Deck 9: Reporting Principles and Preparation of Fund Financial Statements

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

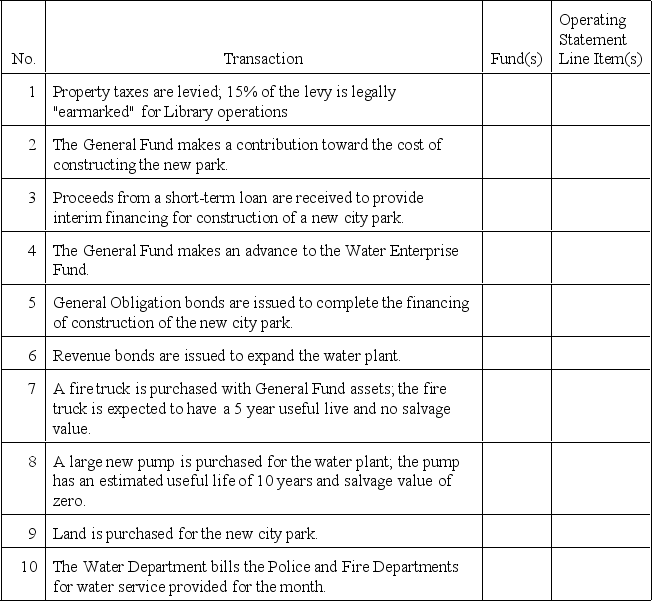

(Matching transactions with funds and operating statement line items)

Harmony Township maintains four funds:

A the General Fund,

B the Library Special Revenue Fund,

C the Capital Projects Fund (recently established to account for the construction of a new city park),and

D the Water Enterprise Fund.

For each of the transactions described below,indicate by letter the fund(s)involved and by number the operating statement line item(s)that could be affected.

Harmony Township maintains four funds:

A the General Fund,

B the Library Special Revenue Fund,

C the Capital Projects Fund (recently established to account for the construction of a new city park),and

D the Water Enterprise Fund.

For each of the transactions described below,indicate by letter the fund(s)involved and by number the operating statement line item(s)that could be affected.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Match between columns

الفرضيات:

The relationships between two primary governments and a third organization may be such that the third organization can be a component unit of both primary governments.

The relationships between two primary governments and a third organization may be such that the third organization can be a component unit of both primary governments.

An example of a state's ability to impose its will on the operations of a legally separate toll road is its ability to approve the road's proposed increases in toll rates.

An example of a state's ability to impose its will on the operations of a legally separate toll road is its ability to approve the road's proposed increases in toll rates.

الردود:

True

False

True

False

True

False

True

False

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Match between columns

سؤال

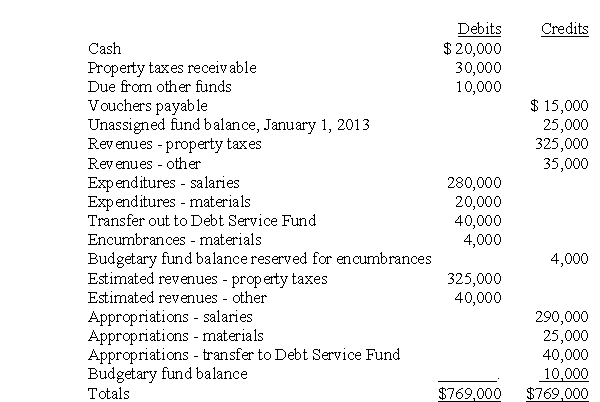

(Preparation of closing entries and fund level financial statements)

Following is a trial balance of City of Peachville's General Fund at December 31,2013.Prepare: (a)closing entries; (b)a post-closing trial balance; (c)a statement of revenues,expenditures,and changes in fund balance for the year ended December 31,2013;and (d)a balance sheet at December 31,2013.

Following is a trial balance of City of Peachville's General Fund at December 31,2013.Prepare: (a)closing entries; (b)a post-closing trial balance; (c)a statement of revenues,expenditures,and changes in fund balance for the year ended December 31,2013;and (d)a balance sheet at December 31,2013.

