Deck 10: Section 404 Audits of Internal Control and Control Risk

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

Which of the following parties provides an assessment of the effectiveness of internal control over financial reporting for public companies?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

When management is evaluating the design of internal control, management evaluates whether the control can do which of the following?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Which of the following factors may increase risks to an organization?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

Which of the following best describes an entity's accounting information and communication system?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

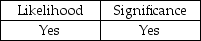

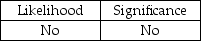

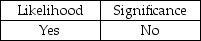

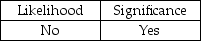

To determine if significant internal control deficiencies are material weaknesses, they must be evaluated on their:

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Section 404 requires auditors to evaluate the effectiveness of the audit committee's oversight of the company's:

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/116

العب

ملء الشاشة (f)

Deck 10: Section 404 Audits of Internal Control and Control Risk

1

Describe each of the three broad objectives management typically has for internal control. With which of these objectives is the auditor primarily concerned?

The three objectives are:

• Reliability of financial reporting. Management has both a legal and professional responsibility to be sure that the information is fairly presented in according with reporting requirements such as GAAP.

• Efficiency and effectiveness of operations. Controls within an organization are meant to encourage efficient and effective use of its resources to optimize the company's goals.

• Compliance with laws and regulations. Public, non-public, and not-for-profit organizations are required to follow many laws and regulations. Some relate to accounting only indirectly, such as environmental protection and civil rights laws. Others are closely related to accounting, such as income tax regulations and anti-fraud legal provisions.

The auditor's focus in both the audit of financial statements and the audit of internal controls is on the controls over the reliability of financial reporting plus those controls over operations and compliance with laws and regulations that could materially affect financial reporting.

• Reliability of financial reporting. Management has both a legal and professional responsibility to be sure that the information is fairly presented in according with reporting requirements such as GAAP.

• Efficiency and effectiveness of operations. Controls within an organization are meant to encourage efficient and effective use of its resources to optimize the company's goals.

• Compliance with laws and regulations. Public, non-public, and not-for-profit organizations are required to follow many laws and regulations. Some relate to accounting only indirectly, such as environmental protection and civil rights laws. Others are closely related to accounting, such as income tax regulations and anti-fraud legal provisions.

The auditor's focus in both the audit of financial statements and the audit of internal controls is on the controls over the reliability of financial reporting plus those controls over operations and compliance with laws and regulations that could materially affect financial reporting.

2

Two key concepts that underlie management's design and implementation of internal control are:

A) costs and materiality.

B) absolute assurance and costs.

C) inherent limitations and reasonable assurance.

D) collusion and materiality.

A) costs and materiality.

B) absolute assurance and costs.

C) inherent limitations and reasonable assurance.

D) collusion and materiality.

C

3

Which of management's assertions with respect to implementing internal controls is the auditor primarily concerned?

A) efficiency of operations

B) reliability of financial reporting

C) effectiveness of operations

D) compliance with applicable laws and regulations

A) efficiency of operations

B) reliability of financial reporting

C) effectiveness of operations

D) compliance with applicable laws and regulations

B

4

Which of the following parties provides an assessment of the effectiveness of internal control over financial reporting for public companies?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

5

Sarbanes-Oxley requires management to issue an internal control report that includes two specific items. Which of the following is one of these two requirements?

A) A statement that management is responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

B) A statement that management and the board of directors are jointly responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

C) A statement that management, the board of directors, and the external auditors are jointly responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

D) A statement that the external auditors are solely responsible.

A) A statement that management is responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

B) A statement that management and the board of directors are jointly responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

C) A statement that management, the board of directors, and the external auditors are jointly responsible for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

D) A statement that the external auditors are solely responsible.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

6

The auditors primary purpose in auditing the client's system of internal control over financial reporting is:

A) to prevent fraudulent financial statements from being issued to the public.

B) to evaluate the effectiveness of the company's internal controls over all relevant assertions in the financial statements.

C) to report to management that the internal controls are effective in preventing misstatements from appearing on the financial statements.

D) to efficiently conduct the Audit of Financial Statements.

A) to prevent fraudulent financial statements from being issued to the public.

