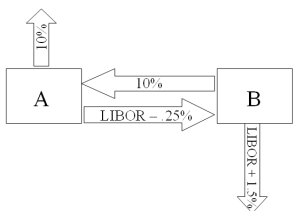

Compute the payments due in the second year on a three-year AMORTIZING swap from company B to company A) Company A and company B both want to borrow £1,000,000 for three years.A wants to borrow floating and B wants to borrow fixed.A and B agree to split the QSD.

A) B pays £402,114.80 to A

B) B pays £100,000 to A

C) B pays £69,788.52 to A

D) None of the above

Correct Answer:

Verified

Q23: Suppose ABC Investment Banker,Ltd.is quoting swap rates

Q24: Company X wants to borrow $10,000,000 floating

Q25: Consider the dollar- and euro-based borrowing opportunities

Q26: A is a U.S.-based MNC with AAA

Q29: Compute the payments due in the FIRST

Q30: Consider the dollar- and euro-based borrowing opportunities

Q31: Company X wants to borrow $10,000,000 floating

Q32: Company X wants to borrow $10,000,000 for

Q33: Use the following information to calculate the

Q39: Pricing a currency swap after inception involves

A)finding

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents