Deck 11: Factor Models and the Arbitrage Pricing Theory

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

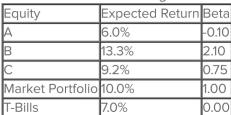

An investor is considerinq the three equities given below:

Calculate the expected return and beta of a portfolio equally weighted between equities B and C. Demonstrate that holding equity A actually reduces risk by comparing the risk of a portfolio equally weighted between equity B and T-Bills with a portfolio equally weighted between equity B and A.

Calculate the expected return and beta of a portfolio equally weighted between equities B and C. Demonstrate that holding equity A actually reduces risk by comparing the risk of a portfolio equally weighted between equity B and T-Bills with a portfolio equally weighted between equity B and A.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/48

العب

ملء الشاشة (f)

Deck 11: Factor Models and the Arbitrage Pricing Theory

1

The single factor APT model that resembles the market model uses _________ as the single factor.

A)arbitrage fees

B)GNP

C)the inflation rate

D)the market return

E)the risk-free return

A)arbitrage fees

B)GNP

C)the inflation rate

D)the market return

E)the risk-free return

the market return

2

The betas along with the factors in the APT adjust the expected return for:

A)calculation errors.

B)unsystematic risks.

C)spurious correlations of factors.

D)differences between actual and expected levels of factors.

E)All of the above.

A)calculation errors.

B)unsystematic risks.

C)spurious correlations of factors.

D)differences between actual and expected levels of factors.

E)All of the above.

differences between actual and expected levels of factors.

3

If the expected rate of inflation was 3% and the actual rate was 6.2%; the systematic response coefficient from inflation, bI , would result in a change in any security return of ___ bI .

A)9.2%

B)3.2%

C)-3.2%

D)3.0%

E)6.2%

A)9.2%

B)3.2%

C)-3.2%

D)3.0%

E)6.2%

3.2%

4

The term Corr(ε R , ε T ) = 0 tells us that:

A)all error terms of company R and T are 0.

B)the unsystematic risk of companies R and T is unrelated or uncorrelated.

C)the correlation between the returns of companies R and T is -1.

D)the systematic risk companies R and T is unrelated.

E)None of the above.

A)all error terms of company R and T are 0.

B)the unsystematic risk of companies R and T is unrelated or uncorrelated.

C)the correlation between the returns of companies R and T is -1.

D)the systematic risk companies R and T is unrelated.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

5

A security that has a beta of zero will have an expected return of:

A)zero.

B)the market risk premium.

C)the risk free rate.

D)less than the risk free rate but not negative.

E)less than the risk free rate which can be negative.

A)zero.

B)the market risk premium.

C)the risk free rate.

D)less than the risk free rate but not negative.

E)less than the risk free rate which can be negative.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

6

Shareholders discount many corporate announcements because of their prior expectations.If an announcement causes the price to change it will mostly be driven by:

A)the expected part of the announcement.

B)market inefficiency.

C)the unexpected part of the announcement.

D)the systematic risk.

E)None of the above.

A)the expected part of the announcement.

B)market inefficiency.

C)the unexpected part of the announcement.

D)the systematic risk.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

7

A criticism of the CAPM is that it:

A)ignores the return on the market portfolio.

B)ignores the risk-free return.

C)requires a single measure of systematic risk.

D)utilizes too many factors.

E)None of the above.

A)ignores the return on the market portfolio.

B)ignores the risk-free return.

C)requires a single measure of systematic risk.

D)utilizes too many factors.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

8

Which of the following is true about the impact on market price of a security when a company makes an announcement and the market has discounted the news?

A)The price will change a great deal; even though the impact is primarily in the future, the

Future value is discounted to the present.

B)The price will change little, if at all, since the impact is primarily in the future.

C)The price will change little, if at all, since the market considers this information

Unimportant.

D)The price will change little, if at all, since the market considers this information untrue.

E)The price will change little, if at all, since the market has already included this information

In the security's price.

A)The price will change a great deal; even though the impact is primarily in the future, the

Future value is discounted to the present.

B)The price will change little, if at all, since the impact is primarily in the future.

C)The price will change little, if at all, since the market considers this information

Unimportant.

D)The price will change little, if at all, since the market considers this information untrue.

E)The price will change little, if at all, since the market has already included this information

In the security's price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

9

The acronym APT stands for:

A)Arbitrage Pricing Techniques.

B)Absolute Profit Theory.

C)Arbitrage Pricing Theory.

D)Asset Puting Theory.

E)Assured Price Techniques.