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/43

العب

ملء الشاشة (f)

Deck 9: Reporting Principles and Preparation of Fund Financial Statements

1

Which of the following sections is not found in proprietary fund operating statements?

A)operating revenues

B)nonoperating revenues

C)operating revenues

D)investing activities

A)operating revenues

B)nonoperating revenues

C)operating revenues

D)investing activities

D

2

The financial statements prepared for fiduciary funds are

A)statement of fiduciary net position

B)statement of changes in fiduciary net position

C)statement of fiduciary cash flows

D)only a and b

E)only b and c

A)statement of fiduciary net position

B)statement of changes in fiduciary net position

C)statement of fiduciary cash flows

D)only a and b

E)only b and c

D

3

Which basis of accounting is used when presenting governmental and proprietary funds in fund-level financial statements?

A)governmental - modified accrual;proprietary - modified accrual

B)governmental - accrual;proprietary - accrual

C)governmental - modified accrual;proprietary - accrual

D)governmental - accrual;proprietary - modified accrual

A)governmental - modified accrual;proprietary - modified accrual

B)governmental - accrual;proprietary - accrual

C)governmental - modified accrual;proprietary - accrual

D)governmental - accrual;proprietary - modified accrual

C

4

Which of the following is one of the minimum requirements established by the GASB for general purpose external financial reporting?

A)introductory letter to report recipients

B)management's discussion and analysis

C)statistical section,with tables of revenues by source and expenditures by function

D)combining statement of non-major funds

A)introductory letter to report recipients

B)management's discussion and analysis

C)statistical section,with tables of revenues by source and expenditures by function

D)combining statement of non-major funds

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

5

A government's discussion of how it defined the reporting entity is presented in which of the following places within the Comprehensive Annual Financial Report?

A)the auditor's report

B)management's discussion and analysis (MD&A)

C)the notes to the financial statements

D)required supplementary information (RSI)

A)the auditor's report

B)management's discussion and analysis (MD&A)

C)the notes to the financial statements

D)required supplementary information (RSI)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

6

An entity can be a component unit of how many primary governments in the same fiscal year?

A)1

B)2

C)3

D)4 or more

A)1

B)2

C)3

D)4 or more

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

7

In addition to the notes,what are the components of the "basic" governmental financial statements?

A)balance sheets and cash flow statements

B)modified accrual financial statements and full accrual financial statements

C)fund financial statements and government-wide financial statements

D)major fund financial statements and minor fund financial statements

A)balance sheets and cash flow statements

B)modified accrual financial statements and full accrual financial statements

C)fund financial statements and government-wide financial statements

D)major fund financial statements and minor fund financial statements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

8

Which fund categories should be included in the fund-level financial statements?

A)governmental,proprietary,and fiduciary

B)only governmental and proprietary

C)only governmental,proprietary,and blended component units

D)only governmental,proprietary,and discretely-presented component units

A)governmental,proprietary,and fiduciary

B)only governmental and proprietary

C)only governmental,proprietary,and blended component units

D)only governmental,proprietary,and discretely-presented component units

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

9

Which of the following is one of the two basic criteria that makes a primary government financially accountable for a legally separate entity?

A)The primary government's chief executive appoints three of the entity's trustees.

B)The primary government appoints a voting majority of the entity's governing body.

C)A department of the primary government can make grants to the entity.

D)A department of the primary government is authorized to obtain and review the entity's financial statements.

A)The primary government's chief executive appoints three of the entity's trustees.

B)The primary government appoints a voting majority of the entity's governing body.

C)A department of the primary government can make grants to the entity.

D)A department of the primary government is authorized to obtain and review the entity's financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

10

Which of the following account captions are you least likely to see on a governmental funds balance sheet?

