The neoclassical growth model predicts that for identical savings rates and population growth rates,countries should converge to the per capita income level.This is referred to as the convergence hypothesis.One way to test for the presence of convergence is to compare the growth rates over time to the initial starting level,i.e. ,to run the regression  =

=  +

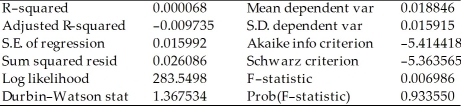

+  × RelProd60 ,where g6090 is the average annual growth rate of GDP per worker for the 1960-1990 sample period,and RelProd60 is GDP per worker relative to the United States in 1960.Under the null hypothesis of no convergence,β1 = 0;H1 : β1 < 0,implying ("beta")convergence.Using a standard regression package,you get the following output:

× RelProd60 ,where g6090 is the average annual growth rate of GDP per worker for the 1960-1990 sample period,and RelProd60 is GDP per worker relative to the United States in 1960.Under the null hypothesis of no convergence,β1 = 0;H1 : β1 < 0,implying ("beta")convergence.Using a standard regression package,you get the following output:

Dependent Variable: G6090

Method: Least Squares

Date: 07/11/06 Time: 05:46

Sample: 1 104

Included observations: 104

White Heteroskedasticity-Consistent Standard Errors & Covariance

You are delighted to see that this program has already calculated p-values for you.However,a peer of yours points out that the correct p-value should be 0.4562.Who is right?

You are delighted to see that this program has already calculated p-values for you.However,a peer of yours points out that the correct p-value should be 0.4562.Who is right?

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q45: Assume that the homoskedastic normal regression assumption

Q49: Consider the following two models involving binary

Q50: (Requires Appendix material and Calculus)Equation (5.36)in your

Q51: Below you are asked to decide on

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents