Deck 6: Variable Costing and Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

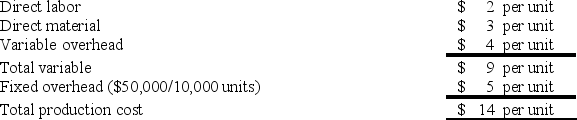

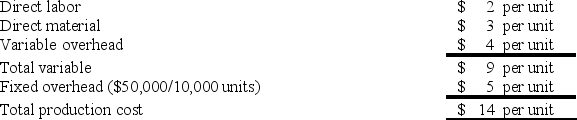

Under absorption costing, a company had the following unit costs when 10,000 units were produced:

The total product cost per unit under absorption costing if 25,000 units had been produced would be $11.

The total product cost per unit under absorption costing if 25,000 units had been produced would be $11.

The total product cost per unit under absorption costing if 25,000 units had been produced would be $11. سؤال

Assume a company had the following production costs:

Under absorption costing, the total product cost per unit when 4,000 units are produced would be $22.50.

Under absorption costing, the total product cost per unit when 4,000 units are produced would be $22.50.

Under absorption costing, the total product cost per unit when 4,000 units are produced would be $22.50. سؤال

سؤال

Given the following data, total product cost per unit under absorption costing is $11.40.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Given the following data, total product cost per unit under absorption costing is $9.14.

سؤال

سؤال

Given the following data, total product cost per unit under variable costing is $7.09.

سؤال

Given the following data, total product cost per unit under absorption costing will be $400 greater than total product cost per unit under variable costing.

سؤال

سؤال

سؤال

Given the following data, total product cost per unit under variable costing is $10.75.

سؤال

سؤال

سؤال

Given the following data, total product cost per unit under variable costing will be greater than total product cost under absorption costing.

سؤال

سؤال

سؤال

Given the following data, total product cost per unit under absorption costing will be greater than total product cost per unit under variable costing.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

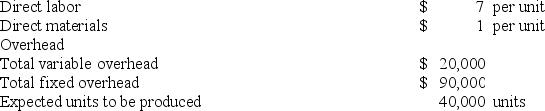

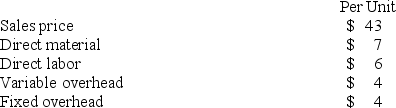

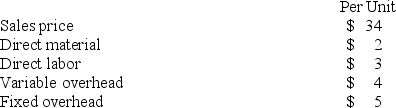

A company is currently operating at 75% capacity and producing 3,000 units. Current cost information relating to this production is shown in the table below:  The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

A) Any amount over $43 per unit.

B) Any amount over $17 per unit.

C) Any amount over $21 per unit.

D) Any amount over $13 per unit.

E) Any amount over $22 per unit.

The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?A) Any amount over $43 per unit.

B) Any amount over $17 per unit.

C) Any amount over $21 per unit.

D) Any amount over $13 per unit.

E) Any amount over $22 per unit.

سؤال

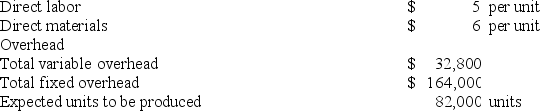

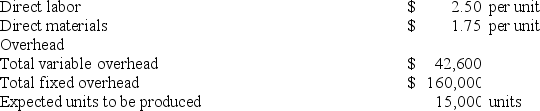

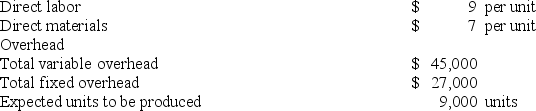

Under absorption costing, a company had the following unit costs when 9,000 units were produced.  Compute the total product cost per unit under variable costing if 30,000 units had been produced.

Compute the total product cost per unit under variable costing if 30,000 units had been produced.