A)Due from other governments

B)Property,plant and equipment

C)Advance deposits

D)Due to other funds

A)Due from other governments

B)Property,plant and equipment

C)Advance deposits

D)Due to other funds

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

11

The General Fund and other funds for which individual fund financial information is presented in separate columns in the basic governmental fund financial statements are known as

A)principal funds

B)primary funds

C)major funds

D)master funds

A)principal funds

B)primary funds

C)major funds

D)master funds

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

12

An organization is a component unit of a primary government and hence part of the primary government's financial reporting entity,provided that:

A)the primary government provides grants to the organization

B)the primary government sells tax-exempt debt on behalf of the organization

C)the primary government is financially accountable for the organization

D)the primary government makes appropriations to the organization

A)the primary government provides grants to the organization

B)the primary government sells tax-exempt debt on behalf of the organization

C)the primary government is financially accountable for the organization

D)the primary government makes appropriations to the organization

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

13

The Basic Financial Statements,as defined for governments,do not include which of the following components?

A)government-wide financial statements

B)governmental fund financial statements

C)fiduciary fund financial statements

D)combining financial statements

A)government-wide financial statements

B)governmental fund financial statements

C)fiduciary fund financial statements

D)combining financial statements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

14

A state has different relationships with many legally separate organizations.Some elements of the relationships are: (1)the state can appoint a majority of some governing boards; (2)the state is able to impose its will on some;and (3)the state gets financial benefits from or is financially burdened by some.Which relationship or combination of relationships will cause an organization to be part of the state's financial reporting entity?

A)Any one of the three relationships must exist.

B)All three relationships must exist.

C)A combination of relationship (3)and either relationship (1)or (2)must exist.

D)A combination of relationship (1)and either relationship (2)or (3)must exist.

A)Any one of the three relationships must exist.

B)All three relationships must exist.

C)A combination of relationship (3)and either relationship (1)or (2)must exist.

D)A combination of relationship (1)and either relationship (2)or (3)must exist.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

15

Which of the following is a true statement about a government financial reporting entity?

A)if it includes discrete component unit(s)it cannot also include blended component unit(s)

B)if it includes blended component unit(s)it cannot also include discrete component unit(s)

C)it cannot include more discrete component units than blended component units

D)it can include both blended and discrete component units

A)if it includes discrete component unit(s)it cannot also include blended component unit(s)

B)if it includes blended component unit(s)it cannot also include discrete component unit(s)

C)it cannot include more discrete component units than blended component units

D)it can include both blended and discrete component units

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

16

What is the general rule regarding the reporting of special items in fund-level financial statements?

A)They should be displayed separately in the operating statements prepared for governmental and proprietary funds.

B)They should be reported as part of expenditures or expenses in operating statements.

C)They should be displayed as separate items in proprietary fund operating statements,but not in governmental fund operating statements.

D)They should be included as part of revenues in fund operating statements.

A)They should be displayed separately in the operating statements prepared for governmental and proprietary funds.

B)They should be reported as part of expenditures or expenses in operating statements.

C)They should be displayed as separate items in proprietary fund operating statements,but not in governmental fund operating statements.

D)They should be included as part of revenues in fund operating statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which of the following statements is true regarding the inclusion of individual non-major funds in the fund-level financial statements?

A)Individual non-major internal service funds are reported in the fund-level financial statements if a government makes a special election to report them

B)Individual non-major funds must always be reported in the fund-level financial statements.

C)Individual non-major funds must be reported in the fund-level financial statements if,in total,they are more than 50 percent of the total assets or liabilities of the fund category.

D)Individual non-major funds may be reported as "major funds" in the fund-level financial statement if governmental officials believe it is important to financial statement users.

A)Individual non-major internal service funds are reported in the fund-level financial statements if a government makes a special election to report them

B)Individual non-major funds must always be reported in the fund-level financial statements.

C)Individual non-major funds must be reported in the fund-level financial statements if,in total,they are more than 50 percent of the total assets or liabilities of the fund category.

D)Individual non-major funds may be reported as "major funds" in the fund-level financial statement if governmental officials believe it is important to financial statement users.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

18

Which of the following account captions are you most likely to see on a governmental funds balance sheet?

A)bonds payable

B)accumulated depreciation

C)inventory

D)land

A)bonds payable

B)accumulated depreciation

C)inventory

D)land

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following interfund transactions does not affect fund balance?