B) to evaluate the effectiveness of the company's internal controls over all relevant assertions in the financial statements.

C) to report to management that the internal controls are effective in preventing misstatements from appearing on the financial statements.

D) to efficiently conduct the Audit of Financial Statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

7

A company frequently sells products at a price below inventory cost. Essential controls in the risk assessment process would include:

A) adequate controls that address the risk of overstating inventory.

B) adequate controls that address the risk of not including a purchased item in inventory.

C) adequate controls that address the risk of understatement of inventory.

D) adequate controls that address the risk of overstatement of cost of goods sold.

A) adequate controls that address the risk of overstating inventory.

B) adequate controls that address the risk of not including a purchased item in inventory.

C) adequate controls that address the risk of understatement of inventory.

D) adequate controls that address the risk of overstatement of cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

8

When one material weakness is present at the end of the year, management of a public company must conclude that internal control over financial reporting is:

A) insufficient.

B) inadequate.

C) ineffective.

D) inefficient.

A) insufficient.

B) inadequate.

C) ineffective.

D) inefficient.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

9

When management is evaluating the design of internal control, management evaluates whether the control can do which of the following?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

10

Which of the following is most correct regarding the requirements under Section 404 of the Sarbanes Oxley Act?

A) The audits of internal control and the financial statements provide reasonable assurance as to misstatements.

B) The audit of internal control provides absolute assurance of misstatement.

C) The audit of financial statements provides absolute assurance of misstatement.

D) The audits of internal control and the financial statements provide absolute assurance as to misstatements.

A) The audits of internal control and the financial statements provide reasonable assurance as to misstatements.

B) The audit of internal control provides absolute assurance of misstatement.

C) The audit of financial statements provides absolute assurance of misstatement.

D) The audits of internal control and the financial statements provide absolute assurance as to misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

11

Internal controls are not designed to provide reasonable assurance that:

A) all frauds will be detected.

B) transactions are executed in accordance with management's authorization.

C) access to assets is permitted only in accordance with management's authorization.

D) company personnel comply with applicable rules and regulations.

A) all frauds will be detected.

B) transactions are executed in accordance with management's authorization.

C) access to assets is permitted only in accordance with management's authorization.

D) company personnel comply with applicable rules and regulations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

12

The primary emphasis by auditors when evaluating and testing internal control is on controls over classes of transactions rather than controls over account balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

13

An act of two or more employees to steal assets and cover their theft by misstating the accounting records would be referred to as:

A) collusion.

B) a material weakness.

C) a control deficiency.

D) a significant deficiency.

A) collusion.

B) a material weakness.

C) a control deficiency.

D) a significant deficiency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

14

Management must disclose material weaknesses in internal control in its audit report:

A) whenever the weakness is deemed significant to a single class of transactions.

B) whenever the weakness is significant to overall financial reporting objectives.

C) if the weakness exists at the end of the year.

D) only if the auditor identifies the weakness as significant.

A) whenever the weakness is deemed significant to a single class of transactions.

B) whenever the weakness is significant to overall financial reporting objectives.

C) if the weakness exists at the end of the year.

D) only if the auditor identifies the weakness as significant.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

15

To issue a report on internal control over financial reporting for a public company, an auditor must:

A) evaluate management's assessment process.

B) independently assess the design and operating effectiveness of internal control.

C) evaluate management's assessment process and independently assess the design and operating effectiveness of internal control.

D) test controls over significant account balances.

A) evaluate management's assessment process.

B) independently assess the design and operating effectiveness of internal control.

C) evaluate management's assessment process and independently assess the design and operating effectiveness of internal control.

D) test controls over significant account balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

16

The PCAOB places responsibility for the reliability of internal controls over the financial reporting process to:

A) the company's board of directors.

B) the audit committee of the board of directors.

C) the CEO and the CFO.

D) the CFO and the Independent Auditors.

A) the company's board of directors.

B) the audit committee of the board of directors.

C) the CEO and the CFO.

D) the CFO and the Independent Auditors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which of the following is responsible for establishing a private company's internal control?

A) Senior Management

B) Internal Auditors

C) Senior Management and auditors

D) Audit committee

A) Senior Management

B) Internal Auditors

C) Senior Management and auditors

D) Audit committee

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

18

The Public Company Accounting Oversight Board states that reasonable assurance allows a:

A) small likelihood of ineffective internal controls.

B) remote likelihood that material misstatements will not be prevented or detected by internal control.

C) likelihood that material misstatements will not be prevented or detected by internal control.

D) high likelihood that material misstatements will not be prevented or detected by internal control.

A) small likelihood of ineffective internal controls.

B) remote likelihood that material misstatements will not be prevented or detected by internal control.

C) likelihood that material misstatements will not be prevented or detected by internal control.

D) high likelihood that material misstatements will not be prevented or detected by internal control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

19

The Sarbanes-Oxley Act of 2002 requires that public companies issue an internal control report.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following is not one of the three primary objectives of effective internal control?

A) reliability of financial reporting

B) efficiency and effectiveness of operations

C) compliance with laws and regulations

D) assurance of elimination of business risk

A) reliability of financial reporting

B) efficiency and effectiveness of operations

C) compliance with laws and regulations

D) assurance of elimination of business risk

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

21

Even with the most effectively designed internal control, the auditor must obtain audit evidence, beyond testing the controls, for every:

A) transaction.

B) financial statement account.

C) material financial statement account.

D) financial statement account that will be relied upon by third parties.

A) transaction.

B) financial statement account.

C) material financial statement account.

D) financial statement account that will be relied upon by third parties.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

22

Internal controls can never be regarded as completely effective. Even if company personnel could design an ideal system, its effectiveness depends on the:

A) adequacy of the computer system.

B) proper implementation by management.

C) ability of the internal audit staff to maintain it.

D) competency and dependability of the people using it.

A) adequacy of the computer system.

B) proper implementation by management.

C) ability of the internal audit staff to maintain it.

D) competency and dependability of the people using it.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

23

Which of the following factors may increase risks to an organization?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following best describes an entity's accounting information and communication system?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

25

Which of the following is correct with respect to the design and use of business documents?

A) Not all documents used for internal purposes need to be prenumbered.

B) Documents should be designed for single purposes only to avoid confusion in their use.

C) Documents should be designed to be understandable only by those who use them.

D) Documents designed for external use must be prenumbered.

A) Not all documents used for internal purposes need to be prenumbered.

B) Documents should be designed for single purposes only to avoid confusion in their use.

C) Documents should be designed to be understandable only by those who use them.

D) Documents designed for external use must be prenumbered.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

26

The primary emphasis by auditors is on controls over:

A) classes of transactions.

B) account balances.

C) both A and B, because they are equally important.

D) both A and B, because they vary from client to client.

A) classes of transactions.

B) account balances.

C) both A and B, because they are equally important.

D) both A and B, because they vary from client to client.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

27

An auditor should consider two key issues when obtaining an understanding of a client's internal controls. These issues are:

A) the effectiveness and efficiency of the controls.

B) the frequency and effectiveness of the controls.

C) the design and implementation of the controls.

D) the implementation and efficiency of the controls.

A) the effectiveness and efficiency of the controls.

B) the frequency and effectiveness of the controls.

C) the design and implementation of the controls.

D) the implementation and efficiency of the controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

28

Internal controls normally include procedures designed to provide reasonable assurance that:

A) employees act with integrity when performing their assigned tasks.

B) transactions are executed in accordance with management's authorization.

C) decision processes leading to management's authorization of transactions are sound.

D) collusive activities would be detected by segregation of employee duties.

A) employees act with integrity when performing their assigned tasks.

B) transactions are executed in accordance with management's authorization.

C) decision processes leading to management's authorization of transactions are sound.

D) collusive activities would be detected by segregation of employee duties.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

29

The Sarbanes-Oxley Act requires:

A) all public companies to issue reports on internal controls.

B) all public companies to define adequate internal controls.

C) the auditor of public companies to design effective ICFR.

D) the auditor of public companies to provide recommendations to correct material weaknesses.

A) all public companies to issue reports on internal controls.

B) all public companies to define adequate internal controls.

C) the auditor of public companies to design effective ICFR.