A) $31.75

B) $28.25

C) $23.45

D) $15.25

E) $20.75

Compute the total product cost per unit under variable costing if 30,000 units had been produced.A) $31.75

B) $28.25

C) $23.45

D) $15.25

E) $20.75

سؤال

سؤال

سؤال

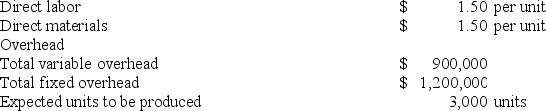

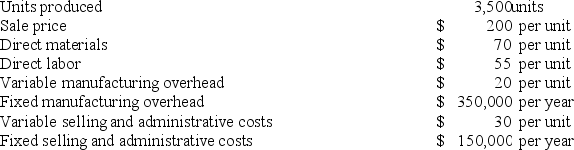

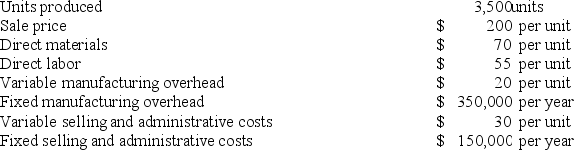

Mentor Corp. has provided the following information for the current year:  Calculate the unit product cost using variable costing.

Calculate the unit product cost using variable costing.

A) $245

B) $275

C) $55

D) $145

E) $125

Calculate the unit product cost using variable costing.A) $245

B) $275

C) $55

D) $145

E) $125

سؤال

Mentor Corp. has provided the following information for the current year:  Calculate the unit product cost using absorption costing.

Calculate the unit product cost using absorption costing.

A) $245

B) $275

C) $55

D) $145

E) $125

Calculate the unit product cost using absorption costing.A) $245

B) $275

C) $55

D) $145

E) $125

سؤال

سؤال

Under absorption costing, a company had the following unit costs when 9,000 units were produced.  Compute the total product cost per unit under absorption costing if 25,000 units had been produced.

Compute the total product cost per unit under absorption costing if 25,000 units had been produced.

A) $28.25

B) $23.45

C) $26.25

D) $20.75

E) $15.25

Compute the total product cost per unit under absorption costing if 25,000 units had been produced.A) $28.25

B) $23.45

C) $26.25

D) $20.75

E) $15.25

سؤال

سؤال

Geneva Company manufactures dolls that are sold to various customers. The company works at full capacity for half the year to meet peak demand, and operates at 80% capacity for the other half of the year. The following information is provided:  Geneva receives a purchase order to make 5,000 dolls as a one-time event. The good news is that this order is during a period when Geneva does have sufficient excess capacity. What is the lowest selling price Geneva should accept for this purchase order?

Geneva receives a purchase order to make 5,000 dolls as a one-time event. The good news is that this order is during a period when Geneva does have sufficient excess capacity. What is the lowest selling price Geneva should accept for this purchase order?

A) $35.00

B) $26.00

C) $29.50

D) $23.50

E) $25.00

Geneva receives a purchase order to make 5,000 dolls as a one-time event. The good news is that this order is during a period when Geneva does have sufficient excess capacity. What is the lowest selling price Geneva should accept for this purchase order?A) $35.00

B) $26.00

C) $29.50

D) $23.50

E) $25.00

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

A company is currently operating at 80% capacity producing 5,000 units. Current cost information relating to this production is shown in the table below:  The company has been approached by a customer with a request for a 100-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

The company has been approached by a customer with a request for a 100-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

A) Any amount over $34 per unit.

B) Any amount over $20 per unit.

C) Any amount over $14 per unit.

D) Any amount over $9 per unit.

E) Any amount over $5 per unit.

The company has been approached by a customer with a request for a 100-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?A) Any amount over $34 per unit.

B) Any amount over $20 per unit.

C) Any amount over $14 per unit.

D) Any amount over $9 per unit.

E) Any amount over $5 per unit.

