Deck 5: The Mathematics of Diversification

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

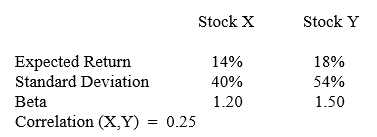

The questions relate to the following table of information:

-What is the expected return for a portfolio with 60% invested in X and 40% invested in Y?

A) 14.4%

B) 14.9%

C) 15.6%

D) 16.1%

-What is the expected return for a portfolio with 60% invested in X and 40% invested in Y?

A) 14.4%

B) 14.9%

C) 15.6%

D) 16.1%

سؤال

The questions relate to the following table of information:

-What is the standard deviation for a portfolio with 60% invested in X and 40% invested in Y?

A) 32.4%

B) 36.1%

C) 41.2%

D) 45.6%

-What is the standard deviation for a portfolio with 60% invested in X and 40% invested in Y?

A) 32.4%

B) 36.1%

C) 41.2%

D) 45.6%

سؤال

The questions relate to the following table of information:

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

A) 1.12

B) 1.22

C) 1.32

D) 1.42

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

A) 1.12

B) 1.22

C) 1.32

D) 1.42

سؤال

The questions relate to the following table of information:

-What is the covariance between Stock X and Stock Y?

A) 0.025

B) 0.033

C) 0.047

D) 0.054

-What is the covariance between Stock X and Stock Y?

A) 0.025

B) 0.033

C) 0.047

D) 0.054

سؤال

The questions relate to the following table of information:

-What is the percent invested in Stock X to yield the minimum variance portfolio with Stock X and Stock Y?

A) 0.21

B) 0.38

C) 0.51

D) 0.69

-What is the percent invested in Stock X to yield the minimum variance portfolio with Stock X and Stock Y?

A) 0.21

B) 0.38

C) 0.51

D) 0.69

سؤال

The questions relate to the following table of information:

-What is the expected return for a portfolio with 20% invested in X and 80% invested in Y?

A) 14.9%

B) 15.6%

C) 16.5%

D) 17.2%

-What is the expected return for a portfolio with 20% invested in X and 80% invested in Y?

A) 14.9%

B) 15.6%

C) 16.5%

D) 17.2%

سؤال

The questions relate to the following table of information:

-What is the standard deviation for a portfolio with 20% invested in X and 80% invested in Y?

A) 41.2%

B) 45.8%

C) 47.1%

D) 49.6%

-What is the standard deviation for a portfolio with 20% invested in X and 80% invested in Y?

A) 41.2%

B) 45.8%

C) 47.1%

D) 49.6%

سؤال

The questions relate to the following table of information:

-What is the beta for a portfolio with 20% invested in X and 80% invested in Y?

A) 1.14

B) 1.24

C) 1.34

D) 1.44

-What is the beta for a portfolio with 20% invested in X and 80% invested in Y?

A) 1.14

B) 1.24

C) 1.34

D) 1.44

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/50

العب

ملء الشاشة (f)

Deck 5: The Mathematics of Diversification

1

The work of Harry Markowitz is based on the search for

A) efficient portfolios

B) undervalued securities

C) the highest long-term growth rates

D) minimum risk portfolios

A) efficient portfolios

B) undervalued securities

C) the highest long-term growth rates

D) minimum risk portfolios

efficient portfolios

2

Securities A and B have expected returns of 12% and 15%, respectively. If you put 30% of your money in Security A and the remainder in B, what is the portfolio expected return?

A) 13.4%

B) 14.1%

C) 14.6%

D) 15.3%

A) 13.4%

B) 14.1%

C) 14.6%

D) 15.3%

14.1%

3

Securities A and B have expected returns of 12% and 15%, respectively. If you put 40% of your money in Security A and the remainder in B, what is the portfolio expected return?