D) the auditor of public companies to provide recommendations to correct material weaknesses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

30

Which of the following deal with ongoing or periodic assessment of the quality of internal control by management?

A) Quality monitoring activities

B) Monitoring activities

C) Oversight activities

D) Management activities

A) Quality monitoring activities

B) Monitoring activities

C) Oversight activities

D) Management activities

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

31

Which of the following activities would be least likely to strengthen a company's internal control?

A) separating accounting from other financial operations

B) maintaining insurance for fire and theft

C) fixing responsibility for the performance of employee duties

D) carefully selecting and training employees

A) separating accounting from other financial operations

B) maintaining insurance for fire and theft

C) fixing responsibility for the performance of employee duties

D) carefully selecting and training employees

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

32

In performing the audit of internal control over financial reporting the auditor emphasizes internal control over class of transactions because:

A) the accuracy of accounting system outputs depends heavily on the accuracy of inputs and processing.

B) the class of transaction is where most fraud schemes occur.

C) account balances are less important to the auditor then the changes in the account balances.

D) classes of transactions tests are the most efficient manner to compensate for inherent risk.

A) the accuracy of accounting system outputs depends heavily on the accuracy of inputs and processing.

B) the class of transaction is where most fraud schemes occur.

C) account balances are less important to the auditor then the changes in the account balances.

D) classes of transactions tests are the most efficient manner to compensate for inherent risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following components of the control environment define the existing lines of responsibility and authority?

A) Organizational Structure

B) Management philosophy and operating style

C) Human resource policies and practices

D) Management integrity and ethical values

A) Organizational Structure

B) Management philosophy and operating style

C) Human resource policies and practices

D) Management integrity and ethical values

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

34

An audit procedure that would most likely be used by an auditor in performing tests of control procedures in which the segregation of functions and that leaves no "audit" trail is:

A) inspection.

B) observation.

C) reperformance.

D) reconciliation.

A) inspection.

B) observation.

C) reperformance.

D) reconciliation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

35

Which of the following best describes the purpose of control activities?

A) the actions, policies and procedures that reflect the overall attitudes of management

B) the identification and analysis of risks relevant to the preparation of financial statements

C) the policies and procedures that help ensure that necessary actions are taken to address risks to the achievement of the entity's objectives

D) activities that deal with the ongoing assessment of the quality of internal control by management

A) the actions, policies and procedures that reflect the overall attitudes of management

B) the identification and analysis of risks relevant to the preparation of financial statements

C) the policies and procedures that help ensure that necessary actions are taken to address risks to the achievement of the entity's objectives

D) activities that deal with the ongoing assessment of the quality of internal control by management

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

36

When a company designs and implements internal controls, cost of the controls is not a valid consideration.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

37

Authorizations can be either general or specific. Which of the following is not an example of a general authorization?

A) Automatic reorder points for raw materials inventory.

B) A sales manager's authorization for a sales return.

C) Credit limits for various classes of customers.

D) A sales price list for merchandise.

A) Automatic reorder points for raw materials inventory.

B) A sales manager's authorization for a sales return.

C) Credit limits for various classes of customers.

D) A sales price list for merchandise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

38

Of the following statements about internal controls, which one is least likely to be correct?

A) No one person should be responsible for the custodial responsibility and the recording responsibility for an asset.

B) Transactions must be properly authorized before such transactions are processed.

C) Because of the cost-benefit relationship, a client may apply controls on a test basis.

D) Control procedures reasonably ensure that collusion among employees cannot occur.

A) No one person should be responsible for the custodial responsibility and the recording responsibility for an asset.

B) Transactions must be properly authorized before such transactions are processed.

C) Because of the cost-benefit relationship, a client may apply controls on a test basis.

D) Control procedures reasonably ensure that collusion among employees cannot occur.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

39

The financial statements may not correctly reflect accounting frameworks such as AAP or IFRS if the:

A) controls affecting the reliability of financial reporting are inadequate.

B) company's controls do not promote efficiency.

C) company's controls do not promote effectiveness.

D) company's controls do not promote compliance with applicable rules and regulations.

A) controls affecting the reliability of financial reporting are inadequate.