A)Arbitrage Pricing Techniques.

B)Absolute Profit Theory.

C)Arbitrage Pricing Theory.

D)Asset Puting Theory.

E)Assured Price Techniques.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

10

The acronym CAPM stands for:

A)Capital Asset Pricing Model.

B)Certain Arbitrage Pressure Model.

C)Current Arbitrage Prices Model.

D)Cumulative Asset Price Model.

E)None of the above.

A)Capital Asset Pricing Model.

B)Certain Arbitrage Pressure Model.

C)Current Arbitrage Prices Model.

D)Cumulative Asset Price Model.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

11

In a portfolio of risky assets, the response to a factor, Fi , can be determined by:

A)summing the weighted bi s and multiplying by the factor Fi.

B)summing the Fis.

C)adding the average weighted expected returns.

D)summing the weighted random errors.

E)All of the above.

A)summing the weighted bi s and multiplying by the factor Fi.

B)summing the Fis.

C)adding the average weighted expected returns.

D)summing the weighted random errors.

E)All of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

12

In the equation R = E(R) + U, the three symbols stand for:

A)average return, expected return, and unexpected return.

B)required return, expected return, and unbiased return.

C)actual total return, expected return, and unexpected return.

D)required return, expected return, and unbiased risk.

E)risk, expected return, and unsystematic risk.

A)average return, expected return, and unexpected return.

B)required return, expected return, and unbiased return.

C)actual total return, expected return, and unexpected return.

D)required return, expected return, and unbiased risk.

E)risk, expected return, and unsystematic risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

13

In normal market conditions if a security has a negative beta:

A)the security always has a positive return.

B)the security has an expected return above the risk-free return.

C)the security has an expected return less than the risk-free rate.

D)the security has an expected return equal to the market portfolio.

E)Both A and B.

A)the security always has a positive return.

B)the security has an expected return above the risk-free return.

C)the security has an expected return less than the risk-free rate.

D)the security has an expected return equal to the market portfolio.

E)Both A and B.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

14

A company owning gold mines will probably have a _____ inflation beta because an ___ increase in inflation is usually associated with an increase in gold prices.

A)negative; anticipated

B)positive; anticipated

C)negative; unanticipated

D)positive; unanticipated

E)None of the above.

A)negative; anticipated

B)positive; anticipated

C)negative; unanticipated

D)positive; unanticipated

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

15

The unexpected return on a security, U, is made up of:

A)market risk and systematic risk.

B)systematic risk and idiosyncratic risk.

C)idiosyncratic risk and unsystematic risk.

D)expected return and market risk.

E)expected return and idiosyncratic risk.

A)market risk and systematic risk.

B)systematic risk and idiosyncratic risk.

C)idiosyncratic risk and unsystematic risk.

D)expected return and market risk.

E)expected return and idiosyncratic risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

16

What would NOT be true about a GNP beta?

A)If a equity's GNP beta = 1.5, the equity will experience a 1.5% increase for every 1% surprise

Increase in GNP.

B)If a equity's GNP beta = -1.5, the equity will experience a 1.5% decrease for every 1%

Surprise increase in GNP.

C)It is a measure of risk.

D)It measures the impact of systematic risk associated with GNP.

E)None of the above.

A)If a equity's GNP beta = 1.5, the equity will experience a 1.5% increase for every 1% surprise

Increase in GNP.

B)If a equity's GNP beta = -1.5, the equity will experience a 1.5% decrease for every 1%

Surprise increase in GNP.

C)It is a measure of risk.

D)It measures the impact of systematic risk associated with GNP.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

17

In the one factor (APT) model, the characteristic line to estimate bi passes through the origin, unlike the estimate used in the CAPM because:

A)the relationship is between the actual return on a security and the market index.

B)the relationship measures the change in the security return over time versus the change in

The market return.

C)the relationship measures the change in excess return on a security versus GNP.

D)the relationship measures the change in excess return on a security versus the return on

The factor about its mean of zero.

E)Cannot be determined without actual data.

A)the relationship is between the actual return on a security and the market index.

B)the relationship measures the change in the security return over time versus the change in

The market return.

C)the relationship measures the change in excess return on a security versus GNP.

D)the relationship measures the change in excess return on a security versus the return on

The factor about its mean of zero.

E)Cannot be determined without actual data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

18

For a diversified portfolio including a large number of equities, the:

A)weighted average expected return goes to zero.

B)weighted average of the betas goes to zero.

C)weighted average of the unsystematic risk goes to zero.

D)return of the portfolio goes to zero.

E)return on the portfolio equals the risk-free rate.

A)weighted average expected return goes to zero.

B)weighted average of the betas goes to zero.

C)weighted average of the unsystematic risk goes to zero.

D)return of the portfolio goes to zero.

E)return on the portfolio equals the risk-free rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

19

A factor is a variable that:

A)affects the returns of risky assets in a systematic fashion.

B)affects the returns of risky assets in an unsystematic fashion.

C)correlates with risky asset returns in a unsystematic fashion.

D)does not correlate with the returns of risky assets in an systematic fashion.

E)None of the above.

A)affects the returns of risky assets in a systematic fashion.

B)affects the returns of risky assets in an unsystematic fashion.

C)correlates with risky asset returns in a unsystematic fashion.

D)does not correlate with the returns of risky assets in an systematic fashion.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

20

Assuming that the single factor APT model applies, the beta for the market portfolio is:

A)zero.

B)one.

C)the average of the risk free beta and the beta for the highest risk security.

D)impossible to calculate without collecting sample data.

E)None of the above.

A)zero.

B)one.

C)the average of the risk free beta and the beta for the highest risk security.

D)impossible to calculate without collecting sample data.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

21

Assume that the single factor APT model applies and a portfolio exists such that 2/3 of the funds are invested in Security Q and the rest in the risk-free asset.Security Q has a beta of 1.5.The

Portfolio has a beta of:

A)0.00

B)0.50

C)0.75

D)1.00

E)1.50

Portfolio has a beta of:

A)0.00

B)0.50

C)0.75

D)1.00

E)1.50

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

22

Suppose that we have identified three important systematic risk factors given by exports, inflation, and industrial production.In the beginning of the year, growth in these three factors is estimated at

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.Calculate the equity's total return if the company announces that an important patent filing

Has been granted sooner than expected and will earn the company 5% more in return.

A)7.95%

B)9.95%

C)11.55%

D)7.90%

E)9.35%

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.Calculate the equity's total return if the company announces that an important patent filing

Has been granted sooner than expected and will earn the company 5% more in return.

A)7.95%

B)9.95%

C)11.55%

D)7.90%

E)9.35%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

23

Suppose the MiniCD Corporation's ordinary equity has a return of 12%.Assume the risk-free rate is 4%, the expected market return is 9%, and no unsystematic influence affected Mini's return.The

Beta for MiniCD is:

A)0.89.

B)1.60.

C)2.40.

D)3.00.

E)It is impossible to calculate beta without the inflation rate.

Beta for MiniCD is:

A)0.89.

B)1.60.

C)2.40.

D)3.00.

E)It is impossible to calculate beta without the inflation rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

24

Consider the following two statements about systematic and unsystematic risk: (i) News about GNP is always related to systematic risk.

(ii) News about the CEO of a company is only unsystematic if it was not expected.

A)(i) is correct, and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)Both (i) and (ii) are correct.

D)Both (i) and (ii) are incorrect.

E)News is not related to risk.

(ii) News about the CEO of a company is only unsystematic if it was not expected.

A)(i) is correct, and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)Both (i) and (ii) are correct.

D)Both (i) and (ii) are incorrect.

E)News is not related to risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

25

Compared to the CAPM, the APT has an advantage: the model adds factors until the unsystematic risk of any security is uncorrelated with the unsystematic risk of every other security.

A)As a result, unsystematic risk steadily falls as the number of securities in the portfolio

Increases.

B)systematic risks do not decrease as the number of securities in the portfolio increases.

C)A and B are both correct.

D)A and B are both incorrect.

E)Only B separates the APT from the CAPM.

A)As a result, unsystematic risk steadily falls as the number of securities in the portfolio

Increases.

B)systematic risks do not decrease as the number of securities in the portfolio increases.

C)A and B are both correct.

D)A and B are both incorrect.

E)Only B separates the APT from the CAPM.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

26

Suppose that we have identified three important systematic risk factors given by exports, inflation, and industrial production.In the beginning of the year, growth in these three factors is estimated at

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.What would the equity's total return be if the actual growth in each of the facts was equal to

Growth expected? Assume no unexpected news on the patent.

A)4%

B)5%

C)6%

D)7%

E)8%

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.What would the equity's total return be if the actual growth in each of the facts was equal to

Growth expected? Assume no unexpected news on the patent.

A)4%

B)5%

C)6%

D)7%

E)8%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

27

Consider the following two statements about inflation betas: (i) If a company's share price return is negatively related to the risk of inflation, it has a positive

Inflation beta.

