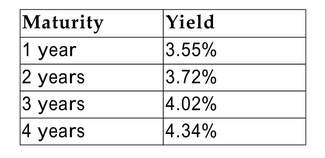

Consider the following term structure:  Assume you expect the interest rate on a 1-year Treasury security issued one year

Assume you expect the interest rate on a 1-year Treasury security issued one year

from today to be 4.0%. Describe the trades that you would make to earn a profit if you

are correct, assuming you are able to short sell securities and invest the proceeds from

the short sale immediately. Give an example.

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q56: A 1-year bond is yielding 7.4%, and

Q57: The following yields were reported for Treasury

Q58: Empirical evidence suggests that the reason that

Q59: The following yields were reported for Treasury

Q60: In which of the following two bonds

Q61: A $10,000 Treasury bill that matures in

Q62: What is the Macaulay duration of a

Q63: What continuously compounded rate is equivalent to

Q64: Calculate the Macaulay duration of a $1,000,

Q66: If you invest $1,000 at 6%, compounded

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents