Deck 9: Reporting and Analysing Liabilities

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

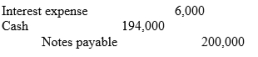

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-The entry made by Tawonga Construction Company Ltd on 1 January to record the proceeds and issue of the note is:

A)

B)

C)

D)

-The entry made by Tawonga Construction Company Ltd on 1 January to record the proceeds and issue of the note is:

A)

B)

C)

D)

سؤال

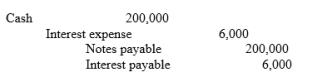

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-What is the adjusting entry required if Tawonga Construction Company Ltd prepares financial statements on 30 June?

A)

B)

C)

D)

-What is the adjusting entry required if Tawonga Construction Company Ltd prepares financial statements on 30 June?

A)

B)

C)

D)

سؤال

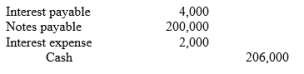

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-What entry will Tawonga Construction Company Ltd make to pay off the note and interest at maturity?

A)

B)

C)

D)

-What entry will Tawonga Construction Company Ltd make to pay off the note and interest at maturity?

A)

B)

C)

D)

سؤال

Wayfarer Ltd withheld $54 000 of 'PAYG'. The entry to record payment of the tax to the Tax Office is:

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

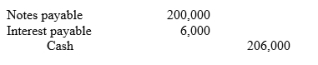

On 1 October, Simon's Solar Service borrows $150,000 from Statewide Bank on a 3 month, 4% note.

-What accrual entry must Simon's Solar Service make on 31 December before financial statements are prepared?

A)

B)

C)

D)

-What accrual entry must Simon's Solar Service make on 31 December before financial statements are prepared?

A)

B)

C)

D)

سؤال

On 1 October, Simon's Solar Service borrows $150,000 from Statewide Bank on a 3 month, 4% note.

-The entry by Simon's Solar Service to record payment of the note and accrued interest on 1 January is:

A)

B)

C)

D)

-The entry by Simon's Solar Service to record payment of the note and accrued interest on 1 January is:

A)

B)

C)

D)

سؤال

Emerald Ltd has the following payroll deductions for the week ended 31 March: $20,000 medical fund deductions; $18,000 pay-as-you-go withheld tax deductions. What is the journal entry to record the obligation for these deductions?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

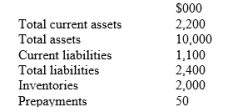

The following information relates to Rangitata Ltd as at 30 June 2019.

The quick ratio is:

The quick ratio is:

A) 2.

B) 9.

C) 14.

D) 0.14.

The quick ratio is:A) 2.

B) 9.

C) 14.

D) 0.14.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Beach Ltd's payroll for June 2019 was $20,000. The pay week ended on 30 June and was paid on the 1 July. Payroll deductions from amounts paid during June were as follows:

Required:

Required:

(a) State the current liabilities relating to Beach Ltd's payroll at 30 June 2019.

(b) Prepare the journal entry to record the payroll for the pay week ended 30 June.

Required:(a) State the current liabilities relating to Beach Ltd's payroll at 30 June 2019.

(b) Prepare the journal entry to record the payroll for the pay week ended 30 June.

سؤال

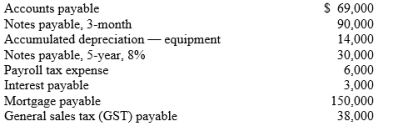

The Candy Company Ltd has the following selected accounts after posting adjusting entries:

Required:

Required:

(a) Prepare the current liability section of The Candy Company's statement of financial position, assuming $25,000 of the mortgage is payable next year.

(b) Comment on The Candy Company's liquidity, assuming total current assets are $400,000.

Required:(a) Prepare the current liability section of The Candy Company's statement of financial position, assuming $25,000 of the mortgage is payable next year.

(b) Comment on The Candy Company's liquidity, assuming total current assets are $400,000.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

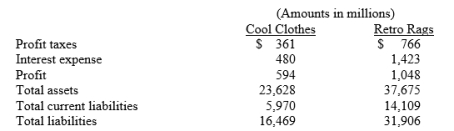

The following information is available from the annual reports of 2 clothing retailers

Required:

Required:

(a) Based on the preceding information, compute the following ratios for each company:

1. liabilities to total assets

2. times interest earned.