A)reimbursements

B)transfers

C)loans

D)interfund services provided and used

A)reimbursements

B)transfers

C)loans

D)interfund services provided and used

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which financial statements are required to be prepared for governmental funds in the fund-level financial statements?

A)balance sheet and statement of cash flows

B)balance sheet and statement of revenues,expenditures,and changes in fund balances

C)statement of fiduciary net assets and statement of revenues,expenditures,and changes in fund balances

D)balance sheet and statement of revenues,expenses,and changes in fund net assets

A)balance sheet and statement of cash flows

B)balance sheet and statement of revenues,expenditures,and changes in fund balances

C)statement of fiduciary net assets and statement of revenues,expenditures,and changes in fund balances

D)balance sheet and statement of revenues,expenses,and changes in fund net assets

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

21

Which basis of accounting must be used in presenting the "actual" column of the fund-level budgetary comparison schedules for the General Fund and major Special Revenue Funds?

A)the government's budgetary basis of accounting

B)the modified accrual basis of accounting

C)the full accrual basis of accounting

D)the cash basis of accounting

A)the government's budgetary basis of accounting

B)the modified accrual basis of accounting

C)the full accrual basis of accounting

D)the cash basis of accounting

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

22

(Matching transactions with funds and operating statement line items)

Harmony Township maintains four funds:

A the General Fund,

B the Library Special Revenue Fund,

C the Capital Projects Fund (recently established to account for the construction of a new city park),and

D the Water Enterprise Fund.

For each of the transactions described below,indicate by letter the fund(s)involved and by number the operating statement line item(s)that could be affected.

Harmony Township maintains four funds:

A the General Fund,

B the Library Special Revenue Fund,

C the Capital Projects Fund (recently established to account for the construction of a new city park),and

D the Water Enterprise Fund.

For each of the transactions described below,indicate by letter the fund(s)involved and by number the operating statement line item(s)that could be affected.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

23

To what extent should economic factors be discussed in Management's Discussion and Analysis (MD&A)?

A)major economic factors affecting operating results should be discussed in MD&A

B)economic factors affecting operating results should not be discussed in MD&A

C)economic factors affecting operating results should be discussed in MD&A,provided the auditor extends his/her opinion to the MD&A

D)economic factors should be discussed in MD&A,provided they are also discussed in the notes

A)major economic factors affecting operating results should be discussed in MD&A

B)economic factors affecting operating results should not be discussed in MD&A

C)economic factors affecting operating results should be discussed in MD&A,provided the auditor extends his/her opinion to the MD&A

D)economic factors should be discussed in MD&A,provided they are also discussed in the notes

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which information must be presented in budgetary comparison schedules?

A)only the original appropriated budget

B)only the final appropriated budget

C)both the original appropriated budget and the final appropriated budget

D)both the original budget submitted by the chief executive officer and the first budget approved by the legislative body

A)only the original appropriated budget

B)only the final appropriated budget

C)both the original appropriated budget and the final appropriated budget

D)both the original budget submitted by the chief executive officer and the first budget approved by the legislative body

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

25

In the net position component called "invested in capital assets,net of related debt" (that appears in proprietary fund financial statements),what is the meaning of net of related debt?

A)bonds,notes,or other borrowings originally issued to acquire or improve the capital assets shown in the amount invested in capital assets

B)outstanding balances of bonds,notes,or other borrowings,issued for any purpose approved by the governing body

C)outstanding balances of all liabilities,regardless of their form,issued to acquire or improve the capital assets shown in the amount invested in capital assets

D)outstanding balances of bonds,notes,or other borrowings,issued to acquire or improve the capital assets shown in the amount invested in capital assets

A)bonds,notes,or other borrowings originally issued to acquire or improve the capital assets shown in the amount invested in capital assets

B)outstanding balances of bonds,notes,or other borrowings,issued for any purpose approved by the governing body

C)outstanding balances of all liabilities,regardless of their form,issued to acquire or improve the capital assets shown in the amount invested in capital assets

D)outstanding balances of bonds,notes,or other borrowings,issued to acquire or improve the capital assets shown in the amount invested in capital assets

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

26

What is the general rule for reporting on funds in the fund-level financial statements for fiduciary funds?

A)There is no requirement for reporting on fiduciary funds in the fund-level statements.

B)All individual major funds must be reported in separate columns of the fund-level financial statements for fiduciary funds;nonmajor funds may be combined in a single column.

C)All individual fiduciary funds,whether major or nonmajor,must be reported in separate columns of the fund-level financial statements for fiduciary funds.

D)Separate columns should be shown for each fund type,such as Investment Trust Funds (rather than individual funds),in the fund-level financial statements for fiduciary funds.

A)There is no requirement for reporting on fiduciary funds in the fund-level statements.

B)All individual major funds must be reported in separate columns of the fund-level financial statements for fiduciary funds;nonmajor funds may be combined in a single column.

C)All individual fiduciary funds,whether major or nonmajor,must be reported in separate columns of the fund-level financial statements for fiduciary funds.

D)Separate columns should be shown for each fund type,such as Investment Trust Funds (rather than individual funds),in the fund-level financial statements for fiduciary funds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following financial statements is not required to be prepared for proprietary funds in the fund-level financial statements?

A)Statement of net position (or balance sheet)

B)Statement of revenues,expenses,and changes in fund net assets

C)Statement of revenues,expenditures,and changes in fund balances

D)Statement of cash flows

A)Statement of net position (or balance sheet)

B)Statement of revenues,expenses,and changes in fund net assets

C)Statement of revenues,expenditures,and changes in fund balances

D)Statement of cash flows

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

28

Which of the following best expresses the kind of information included in notes to the financial statements?

A)notes help to explain differences of opinion between the preparer of financial statements and the auditor.

B)notes contain information essential to a user's understanding of the reporting government's financial position and resource inflows and outflows.

C)notes contain explanations of why the reporting unit did not follow generally accepted accounting principles.

D)notes contain the required management's discussion and analysis.

A)notes help to explain differences of opinion between the preparer of financial statements and the auditor.

B)notes contain information essential to a user's understanding of the reporting government's financial position and resource inflows and outflows.

C)notes contain explanations of why the reporting unit did not follow generally accepted accounting principles.

D)notes contain the required management's discussion and analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

29

Why are separate operating statements prepared for governmental funds and proprietary funds in the fund-level financial statements?

A)because a single operating statement would require too many columns for the average reader to understand readily

B)because governmental funds use the full accrual basis of accounting in the fund financial statements,whereas proprietary funds use the modified accrual basis of accounting

C)because governmental funds have a different measurement focus and basis of accounting than proprietary funds in the fund-level financial statements

D)because governmental fund operating statements need to be read together with the "budget and actual" schedules,whereas proprietary fund operating statements do not

A)because a single operating statement would require too many columns for the average reader to understand readily

B)because governmental funds use the full accrual basis of accounting in the fund financial statements,whereas proprietary funds use the modified accrual basis of accounting

C)because governmental funds have a different measurement focus and basis of accounting than proprietary funds in the fund-level financial statements

D)because governmental fund operating statements need to be read together with the "budget and actual" schedules,whereas proprietary fund operating statements do not

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

30

A municipality incurs liabilities in its operations (such as vacation leave and expected claim settlements)that could be classified as "long-term" because cash payouts will not occur for more than one year.The liabilities result from both governmental and proprietary activities.Where are these long-term liabilities reported in the fund-level balance sheets?

A)as noncurrent liabilities,in the appropriate fund column,on both fund level balance sheets

B)as noncurrent liabilities on both fund level balance sheets,but the long-term liabilities for governmental funds are reported only in the "total" column and not in any fund column

C)as noncurrent liabilities in the proprietary funds balance sheet;but long-term liabilities are not reported in the governmental funds balance sheet

D)long-term liabilities are not reported in the fund level balance sheets of either governmental or proprietary funds

A)as noncurrent liabilities,in the appropriate fund column,on both fund level balance sheets

B)as noncurrent liabilities on both fund level balance sheets,but the long-term liabilities for governmental funds are reported only in the "total" column and not in any fund column

C)as noncurrent liabilities in the proprietary funds balance sheet;but long-term liabilities are not reported in the governmental funds balance sheet

D)long-term liabilities are not reported in the fund level balance sheets of either governmental or proprietary funds

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

31

What is the purpose of preparing proprietary fund balance sheets in classified format?