(ii) Inflation betas are either positive for all equities, or negative for all equities, since inflation is a

Systematic risk factor.

A)(i) is correct, and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)Both (i) and (ii) are correct.

D)Both (i) and (ii) are incorrect.

E)Inflation is never priced in the APT.

Inflation beta.

(ii) Inflation betas are either positive for all equities, or negative for all equities, since inflation is a

Systematic risk factor.

A)(i) is correct, and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)Both (i) and (ii) are correct.

D)Both (i) and (ii) are incorrect.

E)Inflation is never priced in the APT.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

28

The most realistic APT model would likely include:

A)multiple factors.

B)only one factor.

C)a factor to measure inflation.

D)Both A and C.

E)Both B and C.

A)multiple factors.

B)only one factor.

C)a factor to measure inflation.

D)Both A and C.

E)Both B and C.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

29

An investor is considerinq the three equities given below:

Calculate the expected return and beta of a portfolio equally weighted between equities B and C. Demonstrate that holding equity A actually reduces risk by comparing the risk of a portfolio equally weighted between equity B and T-Bills with a portfolio equally weighted between equity B and A.

Calculate the expected return and beta of a portfolio equally weighted between equities B and C. Demonstrate that holding equity A actually reduces risk by comparing the risk of a portfolio equally weighted between equity B and T-Bills with a portfolio equally weighted between equity B and A.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

30

Suppose that we have identified three important systematic risk factors given by exports, inflation, and industrial production.In the beginning of the year, growth in these three factors is estimated at

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.If the expected return on the

Equity is 6%, and no unexpected news concerning the equity surfaces, calculate the equity's total

Return.

A)2.95%

B)4.95%

C)6.55%

D)7.40%

E)8.85%

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.If the expected return on the

Equity is 6%, and no unexpected news concerning the equity surfaces, calculate the equity's total

Return.

A)2.95%

B)4.95%

C)6.55%

D)7.40%

E)8.85%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

31

To estimate the cost of equity capital for a firm using the CAPM, it is necessary to have:

A)company financial leverage, beta, and the market risk premium.

B)company financial leverage, beta, and the risk-free rate.

C)beta, company financial leverage, and the industry beta.

D)beta, company financial leverage, and the market risk premium.

E)beta, the risk-free rate, and the market risk premium.

A)company financial leverage, beta, and the market risk premium.

B)company financial leverage, beta, and the risk-free rate.

C)beta, company financial leverage, and the industry beta.

D)beta, company financial leverage, and the market risk premium.

E)beta, the risk-free rate, and the market risk premium.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

32

The systematic response coefficient for productivity, bP, would produce an unexpected change in any security return of __ bP if the expected rate of productivity was 1.5% and the actual rate was

2)25%.

A)0.75%

B)-0.75%

C)2.25%

D)-2.25%

E)1.5%

2)25%.

A)0.75%

B)-0.75%

C)2.25%

D)-2.25%

E)1.5%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following statements is/are true?

A)Both APT and CAPM argue that expected excess return must be proportional to the

Beta(s).

B)APT and CAPM are the only approaches to measure expected returns in risky assets.

C)Both CAPM and APT are risk-based models.

D)Both A and B are true.

E)Both A and C are true.

A)Both APT and CAPM argue that expected excess return must be proportional to the

Beta(s).

B)APT and CAPM are the only approaches to measure expected returns in risky assets.

C)Both CAPM and APT are risk-based models.

D)Both A and B are true.

E)Both A and C are true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

34

Parametric or empirical models rely on:

A)security betas explaining systematic factor relationships.

B)finding regularities and relations in past market data.

C)there being no true explanations of pricing relationships.

D)always being able to find the exception to the rule.

E)None of the above.

A)security betas explaining systematic factor relationships.

B)finding regularities and relations in past market data.

C)there being no true explanations of pricing relationships.

D)always being able to find the exception to the rule.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

35

Three factors likely to occur in the APT model are:

A)unemployment, inflation, and current rates.

B)inflation, GNP, and interest rates.

C)current rates, inflation and change in housing prices.

D)unemployment, college tuition, and GNP.

E)This cannot be determined or even estimated.

A)unemployment, inflation, and current rates.

B)inflation, GNP, and interest rates.

C)current rates, inflation and change in housing prices.

D)unemployment, college tuition, and GNP.

E)This cannot be determined or even estimated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

36

A growth equity portfolio and a value portfolio might be characterized:

A)each by their P/E relative to the index P/E; high P/E for growth and lower for value.