(b) What conclusion concerning the companies' long-run solvency can be drawn from these ratios?

Required:(a) Based on the preceding information, compute the following ratios for each company:

1. liabilities to total assets

2. times interest earned.

(b) What conclusion concerning the companies' long-run solvency can be drawn from these ratios?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/81

العب

ملء الشاشة (f)

Deck 9: Reporting and Analysing Liabilities

1

A current liability is an obligation that can reasonably be expected to be paid within the operating cycle of a business.

True

2

Notes payable, accounts payable, revenue received in advance and accrued liabilities are all examples of non-current liabilities.

False

3

A $15,000, 8%, 9-month note payable requires an interest payment of $900 at maturity.

True

4

In Australia the taxation authority is the Australian Securities and Investments Commission (ASIC).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

5

An employer business is required by law to withhold tax from an employee's gross pay and remit it to the taxation authority (the ATO).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

6

Sydney Symphony sells 200 season tickets for $20,000 that includes a five-concert season. The amount of unearned ticket revenue after the third concert is $12,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

7

Non-current liabilities are obligations of a business that it expects to pay after one year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

8

Notes that are secured over some of the issuer's assets are called debentures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

9

Shareholder control is diminished by the issue of debt financing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

10

Although interest expense reduces net profit, earnings per share is often higher under debt financing because no additional shares have been issued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

11

The face value of a note is also the principal amount due at maturity of the note.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

12

If a company redeems notes and debentures, it adds debt to its statement of financial position.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

13

If a borrower is unable to repay a mortgage, the lender has no right to recover the debt against the mortgaged property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

14

Each time a borrower makes a mortgage repayment, the borrower must allocate the amount between unearned revenue and revenue.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

15

To the extent that long-term debt is repayable within the same period as current liabilities, it should be classified as a current liability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

16

Provisions are liabilities for which the amount of the future sacrifice is uncertain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

17

A warranty is an obligation of the receiver of goods and services that a future claim will not be made against the supplier of the goods if the goods prove to be unsatisfactory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

18

From a manufacturer's point of view, providing a warranty creates an obligation to repair or replace goods if certain faults arise within the warranty period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

19

Warranties are not recognised as liabilities by manufacturers as the amount of any future claims is too uncertain and/or unlikely.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

20

Provisions for warranties may only be reported in the liabilities section of a statement of financial position as current liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

21

Notes payable usually require the borrower to pay:

A) revenue.

B) interest.

C) prepayments.

D) contingencies.

A) revenue.

B) interest.

C) prepayments.

D) contingencies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following would not be classified as a current liability?

A) Accrued taxes payable

B) Revenue received in advance

C) Mortgage

D) Notes payable

A) Accrued taxes payable

B) Revenue received in advance

C) Mortgage

D) Notes payable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

23

The account 'Revenue received in advance' is properly treated as a/an:

A) asset.

B) liability.

C) revenue.

D) payment to shareholders.

A) asset.

B) liability.

C) revenue.

D) payment to shareholders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

24

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-The entry made by Tawonga Construction Company Ltd on 1 January to record the proceeds and issue of the note is:

A)

B)

C)

D)

-The entry made by Tawonga Construction Company Ltd on 1 January to record the proceeds and issue of the note is:

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

25

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-What is the adjusting entry required if Tawonga Construction Company Ltd prepares financial statements on 30 June?

A)

B)

C)

D)

-What is the adjusting entry required if Tawonga Construction Company Ltd prepares financial statements on 30 June?

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

26

Bondi Bank agrees to lend Tawonga Construction Company Ltd $200,000 on 1 January. Tawonga Construction Company Ltd signs a $200,000, 4%, 9-month note.

-What entry will Tawonga Construction Company Ltd make to pay off the note and interest at maturity?

A)

B)

C)

D)

-What entry will Tawonga Construction Company Ltd make to pay off the note and interest at maturity?