سؤال

سؤال

سؤال

سؤال

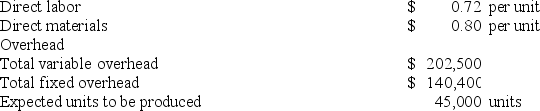

Under absorption costing, a company had the following unit costs when 8,000 units were produced.  Compute the total production cost per unit under variable costing if 25,000 units had been produced.

Compute the total production cost per unit under variable costing if 25,000 units had been produced.

A) $31.75

B) $27.25

C) $26.25

D) $24.25

E) $17.50

Compute the total production cost per unit under variable costing if 25,000 units had been produced.A) $31.75

B) $27.25

C) $26.25

D) $24.25

E) $17.50

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/202

العب

ملء الشاشة (f)

Deck 6: Variable Costing and Analysis

1

The absorption costing approach assigns all manufacturing costs to products.

True

2

When there are zero units in beginning Finished Goods Inventory and more units are produced than sold, the income will be lower under variable costing than under absorption costing.

True

3

Variable costing is required by Generally Accepted Accounting Principles (GAAP) for financial statement purposes.

False

4

For short-term pricing decisions, absorption costing is an appropriate costing method to use.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

5

Many companies link manager bonuses to income computed under absorption costing because this is how income is reported to shareholders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

6

Variable costing treats fixed overhead cost as a period cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

7

Managers should accept special orders provided the special order price exceeds the product cost per unit under absorption costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

8

When the number of units produced is equal to the number of units sold, net income reported under variable costing is identical to net income reported under absorption costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

9

Absorption costing is required under GAAP.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

10

Evaluating and rewarding managers based on absorption costing income can lead to overproduction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

11

Under variable costing, product costs consist of direct labor, direct materials, and fixed overhead.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

12

Since fixed costs remain constant in the short run, special orders should be accepted as long as the order price is greater than the variable costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

13

Cost information from both absorption costing and variable costing can aid managers in pricing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

14

The biggest problems with producing too much are lost sales and customer dissatisfaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

15

The use of absorption costing can result in misleading product cost information.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

16

Under variable costing, product costs consist of direct labor, direct materials, and variable overhead.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

17

Absorption costing is useful because it reflects the full costs that sales must exceed for the company to be profitable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

18

When setting long-term sales prices for products, the sales price must cover all costs, including fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

19

Under absorption costing, a company had the following unit costs when 10,000 units were produced:

The total product cost per unit under absorption costing if 25,000 units had been produced would be $11.

The total product cost per unit under absorption costing if 25,000 units had been produced would be $11. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

20

Assume a company had the following production costs:

Under absorption costing, the total product cost per unit when 4,000 units are produced would be $22.50.

Under absorption costing, the total product cost per unit when 4,000 units are produced would be $22.50. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

21

The data needed for cost-volume-profit analysis is readily available if the income statement is prepared under absorption costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

22

Given the following data, total product cost per unit under absorption costing is $11.40.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

23

The data needed for cost-volume-profit analysis is readily available if the income statement is prepared using a contribution format.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

24

A company normally sells a product for $20 per unit. Variable per unit costs for this product are: $2 direct materials, $4 direct labor, and $1.50 variable overhead. The company is currently operating at 70% of capacity producing 14,000 units per year. Total fixed costs are $42,000 per year. The company should not accept a special order for 2,000 units which would be sold for $10 per unit because there would be an incremental loss on the order.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

25

Assuming fixed costs remain constant, and a company produces more units than it sells, then income under absorption costing is less than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

26

Fixed costs change in the short run depending upon management's decision to accept or reject special orders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

27

Assuming fixed costs remain constant, and a company produces and sells the same number of units, then income under absorption costing is less than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

28

Given the following data, total product cost per unit under absorption costing is $9.14.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

29

Absorption costing is usually used for internal management purposes, and variable costing is usually used for external reporting purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

30

Given the following data, total product cost per unit under variable costing is $7.09.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

31

Given the following data, total product cost per unit under absorption costing will be $400 greater than total product cost per unit under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

32

If a company has excess capacity, increases in production level will increase variable production costs but not fixed production costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

33

Variable costing separates variable costs from fixed costs and therefore makes it easier to identify and assign control over costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

34

Given the following data, total product cost per unit under variable costing is $10.75.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

35

A company normally sells a product for $25 per unit. Variable per unit costs for this product are: $3 direct materials, $5 direct labor, and $2 variable overhead. The company is currently operating at 100% of capacity producing 30,000 units per year. Total fixed costs are $75,000 per year. The company should accept a special order for 1,000 units which would be sold for $13 per unit because the special order price exceeds variable costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

36

The traditional income statement format used for financial reporting is called the contribution margin format.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

37

Given the following data, total product cost per unit under variable costing will be greater than total product cost under absorption costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

38

Assuming fixed costs remain constant, and a company sells more units than it produces, then income under absorption costing is less than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

39

The variable costing income statement classifies costs based on cost behavior rather than function.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

40

Given the following data, total product cost per unit under absorption costing will be greater than total product cost per unit under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

41

Which of the following costing methods charges all manufacturing costs to its products?

A) Direct costing

B) ABC costing

C) Variable costing

D) Absorption costing

E) Period costing

A) Direct costing

B) ABC costing

C) Variable costing

D) Absorption costing

E) Period costing

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

42

The bottom line of a contribution margin report is net income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

43

Information presented in a variable costing format can assist management when making short-term pricing decisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

44

Reporting contribution margin by market segment is useful in assessing the profitability of each segment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

45

Under absorption costing, fixed manufacturing overhead is expensed at the time the units are produced. Under variable costing, fixed manufacturing overhead is expensed at the time the units are sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

46

Contribution margin is the excess of sales over total variable costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

47

Contribution margin is also known as gross margin.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

48

Under an income statement prepared using absorption costing, expenses are grouped according to cost behavior.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

49

When units produced equal units sold, reported income is identical under absorption costing and variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

50

Under variable costing, fixed manufacturing overhead is expensed at the time the units are produced. Under absorption costing, fixed manufacturing overhead is expensed at the time the units are sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

51

When units produced are less than units sold, income under absorption costing is higher than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

52

Sales less total variable costs equals manufacturing margin.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

53

Variable costing is the only acceptable basis for both external reporting and tax reporting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

54

When the number of units produced exceeds the number of units sold, absorption costing defers some of the fixed costs incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

55

Which of the following is not a product cost under variable costing?

A) Direct materials.

B) Fixed manufacturing overhead.

C) Direct labor.

D) Variable manufacturing overhead.

E) All variable manufacturing costs.

A) Direct materials.

B) Fixed manufacturing overhead.

C) Direct labor.

D) Variable manufacturing overhead.

E) All variable manufacturing costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

56

Income under absorption costing will always be different than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

57

It is not possible to convert reports prepared using variable costing to absorption costing reports.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

58

A variable costing income statement focuses attention on the relationship between costs and sales that is not evident from the absorption costing format.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

59

To convert variable costing income to absorption costing income, management will need to add fixed overhead cost deferred in ending inventory and subtract fixed overhead cost recognized from beginning inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

60

When units produced exceed the units sold, income under absorption costing is higher than income under variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

61

A company is currently operating at 75% capacity and producing 3,000 units. Current cost information relating to this production is shown in the table below: The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

A) Any amount over $43 per unit.

B) Any amount over $17 per unit.

C) Any amount over $21 per unit.

D) Any amount over $13 per unit.

E) Any amount over $22 per unit.

The company has been approached by a customer with a request for a 200-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?A) Any amount over $43 per unit.

B) Any amount over $17 per unit.

C) Any amount over $21 per unit.

D) Any amount over $13 per unit.