B)as earning a high rate of return for a growth security and a low rate of return for value

Security irrespective of risk.

C)low unsystematic risk and high systematic risk respectively.

D)moderate systematic risk and zero systematic risk respectively.

E)None of the above.

A)each by their P/E relative to the index P/E; high P/E for growth and lower for value.

B)as earning a high rate of return for a growth security and a low rate of return for value

Security irrespective of risk.

C)low unsystematic risk and high systematic risk respectively.

D)moderate systematic risk and zero systematic risk respectively.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

37

Suppose that we have identified three important systematic risk factors given by exports, inflation, and industrial production.In the beginning of the year, growth in these three factors is estimated at

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.Calculate the equity's total return if the company announces that they had an industrial

Accident and the operating facilities will closed down for some time thus resulting in a loss by the

Company of 7% in return.

A)-4.05%

B)-2.05%

C)4.55%

D)0.40%

E)1.85%

-1%, 2.5%, and 3.5% respectively.However, actual growth in these factors turn out to be 1%, -2%, and

2%)The factor betas are given by bEX = 1.8, bI = 0.7, and bIP = 1.0.The expected return on the equity

Is 6%.Calculate the equity's total return if the company announces that they had an industrial

Accident and the operating facilities will closed down for some time thus resulting in a loss by the

Company of 7% in return.

A)-4.05%

B)-2.05%

C)4.55%

D)0.40%

E)1.85%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

38

Consider the following two statements: (i) The market beta is the standardized variance of the market portfolio.

(ii) The market beta is an appropriate measure of risk under the assumptions of homogenous

Expectations and riskless borrowing and lending.

A)(i) is correct and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)(i) and (ii) are both correct.

D)(i) and (ii) are both incorrect.

E)There is no such thing as a market beta.

(ii) The market beta is an appropriate measure of risk under the assumptions of homogenous

Expectations and riskless borrowing and lending.

A)(i) is correct and (ii) is incorrect.

B)(ii) is correct and (i) is incorrect.

C)(i) and (ii) are both correct.

D)(i) and (ii) are both incorrect.

E)There is no such thing as a market beta.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

39

Both the APT and the CAPM imply a positive relationship between expected return and risk.The APT views risk:

A)very similarly to the CAPM via the beta of the security.

B)in terms of individual intersecurity correlation versus the beta of the CAPM.

C)via the industry wide or marketwide factors creating correlation between securities.

D)the standardized deviation of the covariance.

E)None of the above.

A)very similarly to the CAPM via the beta of the security.

B)in terms of individual intersecurity correlation versus the beta of the CAPM.

C)via the industry wide or marketwide factors creating correlation between securities.

D)the standardized deviation of the covariance.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

40

Suppose the JumpStart Corporation's ordinary equity has a beta of 0.8.If the risk-free rate is 4% and the expected market return is 9%, the expected return for JumpStart's common is:

A)3.2%.

B)4.0%.

C)7.2%.

D)8.0%.

E)9.0%.

A)3.2%.

B)4.0%.

C)7.2%.

D)8.0%.

E)9.0%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

41

You have a 3 factor model to explain returns.Explain what a factor represents in the context of the APT? Each factor is multiplied by a beta.What do these represent and how do they relate to the actual return?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

42

Suppose you hold a portfolio that consists of an investment of 50 per cent in an asset A and the remainder invested at the risk-free rate.What happens to the beta of the portfolio if the risk-free rate doubles?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

43

What does the APT assume about trading costs? And why does that matter?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

44

In recent paper, R.David McLean of the University of Alberta and Jeffrey Pontiff of Boston College look at the impact of academic papers on "market anomalies": finance papers that have successfully tried to find new risk factors.They argue that investors should be reading these papers.In an efficient market, what would be the result if investors indeed read these papers?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

45

Explain the conceptual differences in the theoretical development of the CAPM and APT.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

46

Suppose a new type of risk appears.It is systematic, uncorrelated with previous systematic risks, was not priced before, but can be measured by a single variable.You try to price it, and you use both the CAPM and the APT.Explain how this new risk makes its way into each of the approaches.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

47

Suppose you have a portfolio that contains 2 securities.You are considering adding a third security. Now assume that none of these securities carries any unsystematic risk.What will happen to the total risk of the portfolio if you add the third security?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

48

An investor is using the APT to calculate expected returns and make investment decisions.He has three years of data.The investor runs into a finance professor who offers to supply him with an additional three years of data free of charge.Why should the investor accept the offer?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 48 في هذه المجموعة.