B) company's controls do not promote efficiency.

C) company's controls do not promote effectiveness.

D) company's controls do not promote compliance with applicable rules and regulations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

40

Which of the following statements is most correct with respect to separation of duties?

A) Employees should not have temporary and permanent custody of assets.

B) Employees who authorize transactions should not have custody of related assets.

C) It is permissible to allow an employee to open cash receipts and record those receipts.

D) Employees who authorize transactions should have recording responsibility for these transactions.

A) Employees should not have temporary and permanent custody of assets.

B) Employees who authorize transactions should not have custody of related assets.

C) It is permissible to allow an employee to open cash receipts and record those receipts.

D) Employees who authorize transactions should have recording responsibility for these transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

41

Adequate separation of duties is an important control activity. Discuss the four general guidelines for separation of duties to prevent both intentional and unintentional misstatements that are of significance to auditors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

42

Proper segregation of functional responsibilities calls for separation of:

A) authorization, execution, and payment.

B) authorization, recording, and custody.

C) custody, execution, and reporting.

D) authorization, payment, and recording.

A) authorization, execution, and payment.

B) authorization, recording, and custody.

C) custody, execution, and reporting.

D) authorization, payment, and recording.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

43

To promote operational efficiency, the internal audit department would ideally report to:

A) line management.

B) senior management.

C) Chief Accounting Officer.

D) audit committee.

A) line management.

B) senior management.

C) Chief Accounting Officer.

D) audit committee.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

44

Management's identification and analysis of risk is an ongoing process and is a critical component of effective internal control. An important first step is for management to identify factors that may increase risk. Identify at least five factors, observable by management, which may lead to increased risk in a typical business organization.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

45

It is important for the CPA to consider the competence of the clients' personnel because their competence bears directly and importantly upon the:

A) cost/benefit relationship of the system of internal control.

B) achievement of the objectives of internal control.

C) comparison of recorded accountability with assets.

D) timing of the tests to be performed.

A) cost/benefit relationship of the system of internal control.

B) achievement of the objectives of internal control.

C) comparison of recorded accountability with assets.

D) timing of the tests to be performed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

46

Certain principles dictate the proper design and use of documents and records. Briefly describe several of these principles.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which of the following is not one of the subcomponents of the control environment?

A) management's philosophy and operating style

B) organizational structure

C) adequate separation of duties

D) commitment to competence

A) management's philosophy and operating style

B) organizational structure

C) adequate separation of duties

D) commitment to competence

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

48

As a client's information system becomes more complex, it is likely that an auditor will increase reliance on controls and decrease substantive tests to support a control risk assessment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

49

Which of the following groups establishes and maintains the company's internal controls?

A) Internal auditors

B) Board of Directors

C) Management

D) Audit committee

A) Internal auditors

B) Board of Directors

C) Management

D) Audit committee

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

50

Control activities help assure that the necessary actions are taken to address risks to the achievement of the company's objectives. List the five types of control activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

51

In developing an understanding of the client's accounting information system the auditor follows a sequential process. Describe the process below:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

52

Adequate documents and records is a subcomponent of the control environment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

53

Which of the following is correct regarding management's documentation of internal controls?

A) inadequate documentation is not a control deficiency

B) documentation needs to focus on interim controls

C) documentation needs to have some focus on controls designed to detect fraud

D) documentation should only focus on system design

A) inadequate documentation is not a control deficiency

B) documentation needs to focus on interim controls

C) documentation needs to have some focus on controls designed to detect fraud

D) documentation should only focus on system design

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

54

Discuss what is meant by the term "control environment" and identify four control environment subcomponents that the auditor should consider.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

55

The independent auditor should acquire an understanding of the internal audit function as it relates to the independent auditor's study and evaluation of internal control because the:

A) audit programs, working papers, and reports of internal auditors can often be used as a substitute for the work of the independent auditor's staff.

B) procedures performed by the internal audit staff may eliminate the independent auditor's need for an extensive study and evaluation of internal control.

C) work performed by internal auditors may be a factor in determining the nature, timing, and extent of the independent auditor's procedures.

D) understanding of the internal audit function is an important substantive test to be performed by the independent auditor.

A) audit programs, working papers, and reports of internal auditors can often be used as a substitute for the work of the independent auditor's staff.

B) procedures performed by the internal audit staff may eliminate the independent auditor's need for an extensive study and evaluation of internal control.

C) work performed by internal auditors may be a factor in determining the nature, timing, and extent of the independent auditor's procedures.

D) understanding of the internal audit function is an important substantive test to be performed by the independent auditor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

56

Hanlon Corp. maintains a large internal audit staff that reports directly to the chief financial officer. Audit reports prepared by the internal auditors indicate that the system is functioning as it should and that the accounting records are reliable. An independent auditor will probably:

A) eliminate tests of controls.

B) increase the depth of the study and evaluation of administrative controls.

C) avoid duplicating the work performed by the internal audit staff.

D) place limited reliance on the work performed by the internal audit staff.

A) eliminate tests of controls.

B) increase the depth of the study and evaluation of administrative controls.

C) avoid duplicating the work performed by the internal audit staff.

D) place limited reliance on the work performed by the internal audit staff.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

57

The internal control framework developed by COSO includes five so-called "components" of internal control. Discuss each of these five components.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

58

Separation of duties is essential in preventing errors and intentional misstatements on the financial statements. List below the four general guidelines.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

59

To obtain an understanding of an entity's control environment, an auditor should concentrate on the substance of management's policies and procedures rather than their form because:

A) management may establish appropriate policies and procedures but not act on them.

B) the board of directors may not be aware of management's attitude toward the control environment.

C) the auditor may believe that the policies and procedures are inappropriate for that particular entity.

D) the policies and procedures may be so weak that no reliance is contemplated by the auditor.

A) management may establish appropriate policies and procedures but not act on them.

B) the board of directors may not be aware of management's attitude toward the control environment.

C) the auditor may believe that the policies and procedures are inappropriate for that particular entity.

D) the policies and procedures may be so weak that no reliance is contemplated by the auditor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

60

External financial statement auditors must obtain evidence regarding what attributes of an internal audit (IA) department if the external auditors intend to rely on IA's work?

A) Integrity

B) Objectivity

C) Competence

D) All of the above

A) Integrity

B) Objectivity

C) Competence

D) All of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

61

Procedures used to obtain an understanding of internal control are normally performed on fewer transactions than procedures used to test controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

62

Section 404 requires auditors to perform walkthroughs to assist in understanding internal control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

63

When documenting their understanding of a client's internal controls, auditors are required to use narratives.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

64

Auditing standards prohibit reliance on the work of internal auditors due to the lack of independence of the internal auditors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

65

Which of the following is the correct definition of "control deficiency"?

A) A control deficiency exists if the design or operation of controls does not permit company personnel to prevent or detect misstatements on a timely basis.

B) A control deficiency exists if one or more deficiencies exist that adversely affect a company's ability to prepare external financial statements reliably.

C) A control deficiency exists if the design or operation of controls results in a more than remote likelihood that controls will not prevent or detect misstatements.

D) A control deficiency exists if the design or operation of controls results in a more than probable likelihood that controls will prevent or detect misstatements.

A) A control deficiency exists if the design or operation of controls does not permit company personnel to prevent or detect misstatements on a timely basis.

B) A control deficiency exists if one or more deficiencies exist that adversely affect a company's ability to prepare external financial statements reliably.

C) A control deficiency exists if the design or operation of controls results in a more than remote likelihood that controls will not prevent or detect misstatements.

D) A control deficiency exists if the design or operation of controls results in a more than probable likelihood that controls will prevent or detect misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

66

You are performing the audit of internal control for Clifton Company. Which of the following would represent a material weakness in internal control?

A) The company's audit committee has experienced unusual turnover of members.

B) The company's CFO was indicted for embezzling from the company.

C) Bank reconciliations are done monthly.

D) The CEO was forced to resign due to an inappropriate relationship with an outside vendor.

A) The company's audit committee has experienced unusual turnover of members.

B) The company's CFO was indicted for embezzling from the company.

C) Bank reconciliations are done monthly.

