaches infinity in the central limit theorem for scalars only.

B)the conditions on the variances.

C)that single random variables can have an expected value but vectors cannot.

D)the homoskedasticity assumption in the former but not the latter.

A)that n approaches infinity in the central limit theorem for scalars only.

B)the conditions on the variances.

C)that single random variables can have an expected value but vectors cannot.

D)the homoskedasticity assumption in the former but not the latter.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

6

The OLS estimator

A)has the multivariate normal asymptotic distribution in large samples.

B)is t-distributed.

C)has the multivariate normal distribution regardless of the sample size.

D)is F-distributed.

A)has the multivariate normal asymptotic distribution in large samples.

B)is t-distributed.

C)has the multivariate normal distribution regardless of the sample size.

D)is F-distributed.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

7

The extended least squares assumptions in the multiple regression model include four assumptions from Chapter 6 are i.i.d. draws from their joint distribution; have nonzero finite fourth moments; there is no perfect multicollinearity). In addition, there are two further assumptions, one of which is

A) heteroskedasticity of the error term.

B) serial correlation of the error term.

C) homoskedasticity of the error term.

D) invertibility of the matrix of regressors.

A) heteroskedasticity of the error term.

B) serial correlation of the error term.

C) homoskedasticity of the error term.

D) invertibility of the matrix of regressors.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

8

The assumption that X has full column rank implies that

A)the number of observations equals the number of regressors.

B)binary variables are absent from the list of regressors.

C)there is no perfect multicollinearity.

D)none of the regressors appear in natural logarithm form.

A)the number of observations equals the number of regressors.

B)binary variables are absent from the list of regressors.

C)there is no perfect multicollinearity.

D)none of the regressors appear in natural logarithm form.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

9

The Gauss-Markov theorem for multiple regressions states that the OLS estimator

A)has the smallest variance possible for any linear estimator.

B)is BLUE if the Gauss-Markov conditions for multiple regression hold.

C)is identical to the maximum likelihood estimator.

D)is the most commonly used estimator.

A)has the smallest variance possible for any linear estimator.

B)is BLUE if the Gauss-Markov conditions for multiple regression hold.

C)is identical to the maximum likelihood estimator.

D)is the most commonly used estimator.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

10

The heteroskedasticity-robust estimator of is obtained

A)

B) by replacing the population moments in its definition by the identity matrix.

C) from feasible GLS estimation.

D) by replacing the population moments in its definition by sample moments.

A)

B) by replacing the population moments in its definition by the identity matrix.

C) from feasible GLS estimation.

D) by replacing the population moments in its definition by sample moments.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

11

One implication of the extended least squares assumptions in the multiple regression model is that

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

12

The formulation to test a hypotheses

A) allows for restrictions involving both multiple regression coefficients and single regression coefficients.

B) is F -distributed in large samples.

C) allows only for restrictions involving multiple regression coefficients.

D) allows for testing linear as well as nonlinear hypotheses.

A) allows for restrictions involving both multiple regression coefficients and single regression coefficients.

B) is F -distributed in large samples.

C) allows only for restrictions involving multiple regression coefficients.

D) allows for testing linear as well as nonlinear hypotheses.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

13

In the case when the errors are homoskedastic and normally distributed, conditional on X, then

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

14

A joint hypothesis that is linear in the coefficients and imposes a number of restrictions can be written as

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

15

Let there be q joint hypothesis to be tested. Then the dimension of r in the expression is

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

16

The GLS assumptions include all of the following, with the exception of

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

17

The linear multiple regression model can be represented in matrix notation as where X is of order n x(k+1) . k represents the number of

A) regressors.

B) observations.

C) regressors excluding the "constant" regressor for the intercept.

D) unknown regression coefficients

A) regressors.

B) observations.

C) regressors excluding the "constant" regressor for the intercept.

D) unknown regression coefficients

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

18

The Gauss-Markov theorem for multiple regression proves that

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

19

One of the properties of the OLS estimator is

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

20

A) cannot be calculated since the population parameter is unknown.

B)

C)

D)

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

21

Define the GLS estimator and discuss its properties when is known. Why is this estimator sometimes called infeasible GLS? What happens when is unknown? What would the matrix look like for the case of independent sampling with heteroskedastic errors, where

Since the inverse of the error variancecovariance matrix is needed to compute the GLS estimator, find https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/. The textbook shows that the original model

will be transformed into where

Find in the above case, and describe what effect the transformation has on the original data.

is known. Why is this estimator sometimes called infeasible GLS? What happens when is unknown? What would the matrix look like for the case of independent sampling with heteroskedastic errors, where Since the inverse of the error variancecovariance matrix is needed to compute the GLS estimator, find https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/

. The textbook shows that the original model will be transformed into

where Find

in the above case, and describe what effect the transformation has on the original data. Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

22

Write the following four restrictions in the form where the hypotheses are to be tested simultaneously.