A) 13.4%

B) 13.8%

C) 14.6%

D) 15.3%

A) 13.4%

B) 13.8%

C) 14.6%

D) 15.3%

13.8%

4

The variance of a two-security portfolio decreases as the return correlation of the two securities

A) increases

B) decreases

C) changes in either direction

D) cannot be determined

A) increases

B) decreases

C) changes in either direction

D) cannot be determined

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

5

A security has a return variance of 25%. The standard deviation of returns is

A) 5%

B) 15%

C) 25%

D) 50%

A) 5%

B) 15%

C) 25%

D) 50%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

6

A security has a return variance of 16%. The standard deviation of returns is

A) 4%

B) 16%

C) 40%

D) 50%

A) 4%

B) 16%

C) 40%

D) 50%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

7

Covariance is the product of two securities'

A) expected deviations from their means

B) standard deviations

C) betas

D) standard deviations divided by their correlation

A) expected deviations from their means

B) standard deviations

C) betas

D) standard deviations divided by their correlation

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

8

The covariance of a random variable with itself is

A) its correlation with itself

B) its standard deviation

C) its variance

D) equal to 1.0

A) its correlation with itself

B) its standard deviation

C) its variance

D) equal to 1.0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

9

Covariance is _____ correlation is ______.

A) positive, positive or negative

B) negative, positive or negative

C) positive or negative, positive or zero

D) positive or negative, positive or negative

A) positive, positive or negative

B) negative, positive or negative

C) positive or negative, positive or zero

D) positive or negative, positive or negative

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

10

For a six-security portfolio, it is necessary to calculate ___ covariances plus ___ variances.

A) 36, 6

B) 30, 6

C) 15, 6

D) 30, 12

A) 36, 6

B) 30, 6

C) 15, 6

D) 30, 12

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

11

COV (A,B) = .335. What is COV (B,A)?

A) - 0.335

B) 0.335

C) (0.335 × 0.335)

D) Cannot be determined

A) - 0.335

B) 0.335

C) (0.335 × 0.335)

D) Cannot be determined

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

12

One of the first proponents of the single index model was

A) William Sharpe

B) Robert Merton

C) Eugene Fama

D) Merton Miller

A) William Sharpe

B) Robert Merton

C) Eugene Fama

D) Merton Miller

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

13

Without knowing beta, determining portfolio variance with a sixty-security portfolio requires ___ statistics per security.

A) 1

B) 60

C) 3600/2

D) 3600

A) 1

B) 60

C) 3600/2

D) 3600

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

14

Securities A, B, and C have betas of 1.2, 1.3, and 1.7, respectively. What is the beta of an equally weighted portfolio of all three?

A) 1.15

B) 1.40

C) 1.55

D) 1.60

A) 1.15

B) 1.40

C) 1.55

D) 1.60

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

15

Securities A, B, and C have betas of 1.2, 1.3, and 1.7, respectively. What is the beta of a portfolio composed of 1/2 A and 1/4 each of B and C?

A) 1.15

B) 1.35

C) 1.55

D) 1.60

A) 1.15

B) 1.35

C) 1.55

D) 1.60

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

16

A diversified portfolio has a beta of 1.2; the market variance is 0.25. What is the diversified portfolio's variance?

A) 0.33

B) 0.36

C) 0.41

D) 0.44

A) 0.33

B) 0.36

C) 0.41

D) 0.44

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

17

Security A has a beta of 1.2; security B has a beta of 0.8. If the market variance is 0.30, what is COV (A,B)?

A) .255

B) .288

C) .314

D) .355

A) .255

B) .288

C) .314

D) .355

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

18

As portfolio size increases, the variance of the error term generally

A) increases

B) decreases

C) approaches 1.0

D) becomes erratic

A) increases

B) decreases

C) approaches 1.0

D) becomes erratic

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

19

The least risk portfolio is called the

A) optimum portfolio

B) efficient portfolio

C) minimum variance portfolio

D) market portfolio

A) optimum portfolio

B) efficient portfolio

C) minimum variance portfolio

D) market portfolio

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

20

Industry effects are associated with

A) the single index model

B) the multi-index model

C) the Markowitz model

D) the covariance matrix

A) the single index model

B) the multi-index model

C) the Markowitz model

D) the covariance matrix

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

21

COV (A,B) is equal to

A) the product of their standard deviations and their correlation

B) the product of their variances and their correlation

C) the product of their standard deviations and their covariances

D) the product of their variances and their covariances

A) the product of their standard deviations and their correlation

B) the product of their variances and their correlation

C) the product of their standard deviations and their covariances

D) the product of their variances and their covariances

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

22

The covariance between a constant and a random variable is

A) zero

B) 1.0

C) their correlation

D) the product of their betas

A) zero

B) 1.0

C) their correlation

D) the product of their betas

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

23

The covariance between a security's returns and those of the market index is 0.03. If the security beta is 1.15, what is the market variance?

