Deck 16: Non-Slg Not-For-Profit Organizations

Full screen (f)

Question

Question

Question

Statement of Activity for a Nongovernmental, Not-for-Profit Organization

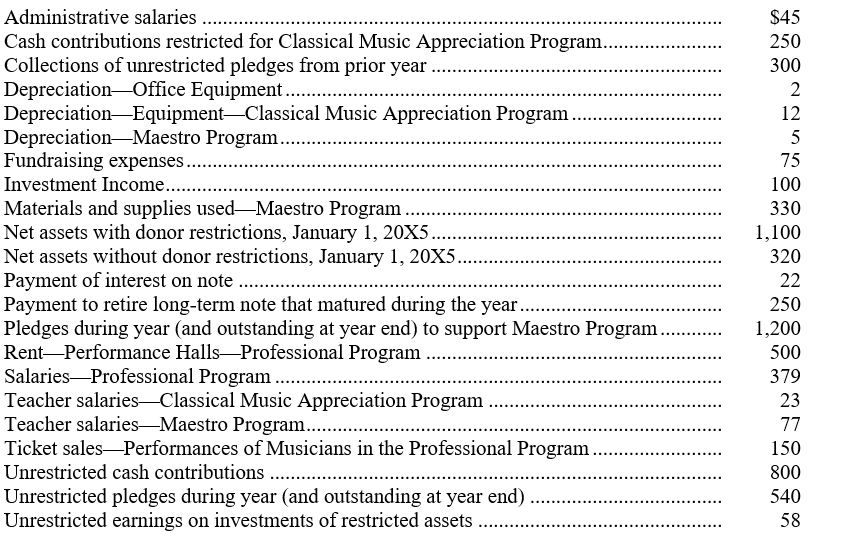

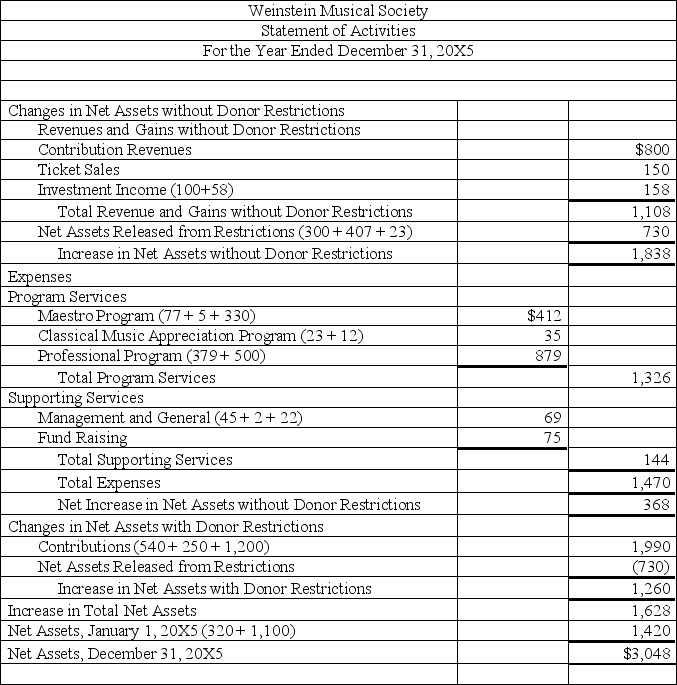

Selected information from the accounts of the Weinstein Musical Society, a nongovernment, not-for-profit organization for the year ended December 31, 20X5 is presented below. (All amounts are in thousands of dollars and all accounts have a normal balance):

All expenses of the Maestro and the Classical Music Appreciation Programs are payable from donor restricted resources.

Prepare the Statement of Activity for the Society

Selected information from the accounts of the Weinstein Musical Society, a nongovernment, not-for-profit organization for the year ended December 31, 20X5 is presented below. (All amounts are in thousands of dollars and all accounts have a normal balance):

All expenses of the Maestro and the Classical Music Appreciation Programs are payable from donor restricted resources.

Prepare the Statement of Activity for the Society

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 16: Non-Slg Not-For-Profit Organizations

1

Nongovernment not-for profit organizations that wish to follow generally accepted accounting principles in the preparation of their financial statements should follow

A) FASB standards.

B) GASB standards.