E) Any amount over $22 per unit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

62

Under absorption costing, a company had the following unit costs when 9,000 units were produced. Compute the total product cost per unit under variable costing if 30,000 units had been produced.

A) $31.75

B) $28.25

C) $23.45

D) $15.25

E) $20.75

Compute the total product cost per unit under variable costing if 30,000 units had been produced.A) $31.75

B) $28.25

C) $23.45

D) $15.25

E) $20.75

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

63

Which of the following best describes costs assigned to the product under the absorption costing method? Direct labor (DL)

Direct materials (DM)

Variable selling and administrative (VSA)

Variable manufacturing overhead (VOH)

Fixed selling and administrative (FSA)

Fixed manufacturing overhead (FOH)

A) DL, DM, VSA, and VOH.

B) DL, DM, and VOH.

C) DL, DM, VOH, and FOH.

D) DL and DM.

E) DL, DM, FSA, and FOH.

Direct materials (DM)

Variable selling and administrative (VSA)

Variable manufacturing overhead (VOH)

Fixed selling and administrative (FSA)

Fixed manufacturing overhead (FOH)

A) DL, DM, VSA, and VOH.

B) DL, DM, and VOH.

C) DL, DM, VOH, and FOH.

D) DL and DM.

E) DL, DM, FSA, and FOH.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

64

Which of the following would be reported on a variable costing income statement?

A) Gross margin

B) Cost of goods available for sale

C) Total cost of goods sold

D) Contribution margin

E) Work-in-process inventory

A) Gross margin

B) Cost of goods available for sale

C) Total cost of goods sold

D) Contribution margin

E) Work-in-process inventory

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

65

Mentor Corp. has provided the following information for the current year: Calculate the unit product cost using variable costing.

A) $245

B) $275

C) $55

D) $145

E) $125

Calculate the unit product cost using variable costing.A) $245

B) $275

C) $55

D) $145

E) $125

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

66

Mentor Corp. has provided the following information for the current year: Calculate the unit product cost using absorption costing.

A) $245

B) $275

C) $55

D) $145

E) $125

Calculate the unit product cost using absorption costing.A) $245

B) $275

C) $55

D) $145

E) $125

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

67

Under absorption costing, which of the following statements is not true?

A) Over production and inventory buildup can occur because of how managers are evaluated and rewarded.

B) The fixed costs per unit decline as more units are produced.

C) Variable inventory costs are treated in the same manner as they are under variable costing.

D) Fixed inventory costs are treated in the same manner as they are under variable costing.

E) All manufacturing costs are assigned to products.

A) Over production and inventory buildup can occur because of how managers are evaluated and rewarded.

B) The fixed costs per unit decline as more units are produced.

C) Variable inventory costs are treated in the same manner as they are under variable costing.

D) Fixed inventory costs are treated in the same manner as they are under variable costing.

E) All manufacturing costs are assigned to products.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

68

Under absorption costing, a company had the following unit costs when 9,000 units were produced. Compute the total product cost per unit under absorption costing if 25,000 units had been produced.

A) $28.25

B) $23.45

C) $26.25

D) $20.75

E) $15.25

Compute the total product cost per unit under absorption costing if 25,000 units had been produced.A) $28.25

B) $23.45

C) $26.25

D) $20.75

E) $15.25

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

69

Using absorption costing, which of the following manufacturing costs are assigned to products?

A) Direct materials and direct labor.

B) Direct labor and variable manufacturing overhead.

C) Fixed manufacturing overhead, direct materials, and direct labor.

D) Variable manufacturing overhead, direct materials, and direct labor.

E) Variable manufacturing overhead, direct materials, direct labor, and fixed manufacturing overhead.

A) Direct materials and direct labor.

B) Direct labor and variable manufacturing overhead.

C) Fixed manufacturing overhead, direct materials, and direct labor.

D) Variable manufacturing overhead, direct materials, and direct labor.

E) Variable manufacturing overhead, direct materials, direct labor, and fixed manufacturing overhead.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

70

Geneva Company manufactures dolls that are sold to various customers. The company works at full capacity for half the year to meet peak demand, and operates at 80% capacity for the other half of the year. The following information is provided: Geneva receives a purchase order to make 5,000 dolls as a one-time event. The good news is that this order is during a period when Geneva does have sufficient excess capacity. What is the lowest selling price Geneva should accept for this purchase order?

A) $35.00

B) $26.00

C) $29.50

D) $23.50

E) $25.00

Geneva receives a purchase order to make 5,000 dolls as a one-time event. The good news is that this order is during a period when Geneva does have sufficient excess capacity. What is the lowest selling price Geneva should accept for this purchase order?A) $35.00

B) $26.00

C) $29.50

D) $23.50

E) $25.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

71

Which of the following best describes costs assigned to the product under the variable costing method? Direct labor (DL)

Direct materials (DM)

Variable selling and administrative (VSA)

Variable manufacturing overhead (VOH)

Fixed selling and administrative (FSA)

Fixed manufacturing overhead (FOH)

A) DL, DM, VSA, and VOH.

B) DL, DM, and VOH.

C) DL, DM, VOH, and FOH.

D) DL and DM.

E) DL, DM, FSA, and FOH.

Direct materials (DM)

Variable selling and administrative (VSA)

Variable manufacturing overhead (VOH)

Fixed selling and administrative (FSA)

Fixed manufacturing overhead (FOH)

A) DL, DM, VSA, and VOH.

B) DL, DM, and VOH.

C) DL, DM, VOH, and FOH.

D) DL and DM.

E) DL, DM, FSA, and FOH.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

72

Which of the following statements is true?

A) Variable costing treats fixed overhead as a period cost.

B) Absorption costing treats fixed overhead as a period cost.

C) Absorption costing treats fixed overhead as an expense in the period it is incurred.

D) Variable costing excludes all overhead from product costs.

E) Managers can manipulate earnings more easily under variable costing by varying the production level.

A) Variable costing treats fixed overhead as a period cost.

B) Absorption costing treats fixed overhead as a period cost.

C) Absorption costing treats fixed overhead as an expense in the period it is incurred.

D) Variable costing excludes all overhead from product costs.

E) Managers can manipulate earnings more easily under variable costing by varying the production level.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

73

Which of the following statements is true regarding variable costing?

A) It is a traditional costing approach.

B) Only manufacturing costs that change in total with changes in production level are included in product costs.

C) It is not permitted to be used for managerial reporting.

D) It treats overhead in the same manner as absorption costing.

E) It makes it easier to manipulate earnings with changes in production levels.

A) It is a traditional costing approach.

B) Only manufacturing costs that change in total with changes in production level are included in product costs.

C) It is not permitted to be used for managerial reporting.

D) It treats overhead in the same manner as absorption costing.

E) It makes it easier to manipulate earnings with changes in production levels.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

74

Which of the following statements is true?

A) Under variable costing, direct materials and direct labor are expensed as period expenses.

B) Under variable costing, fixed manufacturing overhead is expensed as period expenses.

C) Fixed manufacturing overhead costs are treated the same under both absorption costing and variable costing.

D) Reported income under absorption costing is not affected by production level changes.

E) Under absorption costing, fixed manufacturing overhead is expensed as period expenses.

A) Under variable costing, direct materials and direct labor are expensed as period expenses.

B) Under variable costing, fixed manufacturing overhead is expensed as period expenses.

C) Fixed manufacturing overhead costs are treated the same under both absorption costing and variable costing.

D) Reported income under absorption costing is not affected by production level changes.

E) Under absorption costing, fixed manufacturing overhead is expensed as period expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

75

Which of the following statements is true regarding absorption costing?

A) It is not the traditional costing approach.

B) It is not permitted to be used for financial reporting.