Can you write the following restriction in the same format? Why not?

where the hypotheses are to be tested simultaneously.Can you write the following restriction

in the same format? Why not? Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

23

In Chapter 10 of your textbook, panel data estimation was introduced.Panel data consist

of observations on the same n entities at two or more time periods T.For two variables,

you have where n could be the U.S.states.The example in Chapter 10 used annual data from 1982

to 1988 for the fatality rate and beer taxes.Estimation by OLS, in essence, involved

"stacking" the data.

(a)What would the variance-covariance matrix of the errors look like in this case if you

allowed for homoskedasticity-only standard errors? What is its order? Use an example of

a linear regression with one regressor of 4 U.S.states and 3 time periods.

of observations on the same n entities at two or more time periods T.For two variables,

you have

where n could be the U.S.states.The example in Chapter 10 used annual data from 1982to 1988 for the fatality rate and beer taxes.Estimation by OLS, in essence, involved

"stacking" the data.

(a)What would the variance-covariance matrix of the errors look like in this case if you

allowed for homoskedasticity-only standard errors? What is its order? Use an example of

a linear regression with one regressor of 4 U.S.states and 3 time periods.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

24

q = 5 +3 p - 2 yq = 10 - p + 10 y

p = 6 y

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

25

The leading example of sampling schemes in econometrics that do not result in independent observations is

A)cross-sectional data.

B)experimental data.

C)the Current Population Survey.

D)when the data are sampled over time for the same entity.

A)cross-sectional data.

B)experimental data.

C)the Current Population Survey.

D)when the data are sampled over time for the same entity.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

26

Using the model and the extended least squares assumptions, derive the OLS estimator https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/. Discuss the conditions under which is invertible.

and the extended least squares assumptions, derive the OLS estimator https://d2lvgg3v3hfg70.cloudfront.net/TB34225555/. Discuss the conditions under which is invertible. Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

27

Consider the multiple regression model from Chapter 5, where k = 2 and the assumptions

of the multiple regression model hold.

(a)Show what the X matrix and the vector would look like in this case.

of the multiple regression model hold.

(a)Show what the X matrix and the

vector would look like in this case. Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

28

Prove that under the extended least squares assumptions the OLS estimator is unbiased and that its variance-covariance matrix is

is unbiased and that its variance-covariance matrix is Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

29

Assume that the data looks as follows:

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

30

The presence of correlated error terms creates problems for inference based on OLS. These can be overcome by

A)using HAC standard errors.

B)using heteroskedasticity-robust standard errors.

C)reordering the observations until the correlation disappears.

D)using homoskedasticity-only standard errors.

A)using HAC standard errors.

B)using heteroskedasticity-robust standard errors.

C)reordering the observations until the correlation disappears.

D)using homoskedasticity-only standard errors.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

31

The GLS estimator

A)is always the more efficient estimator when compared to OLS.

B)is the OLS estimator of the coefficients in a transformed model, where the errors of the transformed model satisfy the Gauss-Markov conditions.

C)cannot handle binary variables, since some of the transformations require division by one of the regressors.

D)produces identical estimates for the coefficients, but different standard errors.

A)is always the more efficient estimator when compared to OLS.

B)is the OLS estimator of the coefficients in a transformed model, where the errors of the transformed model satisfy the Gauss-Markov conditions.

C)cannot handle binary variables, since some of the transformations require division by one of the regressors.

D)produces identical estimates for the coefficients, but different standard errors.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

32

In order for a matrix A to have an inverse, its determinant cannot be zero.Derive the

determinant of the following matrices:

determinant of the following matrices:

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

33

Your textbook derives the OLS estimator as Show that the estimator does not exist if there are fewer observations than the number of

explanatory variables, including the constant.What is the rank of X′X in this case?

Show that the estimator does not exist if there are fewer observations than the number ofexplanatory variables, including the constant.What is the rank of X′X in this case?

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

34

Given the following matrices

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

35

For the OLS estimator to exist, must be invertible. This is the case when has full rank. What is the rank of a matrix? What is the rank of the product of two matrices? Is it possible that could have rank n ? What would be the rank of in the case Explain intuitively why the OLS estimator does not exist in that situation.

to exist, must be invertible. This is the case when has full rank. What is the rank of a matrix? What is the rank of the product of two matrices? Is it possible that could have rank n ? What would be the rank of in the case Explain intuitively why the OLS estimator does not exist in that situation. Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

36

An estimator of is said to be linear if

A) it can be estimated by least squares.

B) it is a linear function of

C) there are homoskedasticity-only errors.

D) it is a linear function of

A) it can be estimated by least squares.

B) it is a linear function of

C) there are homoskedasticity-only errors.

D) it is a linear function of

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

37

Give several economic examples of how to test various joint linear hypotheses using matrix notation. Include specifications of where you test for (i) all coefficients other than the constant being zero, (ii) a subset of coefficients being zero, and (iii) equality of coefficients. Talk about the possible distributions involved in finding critical values for your hypotheses.

where you test for (i) all coefficients other than the constant being zero, (ii) a subset of coefficients being zero, and (iii) equality of coefficients. Talk about the possible distributions involved in finding critical values for your hypotheses. Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

38

Write an essay on the difference between the OLS estimator and the GLS estimator.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 38 flashcards in this deck.