C) Nonprofit Accounting Standards Board (NASB) standards.

D) AICPA Audit and Accounting Guide, "Not-for-Profit Entities.

A) FASB standards.

B) GASB standards.

C) Nonprofit Accounting Standards Board (NASB) standards.

D) AICPA Audit and Accounting Guide, "Not-for-Profit Entities.

A

2

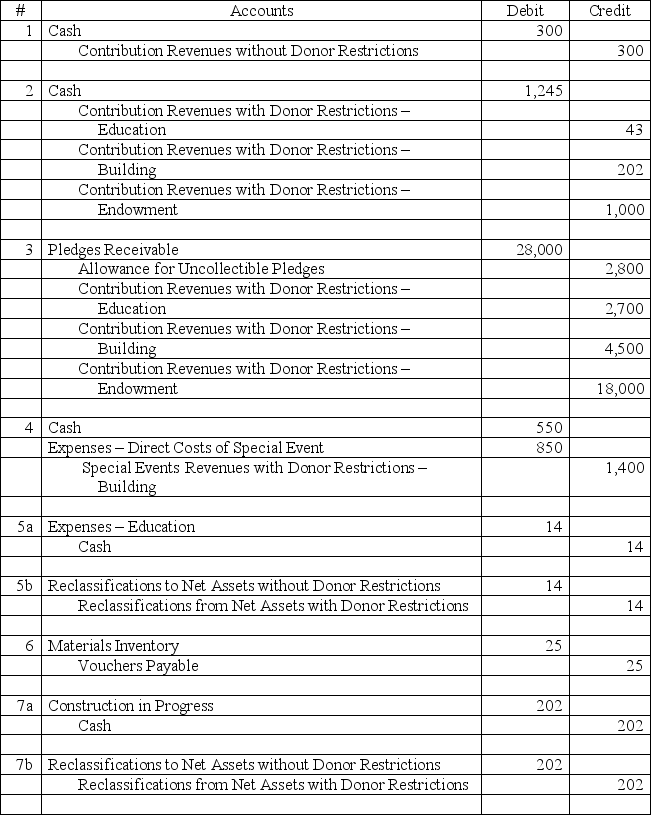

The following selected transactions occurred for a nongovernmental, not-for-profit organization. All amounts are in thousands of dollars.

1. Unrestricted cash contributions received during the year, $300.

2. Restricted cash contributions were received during the year for the following: (a) Education programs, $43; (b) Building fund, $202; and (c) Endowment, $1,000.

3. Pledges received during the year were as follows: Unrestricted, $3,000; (b) Building fund, $5,000; and (c) Endowment, $20,000. 10% of pledges receivable typically prove uncollectible. Pledges expect to be collected early in the next year.

4. A benefit concert was held to raise resources for the building fund. Receipts totaled $1,400 and direct costs incurred totaled $850.

5. Salary expenses incurred for the education programs were paid, $14.

6. Materials were purchased on account for the education programs, $25.

7. Fees paid to an architect for design of the building during the year were $92. Additionally, payments to the building contractor during the year were $110.

8. Earnings on endowment fund investments are restricted to the entity's education programs. The earnings for the year were $13.

9. Cost of materials used for education programs during the year, $32

10. Earnings on building fund investments were not restricted by donors but the board requires that they be used to finance the building. The earnings on those investments for the year were $25.

Prepare the journal entries for the above transactions.

1. Unrestricted cash contributions received during the year, $300.

2. Restricted cash contributions were received during the year for the following: (a) Education programs, $43; (b) Building fund, $202; and (c) Endowment, $1,000.

3. Pledges received during the year were as follows: Unrestricted, $3,000; (b) Building fund, $5,000; and (c) Endowment, $20,000. 10% of pledges receivable typically prove uncollectible. Pledges expect to be collected early in the next year.

4. A benefit concert was held to raise resources for the building fund. Receipts totaled $1,400 and direct costs incurred totaled $850.

5. Salary expenses incurred for the education programs were paid, $14.

6. Materials were purchased on account for the education programs, $25.

7. Fees paid to an architect for design of the building during the year were $92. Additionally, payments to the building contractor during the year were $110.

8. Earnings on endowment fund investments are restricted to the entity's education programs. The earnings for the year were $13.

9. Cost of materials used for education programs during the year, $32

10. Earnings on building fund investments were not restricted by donors but the board requires that they be used to finance the building. The earnings on those investments for the year were $25.

Prepare the journal entries for the above transactions.

3

Statement of Activity for a Nongovernmental, Not-for-Profit Organization

Selected information from the accounts of the Weinstein Musical Society, a nongovernment, not-for-profit organization for the year ended December 31, 20X5 is presented below. (All amounts are in thousands of dollars and all accounts have a normal balance):

All expenses of the Maestro and the Classical Music Appreciation Programs are payable from donor restricted resources.

Prepare the Statement of Activity for the Society

Selected information from the accounts of the Weinstein Musical Society, a nongovernment, not-for-profit organization for the year ended December 31, 20X5 is presented below. (All amounts are in thousands of dollars and all accounts have a normal balance):

All expenses of the Maestro and the Classical Music Appreciation Programs are payable from donor restricted resources.

Prepare the Statement of Activity for the Society

Solution assumes that depreciation does not satisfy any restrictions on resources use.

Solution assumes that depreciation does not satisfy any restrictions on resources use. 4

A nongovernment voluntary health and welfare organization received unrestricted cash donations of $23,000 for the current year, $30,000 of pledges to be received in and used for general purposes in the following year, and a $100,000 donation to establish a permanent investment endowment. The organization should report

A) Revenues without donor restrictions of $53,000 and revenues with donor restrictions of $100,000.

B) Revenues with donor restrictions of $153,000.

C) Revenues without donor restrictions of $23,000, net assets released from restrictions of $30,000, and revenues with donor restrictions of $100,000.

D) Revenues without donor restrictions of $23,000 and revenues with donor restrictions of $130,000.

A) Revenues without donor restrictions of $53,000 and revenues with donor restrictions of $100,000.

B) Revenues with donor restrictions of $153,000.

C) Revenues without donor restrictions of $23,000, net assets released from restrictions of $30,000, and revenues with donor restrictions of $100,000.

D) Revenues without donor restrictions of $23,000 and revenues with donor restrictions of $130,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

Fund-raising expenses are classified as

A) Program services expenses.

B) Supporting services expenses.

C) Management and general expenses.

D) Nonoperating expenses.

A) Program services expenses.

B) Supporting services expenses.

C) Management and general expenses.

D) Nonoperating expenses.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

Membership dues of nongovernment, not-for-profit organizations are

A) Always treated as exchange transactions and reported as revenues.

B) Always treated as contribution revenues.

C) Permitted to be reported either as exchange revenues or as contributions revenues depending on the organization's preference.

D) Reported as contribution revenues if no benefits are received as a result of membership.

A) Always treated as exchange transactions and reported as revenues.

B) Always treated as contribution revenues.

C) Permitted to be reported either as exchange revenues or as contributions revenues depending on the organization's preference.

D) Reported as contribution revenues if no benefits are received as a result of membership.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

A nongovernment, not-for-profit organization provides the following information and asks you to determine how much revenue should be reported in each of its changes in net assets categories. All pledges are unconditional

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

A not-for-profit organization was the recipient of a significant fixed asset donation. The assets, a building valued at $82,000, and one acre of land, valued at $210,000, are going to be used by the organization for office space and parking. The donor's net book value of the building was $22,000, and of the land, $65,000. The not-for-profit organization should record the assets at a total value of

A) $87,000.

B) $104,000.

C) $147,000.

D) $292,000.

A) $87,000.

B) $104,000.

C) $147,000.

D) $292,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

Other not-for-profit organizations include

A) Hospitals.

B) Colleges and universities.

C) Religious organizations.

D) Voluntary health and welfare organizations.

A) Hospitals.

B) Colleges and universities.

C) Religious organizations.

D) Voluntary health and welfare organizations.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

The following selected transactions occurred for a nongovernment, not-for-profit organization. All amounts are in thousands of dollars.

1. Received a contribution of stock to establish an endowment fund. The income from the endowment is unrestricted. The donor had acquired the stock for $23 about 20 years earlier. Its estimated fair value when donated was $250.

2. Pledges receivable at year end were $100, all from pledges received during the year. The pledges are unrestricted and 5% of the pledges are estimated to be uncollectible. The pledges expect to be collected early next year.