A)to distinguish between current and noncurrent assets and liabilities

B)to distinguish between assets and liabilities

C)to distinguish between restricted and unrestricted net position

D)to segregate net position into three components: invested in capital assets,net of related debt;restricted;and unrestricted

A)to distinguish between current and noncurrent assets and liabilities

B)to distinguish between assets and liabilities

C)to distinguish between restricted and unrestricted net position

D)to segregate net position into three components: invested in capital assets,net of related debt;restricted;and unrestricted

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

32

Match between columns

الفرضيات:

The relationships between two primary governments and a third organization may be such that the third organization can be a component unit of both primary governments.

The relationships between two primary governments and a third organization may be such that the third organization can be a component unit of both primary governments.

An example of a state's ability to impose its will on the operations of a legally separate toll road is its ability to approve the road's proposed increases in toll rates.

An example of a state's ability to impose its will on the operations of a legally separate toll road is its ability to approve the road's proposed increases in toll rates.

الردود:

True

False

True

False

True

False

True

False

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following financial statements or schedules is prepared for all fiduciary funds?

A)Statement of fiduciary cash flows

B)Budgetary comparison schedule

C)Statement of fiduciary net position

D)Reconciliation between fund-level and government-wide level operating activities

A)Statement of fiduciary cash flows

B)Budgetary comparison schedule

C)Statement of fiduciary net position

D)Reconciliation between fund-level and government-wide level operating activities

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

34

A municipality allows its employees to accumulate up to 45 days' vacation pay that may be "cashed in" by the employees on retirement.Many employees whose salaries are paid from General Fund appropriations avail themselves of this opportunity.Where does this liability appear on the governmental funds balance sheet when employees are not expected to retire in the near future?

A)General Fund column;Accrued vacation leave caption

B)This liability is not reported in the governmental funds balance sheet.

C)General Fund column;Noncurrent liabilities caption

D)General Fund column;Payable from restricted assets caption

A)General Fund column;Accrued vacation leave caption

B)This liability is not reported in the governmental funds balance sheet.

C)General Fund column;Noncurrent liabilities caption

D)General Fund column;Payable from restricted assets caption

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

35

SEQ CHAPTER \h \r 1What is the reporting requirement for the fund balance section of the governmental funds balance sheet?

A)governmental fund balances should be reported in a single amount

B)governmental fund balances should be segregated in three components: invested in capital assets,net of related debt;restricted;and unrestricted

C)governmental fund balances should be segregated between reserved and unreserved amounts

D)governmental fund balances should be segregated in five components: nonspendable,restricted,committed,assigned and unassigned

A)governmental fund balances should be reported in a single amount

B)governmental fund balances should be segregated in three components: invested in capital assets,net of related debt;restricted;and unrestricted

C)governmental fund balances should be segregated between reserved and unreserved amounts

D)governmental fund balances should be segregated in five components: nonspendable,restricted,committed,assigned and unassigned

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

36

How are amounts due to other funds reported in fund-level financial statements?

A)assets in the balance sheet

B)expenditures in the statement of revenues,expenditures,and changes in fund balances

C)liabilities in the balance sheet

D)transfers out in the statement of revenues,expenditures,and changes in fund balances

A)assets in the balance sheet

B)expenditures in the statement of revenues,expenditures,and changes in fund balances

C)liabilities in the balance sheet

D)transfers out in the statement of revenues,expenditures,and changes in fund balances

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

37

How are long-term loan receivables reported in the fund balance section of governmental funds balance sheets?

A)nonspendable

B)unassigned

C)unrestricted

D)restricted,committed,assigned,or unassigned

A)nonspendable

B)unassigned

C)unrestricted

D)restricted,committed,assigned,or unassigned

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

38

Statistical tables included in the Comprehensive Annual Financial Report are intended to help users by providing what kind of information?