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

27

Wayfarer Ltd withheld $54 000 of 'PAYG'. The entry to record payment of the tax to the Tax Office is:

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

28

On 1 October, Simon's Solar Service borrows $150,000 from Statewide Bank on a 3 month, 4% note.

-What accrual entry must Simon's Solar Service make on 31 December before financial statements are prepared?

A)

B)

C)

D)

-What accrual entry must Simon's Solar Service make on 31 December before financial statements are prepared?

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

29

On 1 October, Simon's Solar Service borrows $150,000 from Statewide Bank on a 3 month, 4% note.

-The entry by Simon's Solar Service to record payment of the note and accrued interest on 1 January is:

A)

B)

C)

D)

-The entry by Simon's Solar Service to record payment of the note and accrued interest on 1 January is:

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

30

Emerald Ltd has the following payroll deductions for the week ended 31 March: $20,000 medical fund deductions; $18,000 pay-as-you-go withheld tax deductions. What is the journal entry to record the obligation for these deductions?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

31

On 1 January 2019 Bradley Ltd, a calendar-year company, issued $200,000 of notes payable of which $50,000 is due on 1 January for each of the next four years. The proper statement of financial position for presentation on 31 December 2019 is:

A) Current liabilities, $200,000

B) Non-current liabilities, $200,000

C) Current liabilities, $50,000; Non-current liabilities, $150,000

D) Current liabilities, $150,000; Non-current liabilities, $50,000

A) Current liabilities, $200,000

B) Non-current liabilities, $200,000

C) Current liabilities, $50,000; Non-current liabilities, $150,000

D) Current liabilities, $150,000; Non-current liabilities, $50,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

32

Companies may find it attractive to issue debt instead of equity because:

A) interest on debt is tax deductible.

B) interest on debt has to be repaid by the shareholders, not the company.

C) interest on debt is always a cheaper form of finance than dividends on shares.

D) interest on debt is not locked in for repayment.

A) interest on debt is tax deductible.

B) interest on debt has to be repaid by the shareholders, not the company.

C) interest on debt is always a cheaper form of finance than dividends on shares.

D) interest on debt is not locked in for repayment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

33

The face value of a note is also known as the:

A) market value.

B) principal.

C) trading value.

D) unsecured amount.

A) market value.

B) principal.

C) trading value.

D) unsecured amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

34

When a company repurchases its unsecured notes, the debt has been:

A) redeemed.

B) discounted.

C) revalued.

D) determined.

A) redeemed.

B) discounted.

C) revalued.

D) determined.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

35

A loan secured by a charge over a property is also known as a:

A) contingent liability.

B) warranty.

C) mortgage.

D) provision.

A) contingent liability.

B) warranty.

C) mortgage.

D) provision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

36

Century Ltd has outstanding debentures with a face value of $50,000. If Century redeems the debentures for $55,000 it must record:

A) a gain of $5,000.

B) a gain of $55,000.

C) a loss of $5,000.

D) a loss of $50,000.

A) a gain of $5,000.

B) a gain of $55,000.

C) a loss of $5,000.

D) a loss of $50,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

37

A borrower must allocate mortgage repayments between:

A) interest expense and interest revenue.

B) interest expense and loan liability.

C) interest revenue and loan liability.

D) loan liability and shareholders' equity.

A) interest expense and interest revenue.

B) interest expense and loan liability.

C) interest revenue and loan liability.

D) loan liability and shareholders' equity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

38

When recording a mortgage payment made by a borrower, the borrower will:

A) debit cash, and credit interest expense.

B) debit mortgage payable, and credit interest expense.

C) debit both interest expense and mortgage payable, and credit cash.

D) debit cash, and credit both interest expense and mortgage payable.

A) debit cash, and credit interest expense.

B) debit mortgage payable, and credit interest expense.

C) debit both interest expense and mortgage payable, and credit cash.

D) debit cash, and credit both interest expense and mortgage payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

39

Liabilities for which the amount of the future sacrifice is uncertain are regarded as:

A) warranties.

B) withholdings.

C) redeemables.

D) provisions.

A) warranties.

B) withholdings.

C) redeemables.

D) provisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

40

Obligations to pay for goods or services that have been provided but for which a supplier's invoice has not yet been received are recorded as:

A) debentures.

B) accounts payable.

C) warranties.

D) contingencies.

A) debentures.

B) accounts payable.

C) warranties.

D) contingencies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

41

Obligations for which the amount of the future sacrifice is so uncertain that it cannot be measured reliably are classified as:

A) warranties.

B) contingent liabilities.

C) provisions.

D) accruals.

A) warranties.

B) contingent liabilities.

C) provisions.

D) accruals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which of the following is not an example of a provision?

A) Warranty for motor vehicle repairs

B) Employee long service leave entitlements

C) Debentures issued

D) Employee annual leave entitlements

A) Warranty for motor vehicle repairs

B) Employee long service leave entitlements

C) Debentures issued

D) Employee annual leave entitlements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

43

Which of the following is an example of a contingent liability?

A) Legal proceedings against the business for a damages claim

B) Warranties for repairs

C) Debentures payable

D) Mortgage owing

A) Legal proceedings against the business for a damages claim

B) Warranties for repairs

C) Debentures payable

D) Mortgage owing

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

44

Warranty obligations are classified as provisions because the:

A) amount of the future sacrifice is certain.

B) future cost of repairs is known with certainty.

C) amount of future claims is uncertain.

D) cost of future servicing is not able to be estimated reliably.

A) amount of the future sacrifice is certain.

B) future cost of repairs is known with certainty.

C) amount of future claims is uncertain.

D) cost of future servicing is not able to be estimated reliably.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

45

Timeless Ltd produces clocks and sells them with a one-year warranty. The warranty provision account currently has a debit balance of $4,000. The estimated cost of repairing clocks that have already been sold is $18,000. The adjustment needed to update the warranty provision account is:

A) debit $18,000.

B) credit $18,000.

C) debit $22,000.

D) credit $22,000.

A) debit $18,000.

B) credit $18,000.

C) debit $22,000.

D) credit $22,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

46

Vagabond Ltd manufactures handbags and provides a six-month quality warranty. The provision for warranty account has a credit balance of $50,000 and the estimated future obligations for warranty work is $190,000. The adjustment necessary to update the provision account is a:

A) debit of $140,000.

B) debit of $240,000.

C) credit of $140,000.

D) credit of $240,000.

A) debit of $140,000.

B) debit of $240,000.

C) credit of $140,000.

D) credit of $240,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

47

A quick ratio is a measure of an entity's:

A) long-term liquidity.

B) medium-term liquidity.

C) short-term liquidity.

D) quickness at paying creditors.

A) long-term liquidity.

B) medium-term liquidity.

C) short-term liquidity.

D) quickness at paying creditors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

48

The quick ratio calculated by a business is also referred to as the:

A) solvency ratio.

B) acid test.

C) marketable test.

D) interest coverage ratio.

A) solvency ratio.

B) acid test.

C) marketable test.

D) interest coverage ratio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

49

The following information relates to Rangitata Ltd as at 30 June 2019.

The quick ratio is:

A) 2.

B) 9.

C) 14.

D) 0.14.

The quick ratio is:A) 2.

B) 9.

C) 14.

D) 0.14.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

50

Match (by letter) each of the following as being :

-3 months of revenues received in advance for an annual subscription to a magazine

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-3 months of revenues received in advance for an annual subscription to a magazine

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

51

Match (by letter) each of the following as being :

-Pay-as-you-go withholding tax payable

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-Pay-as-you-go withholding tax payable

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

52

Match (by letter) each of the following as being :

-Unsecured notes with 9 months to maturity

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-Unsecured notes with 9 months to maturity

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

53

Match (by letter) each of the following as being :

-20-year Mortgage

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-20-year Mortgage

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

54

Match (by letter) each of the following as being :

-5 year debentures payable

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-5 year debentures payable

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

55

Match (by letter) each of the following as being :

-Interest expense

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-Interest expense

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

56

Match (by letter) each of the following as being :

-Warranty expense

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

-Warranty expense

A) current liability (CL)

B) non-current liability (NCL)

C) neither (NA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

57

The NZA Bank agrees to issue $180,000 of 3-month notes payable to Campbell Ltd on 1 March 2019. The notes are interest-bearing at the rate of 10%.

Prepare the journal entries to record:

(a) the notes on issue date

(b) the repayment of the notes including the interest, on due date.

Prepare the journal entries to record:

(a) the notes on issue date

(b) the repayment of the notes including the interest, on due date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

58

Beach Ltd's payroll for June 2019 was $20,000. The pay week ended on 30 June and was paid on the 1 July. Payroll deductions from amounts paid during June were as follows:

Required:

(a) State the current liabilities relating to Beach Ltd's payroll at 30 June 2019.

(b) Prepare the journal entry to record the payroll for the pay week ended 30 June.

Required:(a) State the current liabilities relating to Beach Ltd's payroll at 30 June 2019.

(b) Prepare the journal entry to record the payroll for the pay week ended 30 June.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

59

The Candy Company Ltd has the following selected accounts after posting adjusting entries:

Required:

(a) Prepare the current liability section of The Candy Company's statement of financial position, assuming $25,000 of the mortgage is payable next year.

(b) Comment on The Candy Company's liquidity, assuming total current assets are $400,000.

Required:(a) Prepare the current liability section of The Candy Company's statement of financial position, assuming $25,000 of the mortgage is payable next year.

(b) Comment on The Candy Company's liquidity, assuming total current assets are $400,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

60

On 1 March, Marcel Ltd borrows $90,000 from the Eastward Bank by signing a 6-month, 9%, interest-bearing note.

Instructions: Prepare the necessary entries below associated with the note payable on the books of Marcel Ltd.

(a) Prepare the entry on 1 March when the note was issued.

(b) Prepare any adjusting entries necessary on 30 June in order to prepare the semi-annual financial statements. Assume no other interest accrual entries have been made.

(c) Prepare the entry to record payment of the note at maturity.

Instructions: Prepare the necessary entries below associated with the note payable on the books of Marcel Ltd.

(a) Prepare the entry on 1 March when the note was issued.

(b) Prepare any adjusting entries necessary on 30 June in order to prepare the semi-annual financial statements. Assume no other interest accrual entries have been made.

(c) Prepare the entry to record payment of the note at maturity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

61

On May 31, Pearl Ltd borrows $20,000 from their bank by signing a 2 month, 12%, interest-bearing note.

Instructions: Prepare the necessary entries below associated with the note payable on the books of Pearl Ltd.

(a) Prepare the entry on June 1 when the note was issued.

(b) Prepare any adjusting entries necessary on 30 June in order to prepare the monthly financial statements. Assume no other interest accrual entries have been made.

(c) Prepare the entry to record payment of the note at maturity.

Instructions: Prepare the necessary entries below associated with the note payable on the books of Pearl Ltd.

(a) Prepare the entry on June 1 when the note was issued.

(b) Prepare any adjusting entries necessary on 30 June in order to prepare the monthly financial statements. Assume no other interest accrual entries have been made.

(c) Prepare the entry to record payment of the note at maturity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

62

The Mainland group of hotels billed its customers a total of $1,060,000 for the month of November. The total includes a 6% goods and services tax (GST).

Instructions :

(a) Determine the proper amount of revenue to report for the month.

(b) Prepare the general journal entry to record the revenue and related liabilities for the month.

Instructions :

(a) Determine the proper amount of revenue to report for the month.

(b) Prepare the general journal entry to record the revenue and related liabilities for the month.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

63

March Ltd had cash sales of $44,000 for the month of June. Sales are subject to 10% goods and services tax (GST). Prepare the entry to record the sale.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

64

Seagull Publications publishes a golf magazine for women. The magazine sells for $5.00 a copy on newsstands. Yearly subscriptions to the magazine cost $50 per year (12 issues). During December 2019, Seagull Publications sells 5,000 copies of the golf magazine at news-stands and receives payment for 6,000 subscriptions for 2020. Financial statements are prepared monthly.

Instructions:

(a) Prepare the December 2019 journal entries to record the newsstand sales and subscriptions received.

(b) Prepare the necessary adjusting entry on 31 January, 2020. The January 2020 issue has been mailed to subscribers.

Instructions:

(a) Prepare the December 2019 journal entries to record the newsstand sales and subscriptions received.

(b) Prepare the necessary adjusting entry on 31 January, 2020. The January 2020 issue has been mailed to subscribers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

65

On 1 January 2019 the Guildford Group Ltd issued $800,000, 8%, 10-year unsecured notes at face value. Interest is payable semi-annually on 1 July and 1 January. Guildford Group has a calendar year end.

Instructions: Prepare all entries related to the unsecured note issue for 2019.

Instructions: Prepare all entries related to the unsecured note issue for 2019.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

66

The following information is available from the annual reports of 2 clothing retailers

Required:

(a) Based on the preceding information, compute the following ratios for each company:

1. liabilities to total assets

2. times interest earned.

(b) What conclusion concerning the companies' long-run solvency can be drawn from these ratios?

Required:(a) Based on the preceding information, compute the following ratios for each company:

1. liabilities to total assets

2. times interest earned.

(b) What conclusion concerning the companies' long-run solvency can be drawn from these ratios?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

67

Complete the following statements:

-Liabilities are classified on the statement of financial position as being _______________ liabilities or ______________ liabilities.

-Liabilities are classified on the statement of financial position as being _______________ liabilities or ______________ liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

68

Complete the following statements:

-Goods and services tax (GST) collected from customers are a(n) ______________ of the business until they are remitted to the tax office.

-Goods and services tax (GST) collected from customers are a(n) ______________ of the business until they are remitted to the tax office.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

69

Complete the following statements:

-The ______________ ratio is a measure of a company's immediate short-term liquidity.

-The ______________ ratio is a measure of a company's immediate short-term liquidity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

70

Complete the following statements:

-The ________ value of a note payable is the amount of ____________ due at maturity date.

-The ________ value of a note payable is the amount of ____________ due at maturity date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

71

Match the descriptions with their terms:

-The amount paid by the investor on issue of a debenture or unsecured note

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-The amount paid by the investor on issue of a debenture or unsecured note

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

72

Match the descriptions with their terms:

-The value today of an amount to be paid or received at some date in the future after taking into account current interest rates

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-The value today of an amount to be paid or received at some date in the future after taking into account current interest rates

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

73

Match the descriptions with their terms:

-Costs of borrowing money

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-Costs of borrowing money

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

74

Match the descriptions with their terms:

-An obligation that is not classified as a current liability

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-An obligation that is not classified as a current liability

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

75

Match the descriptions with their terms:

-A measure of an entity's immediate short-term liquidity, also called the acid-test

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-A measure of an entity's immediate short-term liquidity, also called the acid-test

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

76

Match the descriptions with their terms:

-A liability for which the amount is uncertain but able to be measured reliably by estimation

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-A liability for which the amount is uncertain but able to be measured reliably by estimation

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

77

Match the descriptions with their terms:

-Rate used to determine the amount of interest the borrower pays and the investor receives

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-Rate used to determine the amount of interest the borrower pays and the investor receives

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

78

Match the descriptions with their terms:

-An obligation of the supplier of goods and services to the purchased that the product will be functional or that work performed will remain satisfactory for a period after the sale of goods

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-An obligation of the supplier of goods and services to the purchased that the product will be functional or that work performed will remain satisfactory for a period after the sale of goods

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

79

Match the descriptions with their terms:

-A loan that is secured by a charge over property

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-A loan that is secured by a charge over property

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

80

Match the descriptions with their terms:

-An obligation than can reasonably be expected to be paid within one year or the operating cycle of a business

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

-An obligation than can reasonably be expected to be paid within one year or the operating cycle of a business

A) Non-current liability

B) Present value

C) Warranty

D) Issue price

E) Current liability

F) Borrowing costs

G) Contract interest rate

H) Mortgage

I) Quick ratio

J) Provision

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 81 في هذه المجموعة.