For questions 3-5, assume that the organization has adopted a policy that restrictions on donations made for capital purposes are met when the capital item is purchased.

3. A cash gift of $200 was received restricted for the purchase of equipment.

4. Equipment of $80 was purchased from the gift restricted for this purpose.

5. Depreciation expense for the year on the equipment purchased is $10.

Prepare the journal entries for the above transactions.

1. Received a contribution of stock to establish an endowment fund. The income from the endowment is unrestricted. The donor had acquired the stock for $23 about 20 years earlier. Its estimated fair value when donated was $250.

2. Pledges receivable at year end were $100, all from pledges received during the year. The pledges are unrestricted and 5% of the pledges are estimated to be uncollectible. The pledges expect to be collected early next year.

For questions 3-5, assume that the organization has adopted a policy that restrictions on donations made for capital purposes are met when the capital item is purchased.

3. A cash gift of $200 was received restricted for the purchase of equipment.

4. Equipment of $80 was purchased from the gift restricted for this purpose.

5. Depreciation expense for the year on the equipment purchased is $10.

Prepare the journal entries for the above transactions.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

A not-for-profit organization receives donated supplies valued at $40,000 in June. As of the fiscal year end December, 31, 20X3, the organization had used 25% of the materials. The organization should report

A) Restricted contributions of $40,000 and no expenses.

B) Restricted contributions and expenses of $40,000.

C) Unrestricted contributions of $40,000 and expenses of $10,000.

D) Unrestricted contributions of $10,000 and no expenses.

A) Restricted contributions of $40,000 and no expenses.

B) Restricted contributions and expenses of $40,000.

C) Unrestricted contributions of $40,000 and expenses of $10,000.

D) Unrestricted contributions of $10,000 and no expenses.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

Nongovernment not-for-profit organizations are required to report their financial statements on

A) A current financial resources measurement focus.

B) An economic resources measurement focus.

C) A cash measurement focus.

D) A modified accrual measurement focus.

A) A current financial resources measurement focus.

B) An economic resources measurement focus.

C) A cash measurement focus.

D) A modified accrual measurement focus.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

A private school is given $40,000 to permanently endow one of its education programs. A debit of $40,000 should be made to

A) Cash.

B) Unrestricted cash.

C) Temporarily restricted cash.

D) Cash restricted for endowment.

A) Cash.

B) Unrestricted cash.

C) Temporarily restricted cash.

D) Cash restricted for endowment.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

The line item, net assets released from restrictions, may be reported in a nongovernment, not-for-profit organization's statement of activities in which classifications?

A) Changes in net assets with donor restrictions only.

B) Changes in net assets without donor restrictions and changes in net assets with donor restrictions.

C) Changes in unrestricted net assets and changes in permanently restricted net assets.

D) Changes in unrestricted net assets, changes in temporarily restricted net assets, and/or changes in permanently restricted net assets.

A) Changes in net assets with donor restrictions only.

B) Changes in net assets without donor restrictions and changes in net assets with donor restrictions.

C) Changes in unrestricted net assets and changes in permanently restricted net assets.

D) Changes in unrestricted net assets, changes in temporarily restricted net assets, and/or changes in permanently restricted net assets.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

Reporting for Not-for-Profit Organizations

Explain the way a nongovernmental, not-for-profit organization must report the following items in its statement of activities:

A. Receipt of unrestricted contributions

B. Pledges restricted to a specific program

C. Collections, in a subsequent year, of pledges restricted to a specific purpose

D. Pledges restricted to fixed asset construction

E. Earnings on restricted investments

Explain the way a nongovernmental, not-for-profit organization must report the following items in its statement of activities:

A. Receipt of unrestricted contributions

B. Pledges restricted to a specific program

C. Collections, in a subsequent year, of pledges restricted to a specific purpose

D. Pledges restricted to fixed asset construction

E. Earnings on restricted investments

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

A nongovernment not-for-profit organization received donated services from a local volunteer. The volunteer works as a receptionist for the organization. The market value of service is $5,000. How should this activity be reported be in the statement of activities?

A) Not be reported.

B) Unrestricted support, $5,000.

C) Restricted support, $5,000.

D) Both unrestricted support and program expense, $5,000.

A) Not be reported.

B) Unrestricted support, $5,000.

C) Restricted support, $5,000.

D) Both unrestricted support and program expense, $5,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

Listed below are two transactions for an alcohol rehabilitation treatment program. All amounts are in thousands of dollars.

1. Received pledges of $300 and cash gifts of $100 during the year to be used only for alcohol rehabilitation treatment programs.

2. Incurred expenses of $220 for its alcohol rehabilitation program but paid the expenses from unrestricted resources, not from available restricted resources.

Prepare the journal entries for these transactions.

1. Received pledges of $300 and cash gifts of $100 during the year to be used only for alcohol rehabilitation treatment programs.

2. Incurred expenses of $220 for its alcohol rehabilitation program but paid the expenses from unrestricted resources, not from available restricted resources.

Prepare the journal entries for these transactions.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

The statement of net assets for a nongovernment nonprofit organization would report the following components of net assets

A) Unrestricted net assets and net assets with donor restrictions.

B) Net assets without donor restrictions and temporarily restricted net assets.

C) Net investment in capital assets, restricted net assets, and unrestricted net assets.

D) Net assets without donor restrictions and net assets with donor restrictions.

A) Unrestricted net assets and net assets with donor restrictions.

B) Net assets without donor restrictions and temporarily restricted net assets.

C) Net investment in capital assets, restricted net assets, and unrestricted net assets.

D) Net assets without donor restrictions and net assets with donor restrictions.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

A not-for-profit entity that receives a donation restricted for a specific purpose and meets the use restriction in the same reporting period reports

A) Revenues without donor restrictions.

B) Revenues with donor restrictions and revenues without donor restrictions.

C)

C) Revenues with donor restrictions and net assets released from restrictions.

D) Either A or

A) Revenues without donor restrictions.

B) Revenues with donor restrictions and revenues without donor restrictions.

C)

C) Revenues with donor restrictions and net assets released from restrictions.

D) Either A or

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

Special fund-raising events of a nongovernment, not-for-profit organization

A) Must always be reported as revenues and at gross amounts.

B) Must always be reported as gains and at net amounts.

C) Must be reported as revenues at gross amounts or gains reported at net amounts.

D) Must be reported as revenues at gross amounts unless the event is incidental or peripheral.

A) Must always be reported as revenues and at gross amounts.

B) Must always be reported as gains and at net amounts.

C) Must be reported as revenues at gross amounts or gains reported at net amounts.

D) Must be reported as revenues at gross amounts unless the event is incidental or peripheral.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is true for a nongovernment, not-for-profit organization?

A) Revenues and expenses may be reported in changes in net assets without donor restrictions.

B) Revenues and expenses may be reported in changes in net assets with donor restrictions.

C) Expenses and net assets released from restrictions may be reported in changes in net assets with donor restrictions.

D) Expenses may be reported in changes in net assets without donor restrictions or in changes in net assets with donor restrictions.

A) Revenues and expenses may be reported in changes in net assets without donor restrictions.

B) Revenues and expenses may be reported in changes in net assets with donor restrictions.

C) Expenses and net assets released from restrictions may be reported in changes in net assets with donor restrictions.

D) Expenses may be reported in changes in net assets without donor restrictions or in changes in net assets with donor restrictions.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

A nongovernment not-for-profit organization received a cash donation restricted for construction of a new building. How should the donation be reported be reported in the statement of cash flows?

A) Cash inflows from operating activities.

B) Cash inflows from financing activities.

C) Cash inflows from investing activities.

D) Cash inflows from capital and related financing activities.

A) Cash inflows from operating activities.

B) Cash inflows from financing activities.

C) Cash inflows from investing activities.

D) Cash inflows from capital and related financing activities.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

The net realizable value or present value of unrestricted pledges receivable outstanding at the end of a year for a nongovernmental not-for-profit organization are

A) Always considered unrestricted net assets.

B) Always considered temporarily restricted net assets.

C) Always considered permanently restricted net assets.

D) Considered temporarily restricted unless the donor specified that the pledge was intended to finance current year expenses.

A) Always considered unrestricted net assets.

B) Always considered temporarily restricted net assets.

C) Always considered permanently restricted net assets.