A) 0.005

B) 0.010

C) 0.021

D) 0.026

A) 0.005

B) 0.010

C) 0.021

D) 0.026

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

24

COV(A,B) = 0.50; the variance of the market is 0.25, and the beta of Security A is 1.00. What is the beta of security B?

A) 1.00

B) 1.25

C) 1.50

D) 2.00

A) 1.00

B) 1.25

C) 1.50

D) 2.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

25

There are 1,700 stocks in the Value Line index. How many covariances would have to be calculated in order to use the Markowitz full covariance model?

A) 1,700

B) 5,650

C) 12,350

D) 1,444,150

A) 1,700

B) 5,650

C) 12,350

D) 1,444,150

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

26

There are 1,700 stocks in the Value Line index. How many betas would have to be calculated in order to find the portfolio variance?

A) 1,700

B) 5,650

C) 12,350

D) 1,444,150

A) 1,700

B) 5,650

C) 12,350

D) 1,444,150

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

27

Knowing beta, determining the portfolio with a sixty-security fully diversified portfolio requires ______ statistic(s) per security.

A) 1

B) 60

C) 3600/2

D) 3600

A) 1

B) 60

C) 3600/2

D) 3600

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

28

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the expected return for a portfolio with 80% invested in Stock A and 20% invested in Stock B?

A) 17%

B) 19%

C) 21%

D) 23%

A) 17%

B) 19%

C) 21%

D) 23%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

29

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the standard deviation for a portfolio with 80% invested in Stock A and 20% invested in Stock B?

A) 15.8%

B) 18.4%

C) 22.0%

D) 28.0%

A) 15.8%

B) 18.4%

C) 22.0%

D) 28.0%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

30

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the beta for a portfolio with 80% invested in Stock A and 20% invested in Stock B?

A) 0.57

B) 0.77

C) 0.97

D) 1.17

A) 0.57

B) 0.77

C) 0.97

D) 1.17

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

31

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the covariance between Stock A and Stock B?

A) 0.015

B) 0.025

C) 0.035

D) 0.045

A) 0.015

B) 0.025

C) 0.035

D) 0.045

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

32

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the percent invested in Stock A to yield the minimum standard deviation portfolio containing Stock A and Stock B?

A) 25%

B) 50%

C) 75%

D) 90%

A) 25%

B) 50%

C) 75%

D) 90%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

33

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the expected return for a portfolio with 50% invested in Stock A and 50% invested in Stock B?

A) 18%

B) 19%

C) 20%

D) 21%

A) 18%

B) 19%

C) 20%

D) 21%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

34

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the standard deviation for a portfolio with 50% invested in Stock A and 50% invested in Stock B?

A) 15%

B) 20%

C) 23%

D) 25%

A) 15%

B) 20%

C) 23%

D) 25%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

35

Suppose Stock A has an expected return of 15%, a standard deviation of 20%, and a Beta of 0.4 while Stock B has an expected return of 25%, a standard deviation of 30% and a beta of 1.25, and the correlation between the two stocks is 0.25. What is the beta for a portfolio with 50% invested in Stock A and 50% invested in Stock B?

A) 0.425

B) 0.625

C) 0.825

D) 1.125

A) 0.425

B) 0.625

C) 0.825

D) 1.125

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

36

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the expected return for a portfolio with 70% invested in Stock M and 30% invested in Stock N?

A) 11%

B) 13%

C) 15%

D) 17%

A) 11%

B) 13%

C) 15%

D) 17%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

37

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the standard deviation for a portfolio with 70% invested in Stock M and 30% invested in Stock N?

A) 12.5%

B) 13.6%

C) 15.7%

D) 18.0%

A) 12.5%

B) 13.6%

C) 15.7%

D) 18.0%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

38

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the covariance between Stock M and Stock N?

A) 0.01052

B) 0.01875

C) 0.03425

D) 0.04775

A) 0.01052

B) 0.01875

C) 0.03425

D) 0.04775

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

39

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the percent invested in Stock M to yield the minimum standard deviation portfolio containing Stock M and Stock N?

A) 34%

B) 55%

C) 73%

D) 92%

A) 34%

B) 55%

C) 73%

D) 92%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

40

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the expected return for a portfolio with 80% invested in Stock M and 20% invested in Stock N?

A) 12%

B) 14%

C) 16%

D) 18%

A) 12%

B) 14%

C) 16%

D) 18%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

41

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the standard deviation for a portfolio with 80% invested in Stock M and 20% invested in Stock N?

A) 13.2%

B) 15.1%

C) 17.3%

D) 21.5%

A) 13.2%

B) 15.1%

C) 17.3%

D) 21.5%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

42

Suppose Stock M has an expected return of 10%, a standard deviation of 15%, and a Beta of 0.6 while Stock N has an expected return of 20%, a standard deviation of 25% and a beta of 1.04, and the correlation between the two stocks is 0.50. What is the beta for a portfolio with 80% invested in Stock M and 20% invested in Stock N?

A) 0.688

B) 0.738

C) 0.878

D) 0.968

A) 0.688

B) 0.738

C) 0.878

D) 0.968

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

43

The questions relate to the following table of information:

-What is the expected return for a portfolio with 60% invested in X and 40% invested in Y?

A) 14.4%

B) 14.9%

C) 15.6%

D) 16.1%

-What is the expected return for a portfolio with 60% invested in X and 40% invested in Y?

A) 14.4%

B) 14.9%

C) 15.6%

D) 16.1%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

44

The questions relate to the following table of information:

-What is the standard deviation for a portfolio with 60% invested in X and 40% invested in Y?

A) 32.4%

B) 36.1%

C) 41.2%

D) 45.6%

-What is the standard deviation for a portfolio with 60% invested in X and 40% invested in Y?

A) 32.4%

B) 36.1%

C) 41.2%

D) 45.6%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

45

The questions relate to the following table of information:

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

A) 1.12

B) 1.22

C) 1.32

D) 1.42

-What is the beta for a portfolio with 60% invested in X and 40% invested in Y?

A) 1.12

B) 1.22

C) 1.32

D) 1.42

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

46

The questions relate to the following table of information:

-What is the covariance between Stock X and Stock Y?

A) 0.025

B) 0.033

C) 0.047

D) 0.054

-What is the covariance between Stock X and Stock Y?

A) 0.025

B) 0.033

C) 0.047

D) 0.054

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

47

The questions relate to the following table of information:

-What is the percent invested in Stock X to yield the minimum variance portfolio with Stock X and Stock Y?

A) 0.21

B) 0.38

C) 0.51

D) 0.69

-What is the percent invested in Stock X to yield the minimum variance portfolio with Stock X and Stock Y?

A) 0.21

B) 0.38

C) 0.51

D) 0.69

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

48

The questions relate to the following table of information:

-What is the expected return for a portfolio with 20% invested in X and 80% invested in Y?

A) 14.9%

B) 15.6%

C) 16.5%

D) 17.2%

-What is the expected return for a portfolio with 20% invested in X and 80% invested in Y?

A) 14.9%

B) 15.6%

C) 16.5%

D) 17.2%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

49

The questions relate to the following table of information:

-What is the standard deviation for a portfolio with 20% invested in X and 80% invested in Y?

A) 41.2%

B) 45.8%

C) 47.1%

D) 49.6%

-What is the standard deviation for a portfolio with 20% invested in X and 80% invested in Y?

A) 41.2%

B) 45.8%

C) 47.1%

D) 49.6%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

50

The questions relate to the following table of information:

-What is the beta for a portfolio with 20% invested in X and 80% invested in Y?

A) 1.14

B) 1.24

C) 1.34

D) 1.44

-What is the beta for a portfolio with 20% invested in X and 80% invested in Y?

A) 1.14

B) 1.24

C) 1.34

D) 1.44

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.