C) It is not permitted to be used for tax reporting.

D) It assigns all manufacturing costs to products.

E) It requires only variable costs to be treated as product costs.

A) It is not the traditional costing approach.

B) It is not permitted to be used for financial reporting.

C) It is not permitted to be used for tax reporting.

D) It assigns all manufacturing costs to products.

E) It requires only variable costs to be treated as product costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

76

A company is currently operating at 80% capacity producing 5,000 units. Current cost information relating to this production is shown in the table below: The company has been approached by a customer with a request for a 100-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?

A) Any amount over $34 per unit.

B) Any amount over $20 per unit.

C) Any amount over $14 per unit.

D) Any amount over $9 per unit.

E) Any amount over $5 per unit.

The company has been approached by a customer with a request for a 100-unit special order. What is the minimum per unit sales price that management would accept for this order if the company wishes to increase current profits?A) Any amount over $34 per unit.

B) Any amount over $20 per unit.

C) Any amount over $14 per unit.

D) Any amount over $9 per unit.

E) Any amount over $5 per unit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

77

Income ________ when there is zero beginning inventory and all inventory units produced are sold.

A) Will be lower under variable costing than absorption costing

B) Will be the same under both variable and absorption costing

C) Will be higher under variable costing than absorption costing

D) Will be higher than gross margin under variable costing

E) Will be lower than administrative costs under absorption costing

A) Will be lower under variable costing than absorption costing

B) Will be the same under both variable and absorption costing

C) Will be higher under variable costing than absorption costing

D) Will be higher than gross margin under variable costing

E) Will be lower than administrative costs under absorption costing

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

78

When evaluating a special order, management should:

A) Only accept the order if the incremental revenue exceeds all product costs.

B) Only accept the order if the incremental revenue exceeds fixed product costs.

C) Only accept the order if the incremental revenue exceeds total variable product costs.

D) Only accept the order if the incremental revenue exceeds full absorption product costs.

E) Only accept the order if the incremental revenue exceeds regular sales revenue.

A) Only accept the order if the incremental revenue exceeds all product costs.

B) Only accept the order if the incremental revenue exceeds fixed product costs.

C) Only accept the order if the incremental revenue exceeds total variable product costs.

D) Only accept the order if the incremental revenue exceeds full absorption product costs.

E) Only accept the order if the incremental revenue exceeds regular sales revenue.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

79

When the number of units sold exceed the number of units produced, income reported under absorption costing will be lower than variable costing. Which of the following gives the best justification of the above statement?

A) Income under absorption costing is always less than income reported using variable costing, regardless of the number of units produced.

B) Income under absorption costing is always more than income reported using variable costing, regardless of the number of units produced.

C) The fixed overhead cost deferred in ending inventory is greater than the fixed overhead cost recognized from beginning inventory.

D) The fixed overhead cost deferred in ending inventory is less than the fixed overhead cost recognized from beginning inventory.

E) Fixed overhead is treated as a period cost under absorption costing.

A) Income under absorption costing is always less than income reported using variable costing, regardless of the number of units produced.

B) Income under absorption costing is always more than income reported using variable costing, regardless of the number of units produced.

C) The fixed overhead cost deferred in ending inventory is greater than the fixed overhead cost recognized from beginning inventory.

D) The fixed overhead cost deferred in ending inventory is less than the fixed overhead cost recognized from beginning inventory.

E) Fixed overhead is treated as a period cost under absorption costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

80

Under absorption costing, a company had the following unit costs when 8,000 units were produced. Compute the total production cost per unit under variable costing if 25,000 units had been produced.

A) $31.75

B) $27.25

C) $26.25

D) $24.25

E) $17.50

Compute the total production cost per unit under variable costing if 25,000 units had been produced.A) $31.75

B) $27.25

C) $26.25

D) $24.25

E) $17.50

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 202 في هذه المجموعة.