D) Considered temporarily restricted unless the donor specified that the pledge was intended to finance current year expenses.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

24

Land valued at $100,000 was donated to a not-for-profit organization. The donation came with no restrictions. The organization's management decided to hold the land for resale and use the proceeds to establish a reserve for future capital needs. Which of the following journal entries would be made on the date of donation?

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

In 20X8, the following pledges were made: $35,000 in unrestricted contributions for use in 20X8; $20,000 in contributions restricted for use in 20X9; and a $400,000 contribution restricted for the establishment of a permanent endowment. It is anticipated that 10% of all pledges except the endowment pledge will be uncollectible. Pledges receivable for 20X8 should be

A) $455,000.

B) $449,500.

C) $55,000.

D) $49,500.

A) $455,000.

B) $449,500.

C) $55,000.

D) $49,500.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

With respect to collections, nongovernment not-for-profit organizations are

A) Required to capitalize all collections.

B) Prohibited from capitalizing collections.

C) Required to either capitalize all collections or to capitalize no collections.

D) Permitted to capitalize no collections, to capitalize all collections, or to capitalize only those collections acquired after the FASB adopted its original not-for-profit accounting standards.

A) Required to capitalize all collections.

B) Prohibited from capitalizing collections.

C) Required to either capitalize all collections or to capitalize no collections.

D) Permitted to capitalize no collections, to capitalize all collections, or to capitalize only those collections acquired after the FASB adopted its original not-for-profit accounting standards.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

A nongovernment not-for-profit organization received a cash donation of $100,000 restricted for a specific operating purpose. Only $20,000 of the donation was spent during the current year. How should the donation be reported be in the statement of activities?

A) Revenues without donor restrictions - $100,000.

B) Revenues without donor restrictions - $20,000.

C) Revenues with donor restrictions - $100,000.

D) Revenues with donor restrictions - $20,000.

A) Revenues without donor restrictions - $100,000.

B) Revenues without donor restrictions - $20,000.

C) Revenues with donor restrictions - $100,000.

D) Revenues with donor restrictions - $20,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

A nongovernment not-for-profit organization received a cash donation of $100,000 restricted for a specific operating purpose. Only $20,000 of expenses related to the specific operating purpose was incurred during the current year. How should this activity be reported be in the statement of activities?

A) Expenses in changes in net assets without donor restrictions, $20,000.

B) Expenses in changes in net assets with donor restrictions, $20,000.

C) Both revenues of $100,000 and expenses of $20,000 in changes in net assets without donor restrictions.

D) Both expenses and net assets released from restrictions of $20,000 in changes in net assets with donor restrictions.

A) Expenses in changes in net assets without donor restrictions, $20,000.

B) Expenses in changes in net assets with donor restrictions, $20,000.

C) Both revenues of $100,000 and expenses of $20,000 in changes in net assets without donor restrictions.

D) Both expenses and net assets released from restrictions of $20,000 in changes in net assets with donor restrictions.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following financial statements is not required for all nongovernment not-for-profit organizations?

A) Statement of net assets.

B) Statement of activities.

C) Statement of cash flows.

D) Statement of changes in assets and liabilities.

A) Statement of net assets.

B) Statement of activities.

C) Statement of cash flows.

D) Statement of changes in assets and liabilities.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

Computer equipment used in the business office of a not-for-profit organization was sold for $9,000. The original cost of the equipment had been $21,000 and there was $15,000 of accumulated depreciation as of the date of sale. How will the gain be reported?

A) Gains are not recognized in not-for-profit organizations.

B) Gain of $3,000 in changes in net assets without donor restrictions.

C) Gain of $3,000 in changes in net assets with donor restrictions.

D) Net assets released from restrictions of $3,000.

A) Gains are not recognized in not-for-profit organizations.

B) Gain of $3,000 in changes in net assets without donor restrictions.

C) Gain of $3,000 in changes in net assets with donor restrictions.

D) Net assets released from restrictions of $3,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

What costs may be deducted directly from revenues instead of being reported with the as other expenses?

A) Direct costs of special fund raising events.

B) Expenses for benefits provided in exchange for membership dues.

C) Fund raising expenses.

D) Depreciation expense.

A) Direct costs of special fund raising events.

B) Expenses for benefits provided in exchange for membership dues.

C) Fund raising expenses.

D) Depreciation expense.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

A nongovernment, not-for-profit environmental organization conducts a mailing about the dangers of global warming. Included in the mailing is a request for donations. How should this activity be reported be in the statement of activities?

