Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

النسخة 3الرقم المعياري الدولي: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

النسخة 3الرقم المعياري الدولي: 978-9352863501 تمرين 13

Consider the regression model in matrix form

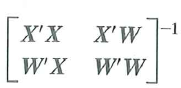

where X and W are matrices of regressors and ß and are vectors of unknown regression coefficients. Let

where X and W are matrices of regressors and ß and are vectors of unknown regression coefficients. Let

where

where

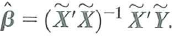

a. Show that the OLS estimators of ß and can be written as

b. Show that

=

=

c. Show that

d. The Frisch-Waugh theorem (Appendix 6.2) says that

Use the result in (c) to prove the Frisch-Waugh theorem.

Use the result in (c) to prove the Frisch-Waugh theorem.

where X and W are matrices of regressors and ß and are vectors of unknown regression coefficients. Let where a. Show that the OLS estimators of ß and can be written as

b. Show that

= c. Show that

d. The Frisch-Waugh theorem (Appendix 6.2) says that

Use the result in (c) to prove the Frisch-Waugh theorem.التوضيح موثّق

موثّق

The given regression equation in matrix ...

Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255