Deck 30: Portfolio Optimization with Negative Correlation: Finding Minimum Variance and Weight Allocation

ملء الشاشة (f)

سؤال

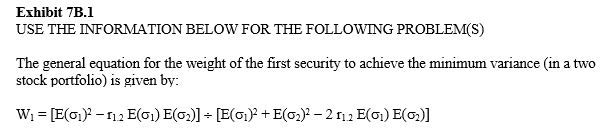

Refer to Exhibit 7B.1.What is the value of W₁ when r₁.₂ = -1 and E(s₁)= .10 and E(s₂)= .12?

A) 45.46%

B) 50.00%

C) 59.45%

D) 54.55%

E) 74.55%

سؤال

Refer to Exhibit 7B.1.Show the minimum portfolio variance for a portfolio of two risky assets when r₁.₂ = -1.

A) E(s1) ¸ [E(s1) + E(s2)]

B) E(s1) ¸ [E(s1) - E(s2)]

C) E(s2) ¸ [E(s1) + E(s2)]

D) E(s2) ¸ [E(s1) - E(s2)]

E) None of the above

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/2

العب

ملء الشاشة (f)

Deck 30: Portfolio Optimization with Negative Correlation: Finding Minimum Variance and Weight Allocation

Refer to Exhibit 7B.1.What is the value of W₁ when r₁.₂ = -1 and E(s₁)= .10 and E(s₂)= .12?

A) 45.46%

B) 50.00%

C) 59.45%

D) 54.55%

E) 74.55%

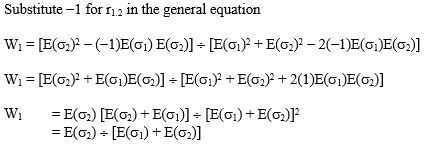

D

W₁ = 12/(.12 + .10)= .5455 = 54.55%

W₁ = 12/(.12 + .10)= .5455 = 54.55%

Refer to Exhibit 7B.1.Show the minimum portfolio variance for a portfolio of two risky assets when r₁.₂ = -1.

A) E(s1) ¸ [E(s1) + E(s2)]

B) E(s1) ¸ [E(s1) - E(s2)]

C) E(s2) ¸ [E(s1) + E(s2)]

D) E(s2) ¸ [E(s1) - E(s2)]

E) None of the above

C

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 2 في هذه المجموعة.