A) Fund-raising expense.

B) Program expense.

C) Fund-raising, unless certain criteria are met.

D) Always allocated between fund-raising and program support.

A) Fund-raising expense.

B) Program expense.

C) Fund-raising, unless certain criteria are met.

D) Always allocated between fund-raising and program support.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

Fund raising expenses are reported as

A) Nonoperating expenses.

B) Operating expenses.

C) Program expenses.

D) Supporting services expenses.

A) Nonoperating expenses.

B) Operating expenses.

C) Program expenses.

D) Supporting services expenses.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

Investment earnings of $1,250 were earned on restricted investments. The earnings are to be used for various research projects during the current year. The earnings would be reported as

A) Revenues without donor restrictions.

B) Revenues with donor restrictions.

C) Net assets released from restrictions.

D) Revenues from donations.

A) Revenues without donor restrictions.

B) Revenues with donor restrictions.

C) Net assets released from restrictions.

D) Revenues from donations.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

How should a nongovernment not-for-profit organization generally report increases in the fair value of marketable debt securities in its statement of activities?

A) Such increases in fair value should not be reported because debt securities are reported at amortized cost.

B) As an increase in net assets with donor restrictions

C) As an increase in net assets without donor restrictions

D) As an increase in net assets without donor restrictions, unless restricted by donor stipulation or law

A) Such increases in fair value should not be reported because debt securities are reported at amortized cost.

B) As an increase in net assets with donor restrictions

C) As an increase in net assets without donor restrictions

D) As an increase in net assets without donor restrictions, unless restricted by donor stipulation or law

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

A nongovernment not-for-profit organization statement of activities reports

A) Only changes in net assets without donor restrictions.

B) Only changes in net assets without donor restrictions that are revenues, expenses, gains, or losses.

C) Both changes in net assets without donor restrictions and changes in net assets with donor restrictions.

D) Only changes in total net assets.

A) Only changes in net assets without donor restrictions.

B) Only changes in net assets without donor restrictions that are revenues, expenses, gains, or losses.

C) Both changes in net assets without donor restrictions and changes in net assets with donor restrictions.

D) Only changes in total net assets.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

A nongovernment, not-for-profit organization received $5,000,000 of unconditional pledges during 2013 that had not been collected by year end. In its 2013 statement of activities, the organization should recognize

A) No revenues, but should report receivables and deferred revenues in its balance sheet.

B) Revenues without donor restrictions of $5,000,000.

C) Revenues with donor restrictions of $5,000,000.

D) Other financing sources of $5,000,000.

A) No revenues, but should report receivables and deferred revenues in its balance sheet.

B) Revenues without donor restrictions of $5,000,000.

C) Revenues with donor restrictions of $5,000,000.

D) Other financing sources of $5,000,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

Nongovernment not-for-profit organizations recognize revenues when

A) Pledges are measurable and available.

B) Unconditional pledges become due.

C) Unconditional pledges are made by donors, even if not yet collected.

D) Unconditional pledges are made by donors and qualifying costs have been incurred.

A) Pledges are measurable and available.

B) Unconditional pledges become due.

C) Unconditional pledges are made by donors, even if not yet collected.

D) Unconditional pledges are made by donors and qualifying costs have been incurred.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

Nongovernment, not-for-profit organizations use the following classifications to report expenses in the statement of activities

A) Changes in net assets without donor restrictions and changes in net assets with donor restrictions.

B) Operating and nonoperating.

C) Management and general and supporting services.

D) Mission critical, non-mission-critical, and discretionary.

A) Changes in net assets without donor restrictions and changes in net assets with donor restrictions.

B) Operating and nonoperating.

C) Management and general and supporting services.

D) Mission critical, non-mission-critical, and discretionary.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

Pledges should be reported by a nongovernment not-for-profit organization as revenues in the period that they are unconditionally received

A) By the organization.

B) By the organization if the pledges are unrestricted.

C) By the organization if the pledges are unrestricted and have been collected by year end.

D) If the organization has incurred qualifying costs.

A) By the organization.

B) By the organization if the pledges are unrestricted.

C) By the organization if the pledges are unrestricted and have been collected by year end.

D) If the organization has incurred qualifying costs.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.