A)detailed data on the financial position and results of operations of each individual fund

B)additional financial,economic,and demographic data helpful in placing the financial statements of a government in a broader context

C)data showing whether the entity has delivered public services efficiently and effectively

D)an overview of the financial position and results of operations of the entity as a whole

A)detailed data on the financial position and results of operations of each individual fund

B)additional financial,economic,and demographic data helpful in placing the financial statements of a government in a broader context

C)data showing whether the entity has delivered public services efficiently and effectively

D)an overview of the financial position and results of operations of the entity as a whole

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

39

Which of the following best expresses the general rule regarding the reporting of operating revenues,nonoperating revenues,and special items in the proprietary funds statement of revenues,expenses,and changes in fund net position?

A)operating revenues,nonoperating revenues,and special items should be reported in separate sections of the statement.

B)operating revenues,nonoperating revenues,and special items should be included in a single section,headed "Revenues and other gains."

C)special items should be included as nonoperating revenues,but operating revenues and nonoperating revenues should be reported in separate sections of the statement.

D)nonoperating revenues and special items should be netted against nonoperating expenses and reported as a single item,captioned "other."

A)operating revenues,nonoperating revenues,and special items should be reported in separate sections of the statement.

B)operating revenues,nonoperating revenues,and special items should be included in a single section,headed "Revenues and other gains."

C)special items should be included as nonoperating revenues,but operating revenues and nonoperating revenues should be reported in separate sections of the statement.

D)nonoperating revenues and special items should be netted against nonoperating expenses and reported as a single item,captioned "other."

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

40

Budgetary comparison schedules (or statements)must be prepared for:

A)major governmental and proprietary funds

B)the General Fund and major Special Revenue Funds

C)only major governmental funds

D)all major fund and fiduciary funds

A)major governmental and proprietary funds

B)the General Fund and major Special Revenue Funds

C)only major governmental funds

D)all major fund and fiduciary funds

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

41

Match between columns

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

42

(Preparation of closing entries and fund level financial statements)

Following is a trial balance of City of Peachville's General Fund at December 31,2013.Prepare: (a)closing entries; (b)a post-closing trial balance; (c)a statement of revenues,expenditures,and changes in fund balance for the year ended December 31,2013;and (d)a balance sheet at December 31,2013.

Following is a trial balance of City of Peachville's General Fund at December 31,2013.Prepare: (a)closing entries; (b)a post-closing trial balance; (c)a statement of revenues,expenditures,and changes in fund balance for the year ended December 31,2013;and (d)a balance sheet at December 31,2013.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

43

(Classification of financing sources in financial statements)

Martin Township decides to construct a new city hall.Based on the following data,prepare a statement of revenues,expenditures,and changes in fund balance for Martin Township's Capital Projects Fund.All transactions occur within the calendar year 2013.

a.The Fund starts and ends the year with a zero fund balance.

b.The Fund's financing sources for the city hall project were: long-term bond proceeds - $5 million;operating transfer from the General Fund - $2 million;state grant - $1 million;interest from the temporary investment of cash - $70,000.

c.Total outlays for constructing the new city hall were: construction costs - $7,200,000;design and construction supervision fees - $600,000.

d.City laws require that,whenever bonds are used,any remaining difference between total financing sources and construction costs must be transferred to the Debt Service Fund.Therefore,$270,000 was transferred to the Debt Service Fund.

Martin Township decides to construct a new city hall.Based on the following data,prepare a statement of revenues,expenditures,and changes in fund balance for Martin Township's Capital Projects Fund.All transactions occur within the calendar year 2013.

a.The Fund starts and ends the year with a zero fund balance.

b.The Fund's financing sources for the city hall project were: long-term bond proceeds - $5 million;operating transfer from the General Fund - $2 million;state grant - $1 million;interest from the temporary investment of cash - $70,000.

c.Total outlays for constructing the new city hall were: construction costs - $7,200,000;design and construction supervision fees - $600,000.

d.City laws require that,whenever bonds are used,any remaining difference between total financing sources and construction costs must be transferred to the Debt Service Fund.Therefore,$270,000 was transferred to the Debt Service Fund.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 43 في هذه المجموعة.