D) The CEO was forced to resign due to an inappropriate relationship with an outside vendor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

67

Narratives, flowcharts, and internal control questionnaires are three common methods of:

A) testing the internal controls.

B) documenting the auditor's understanding of internal controls.

C) designing the audit manual and procedures.

D) documenting the auditor's understanding of a client's organizational structure.

A) testing the internal controls.

B) documenting the auditor's understanding of internal controls.

C) designing the audit manual and procedures.

D) documenting the auditor's understanding of a client's organizational structure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

68

To determine if significant internal control deficiencies are material weaknesses, they must be evaluated on their:

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

69

The person responsible for reconciling sales invoices to customer orders does not access to the company's master price list in order to correctly compute sales. This is an example of a(n):

A) operating deficiency.

B) design deficiency.

C) training deficiency.

D) management deficiency.

A) operating deficiency.

B) design deficiency.

C) training deficiency.

D) management deficiency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

70

If an auditor wishes to rely on the work of internal auditors (IA), the auditor must obtain satisfactory evidence related to the IA's competence, integrity, and objectivity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

71

Audit evidence concerning proper segregation of duties normally is best obtained by:

A) direct personal observation of the employee who applies control procedures.

B) making inquiries of co-workers about the employee who applies control procedures.

C) preparation of a flowchart of duties performed and available personnel.

D) inspection of third-party documents containing the initials of who applied control procedures.

A) direct personal observation of the employee who applies control procedures.

B) making inquiries of co-workers about the employee who applies control procedures.

C) preparation of a flowchart of duties performed and available personnel.

D) inspection of third-party documents containing the initials of who applied control procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

72

Once auditors determine that entity level controls are designed and placed in the operation they:

A) make a preliminary assessment for each transaction-related audit objective for each major type of transaction.

B) make a preliminary assessment of control risk.

C) obtain an understanding of the design and implementation of internal control.

D) prepare audit documentation in order to opine on the company's internal control system.

A) make a preliminary assessment for each transaction-related audit objective for each major type of transaction.

B) make a preliminary assessment of control risk.

C) obtain an understanding of the design and implementation of internal control.

D) prepare audit documentation in order to opine on the company's internal control system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

73

The chart of accounts is a control and is closely related to the controls related to adequate documents and records.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

74

For most uses, flowcharts are superior to narratives as a method of communicating the characteristics of internal control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

75

Audit evidence regarding the separation of duties is normally best obtained by:

A) preparing flowcharts of operational processes.

B) preparing narratives of operational processes.

C) observation of employees applying control activities.

D) inquiries of employees applying control activities.

A) preparing flowcharts of operational processes.

B) preparing narratives of operational processes.

C) observation of employees applying control activities.

D) inquiries of employees applying control activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

76

The purpose of phase 3 in the "process for understanding internal control and assessing control risk" is to:

A) design, perform and evaluate tests of controls.

B) obtain and document an understanding of internal control design an operation.

C) assess control risk.

D) decide planned detection risk and substantive tests.

A) design, perform and evaluate tests of controls.

B) obtain and document an understanding of internal control design an operation.

C) assess control risk.

D) decide planned detection risk and substantive tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which of the following deficiency exists if a necessary control is missing or not properly formulated?

A) control

B) significant

C) design

D) operating

A) control

B) significant

C) design

D) operating

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

78

Section 404 requires auditors to evaluate the effectiveness of the audit committee's oversight of the company's:

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

79

The employee in charge of authorizing credit to the company's customers does not fully understand the concept of credit risk. This lack of knowledge would constitute:

A) a deficiency in operation of internal controls.

B) a deficiency in design of internal controls.

C) a deficiency of management.

D) not constitute a deficiency.

A) a deficiency in operation of internal controls.

B) a deficiency in design of internal controls.

C) a deficiency of management.

D) not constitute a deficiency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

80

When the auditor attempts to understand the operation of the accounting system by tracing a few transactions through the accounting system, the auditor is said to be:

A) tracing.

B) vouching.

C) performing a walk-through.

D) testing controls.

A) tracing.

B) vouching.

C) performing a walk-through.

D) testing controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 116 في هذه المجموعة.